From the “raw and frequently hilarious” (The New York Times) investment guru andNew York Timesbestselling author ofThe Wolf of Wall Streetwho inspired the Oscar-winning film of the same name, a witty and clear-eyed guide for anyone who wants to play the stock market to their advantage and learn the secrets of a top Wall Street investor.

From Jordan Belfort, The Wolf of Investing offers “concrete insights and advice” (Booklist) on when to buy, sell, hold, and cash out; how to make smarter (and safer) investments; and how to build significant wealth over both the short- and long-term. Unlike traditional investment books, each page of Jordan’s lessons, colorful stories, and principles entertains you with the charismatic swagger portrayed so famously on the screen by Leonardo DiCaprio.

Belfort teaches you everything you need to know about savvy investing—even if whatever stock you’ve touched has turned to yesterday’s trash. As you read this guide, you will not only learn life’s most profitable lessons, but you’ll also laugh out loud at Belfort’s brazen honesty and salty wit. After being enraged by watching big banks steal money from individual investors and determined to right the wrongs of his own infamous past, Belfort now shows regular investors how we can use Wall Street to our advantage.

Whether you’re new to investing or want to take your portfolio to the next level, you will learn everything Belfort knows about the stock market from The Wolf of Investing.

There is no insight in this book for advanced / investment community. It can be a starter book for someone who wants to learn few things.

Summary is

Do’s:

- Invest in Index funds / ETFs (example are given) - Research using Valueline, Moodys, CFRA, Morningstar

Don’t

- Don’t watch Media like CNBC - Don’t invest based on what you hear at the barbershop (Gamestop mania types) - Daily traders (trade w 5% of your portfolio) - 2 books are given in the footnote - Don’t follow social influencers - Don’t read click bait newsletters

Always tough to take the advice from a millionaire who made his name doing the complete opposite of what he recommends. Either way, think it’s good information but wouldn’t really recommend it.

1. Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX) 2. Vanguard Short-Term Bond Index Fund Admiral Shares (VBIRX) 3. SPDR Portfolio Aggregate Bond ETF (SPAB) 4. Schwab US Aggregate Bond Fund ETF (SHCZ) 5. SPDR Short-Term Corp Bond ETF (SPSB) 6. iShares Core 1-5 Years US Bond ETF (ISTB)

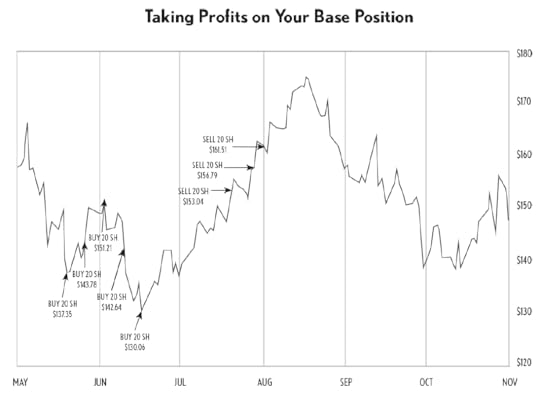

Base Trading Strategy:

1. Picking the Correct Stock 2. Establishing your initial base position 3. Selling shares to take a short-term trading profit: sell 20% of shares at 10% gain 4. Buying back shares to reestablish your base position 5. Rinsing and repeating, again and again

Most of this book is about the history of Wall Street, which I enjoyed. The last few chapters got into investing.

Takeaways: 1. Day Trading is stupid and no one should do it. This is an ongoing theme in most investing books. He actually provided some statistics on what percentage people lose when they day trade.

2. ETF's are the way to go for investing. VOO is one of the most recommended, but anything Vanguard seems to be the golden goose.

3. YOu shouldn't only buy ETF's. Diversify. 80% stocks/20% Bonds is a starting point. It protects your investment. There are bond ETF's so you don't have to try and pick individual bonds.

when that sad realization came bubbling up into my brain.

condence grows stronger with each passing day.

have the worst sense of timing since Napoléon invaded Russia in the dead of winter.

“What’s a wild banshee?” “It’s like a… a wild Indian. You know, screaming, yelling, shooting arrows.

let’s table that discussion until I’ve gone through the dierent strategies

Crypto, on the other hand, should make up only 5 percent of their total portfolio, at most.

ultimately robbing them of their wealth.

Financial freedom to do whatever you want, whenever you want, with whomever you want, as much as you want.

throwing good money after bad

Gordita whipped her head around, narrowed her eyes, and shot me a look; the unspoken words were: “You better agree with me, if you know what’s good for you!”

it’s gone; it’s left the fucking building, along with Elvis.

Net Asset Value (NAV) = (Total Assets of the Fund - Total Liabilities of the Fund) / Shares Oustanding

Warren Buett is as old as the hills

had the foresight to invest $10,000 in Berkshire Hathaway when Buett rst assumed control in 1964, that investment would now be worth $410 million.

To calculate the total number of outstanding shares, you simply add up all the shares of a company’s stock that are currently being held by individual investors, institutional investors (such as mutual funds and pension funds), and the company’s management team, and then subtract the shares that are being held by the company itself through a stock buyback program.

a high P/E ratio means that investors are willing to pay a very large multiple on the company’s annual earnings, because they are extremely bullish on its future growth prospects.

a company that’s growing extremely fast, with a high gross margin and a compelling business model, will typically trade with a much higher P/E ratio than a slow-growing company that maintains razor-thin margins and has no discernible way of rapidly growing its earnings.

If its P/E ratio is above the industry average, it suggests that investors are bullish on the company’s future growth potential relative to the rest of the industry.

there’s a ne line between investors who think that good news is coming out and investors who know that good news is coming out.

it’s also a common reason why investors might nd themselves doing three to ve years in Club Fed

a bond represents a promise from the issuer to the holder to repay the full face amount of the bond at a certain point in the future (referred to as the bond’s maturity date), plus an agreed-upon amount of interest dispersed at regular intervals (referred to as the bond’s coupon rate).

when interest rates are moving higher, Team Debt gets the advantage and money will ow out of the stock market and into the bond market. This is why, when interest rates are on the rise, the stock market tends to fall. To that end, there is an inverse relationship between the direction of interest rates and overall investor sentiment. Specically, a decrease in interest rates causes investor sentiment in general to rise

capitalist version of our Shakespearean dilemma, “to sell or not to sell,”

might it make sense to continue holding the stock based on a value play?

That, my friend, is the quickest way to end up in the poorhouse.

simple process called changing your mind based on new information.

unleash my inner carnivore

revolving door between Washington and Wall Street rotating with the speed of an F-5 tornado

earliest days of Wall Street and colonial America in the 1600s

When the Brits assumed control in 1676, they changed the city’s name from New Amsterdam to New York, and they dubbed the “walled street” Wall Street.

It started in 1711, when Wall Street was chosen as the ocial site for the rst organized slave auctions in the New World, with the city taking a cut on every sale.

if you think there’s fraud on Wall Street now, just imagine what it was like back in the 1700s, with no regulator

We the Subscribers, Brokers for the Purchase and Sale of Public Stock, do hereby solemnly promise and pledge ourselves to each other, that we will not buy or sell from this day for any person whatsoever, any kind of Public Stock, at a less rate than one quarter per cent Commission on the Specie value and that we will give a preference to each other in our Negotiations. In Testimony whereof we have set our hands this 17th day of May of New York, 1792.

Known as the Buttonwood Agreement

the rst rule of thumb was that there were no rules at all, and the second rule of thumb was that the only dierence between right and wrong was that wrong meant getting caught.

unlike the scapegoat, who would spend years in jail and have his reputation shattered, the member would walk away without even a slap on the wrist and with his reputation intact.

agreeable weather

I don’t owe you or your rm a bent nickel.

Besides, the broker never mentioned the term “margin call,” only buying on margin. That gives him the moral high ground; clearly he’s been wronged. He has every right to demand his money back, no two ways about it!

the bastard is lying through his greedy teeth!

The old fine-print trick! They got him!

the nancial equivalent of an avalanche at the top of Mount Everest—no matter how small it starts, it can’t be stopped until it reaches the bottom

People realized that the money that they thought they had waiting for them safely in the bank had actually been loaned out to Wall Street speculators who’d been buying dogshit

“But the day is young. I’m still hopeful.”

A short squeeze occurs when the price of a stock (or any asset) increases rapidly, causing short sellers to incur signicant losses, which then forces many of them to buy back the shares in order to meet margin calls.

foot messengers running around Lower Manhattan, picking up and delivering physical stock certicates from all the buyers and sellers. They did away with all that after the 1960s.

“If you were to check the electronic stock ledger, whose name would you see listed as the owner of those shares?

All stocks are held in what’s called street name nowadays. That means the owner of record on the electronic register is the brokerage rm that sells a client the stock, not the actual buyer.”

“You’re still listed as the beneficial owner of the stock on our internal register, so there’s no dierence to you financially.

Never has someone who knows so little thought they knew so much!

This trade isn’t going the wrong way! It’s going one way, and that’s right down the toilet bowl.

letting the inmates rule the asylum; electing an arsonist to become the fire chief

risks of giving power to someone with a history of exploiting it

to hightail it and run.

the truth lies somewhere in the middle

There are risks around every corner and danger at every turn.

Seeds of doubt have been sowed in their subconscious, where they’ll quietly lie like a dormant virus.

a prospectus, by its very nature, is designed to make the positives seem less positive and the negatives seem more negative

massive competition, no foothold in the market, questionable patents, a worthless trademark, and a failure-prone management team that has a consistent track record for running companies into the ground.

a bunch of overgrown adolescents wearing jeans and sneakers and dim-witted expressions.

I ashed the manager a comrade-in-arms sort of smile, as if to say, “Don’t worry, I know what goes on on a Wall Street sales oor. I’m not gonna blow the whistle on you!”

enough online advertising to choke a horse

the playing field had been leveled

if they gave FDR an inch, he would take a yard, and before they knew it, they’d be under his yoke.

“For the people we trust, regulation is simple. We’ll simply hand them a set of laws that they’re obligated to follow, and their internal moral compasses will take care of the rest. And as far as everyone else goes, we’ll watch them like fucking hawks.”

economic statistics are reported in two distinct ways: 1. Nominal terms 2. Real terms

“dividend yield.” Staying with the example of IBM, you divide its annual dividend of $6 a share by its current share price of $120, and you end up with a number that’s expressed as a percentage, which, in this case, is 5 percent. In other words, if you simply buy IBM and hold it, and the stock stays exactly where it is, you will still end up with an ROI of 5 percent per year.

When a company is young and experiencing rapid growth, it’s very rare for it to pay a dividend—because it needs every dollar it has to fund future growth. However, if the company gets to the point where it’s generating enough cash ow to fund all its operations and its future growth, then the board of directors could declare a dividend, which would be distributed to all of the company’s shareholders based on their percentage of ownership.

From a historical perspective, there are certain industries that have very high dividend yields, which makes them extremely attractive to older investors looking for additional income to supplement their retirement income. For example, public utilities, oil and gas companies, and companies in the nancial services industry

between 1930 and 1945, the average dividend yield of the thirty stocks in the Dow was 14 percent, a truly staggering number in historical terms (today, the average dividend yield of the Dow is a mere 1.9 percent)

In practical terms, this meant that any investor during this time period who held on to the Dow and reinvested their dividends was doubling their investment every ve years, even if the Dow didn’t budge so much as an inch. The dividends alone were enough to do the trick.

the single greatest bookkeeping nightmare in the history of all bookkeeping nightmares: the Social Security Act. Suddenly, every company in America was legally required to keep track of every hour that every one of their employees worked, and then pay a portion of their wages to the federal government, which had to then gure out to whom, when, where, and how much to send back to each one of these employees when they nally turned sixty-ve and qualied for benets. In the end, there was only one solution: International Business Machines.

March 6, 1957. It was on this fateful day, a Wednesday, that Standard & Poor’s launched the world’s rst computer-generated stock index: the S&P 500.

Wall Street back in 1987. It happened over lunch at the Top of the Sixes restaurant

Wall Street takes companies public, nances their growth, provides liquidity to the markets, and analyzes companies to see which ones deserve more capital for growth and which ones don’t. In addition, Wall Street also facilitates global trade, maintains the currency markets, and works hand in hand with the Federal Reserve and the Treasury Department to keep the debt market moving and the economy trucking along.

“I’M WILLING TO BET ANYONE $500,000 that over ten years, an S&P index fund will outperform any hedge fund or collection of hedge funds that any of you can come up with. Any takers?”

The challenge was announced on May 6, 2006, at Berkshire Hathaway’s annual shareholder conference

Yet for some inexplicable reason, when it comes to investing there are many people who refuse to grow up. They hang on to the childish notion that there still might be a Wall Street Santa Claus, if they just believe hard enough.

investors are getting hit twice. “fund of funds” will use cleverly worded language in their marketing brochures to try to convince you otherwise

Longbets.com, which was the vehicle that was chosen to administer the bet.

ETFs do not allow you to automatically reinvest dividends, and mutual funds do. In this context, mutual funds are the preferred option, although there are certain circumstances that might make an ETF a better fit for you

Buett chose Vanguard’s 500 Index Fund Admiral Shares

“Jack Bogle has done more for the average investor than everyone else on Wall Street combined.”

in 2019, Warren Buett famously said, “If a statue is ever erected to honor the person who has done the most for American investors, then the hands-down choice should be Jack Bogle.”

Bogle wasn’t willing to pay them any sales commission at all, and the rest of the industry was paying 8.5 percent

Bogle created a shockingly seless structure, whereby the people who invested in Vanguard’s index fund became the owners of Vanguard. In other words, Bogle himself didn’t own the majority of Vanguard; his investors did.

interest on unpaid credit card balances is compounded daily.

Vanguard’s 500 Index Fund Admiral Shares, which I highly recommend, the annual fee is .04 percent

when the index rst launched in 1957, its composition was massively weighted towards industrial concerns, which, at the time, numbered 425 out of the total 500 companies, while healthcare, nancials, and information technology collectively accounted for only 17 companies. Today, of course, the weighting of the index is almost the exact opposite, with the three largest sectors being information technology, nancial services, and healthcare, and the once-dominant industrial concerns are now towards the bottom of the pack.

as the great general Hannibal said back in 218 BC, “Either we nd a way or make a way!” At the time, he was referring to crossing the Alps on the backs of elephants to launch a surprise attack on Rome.

if you decide to go with a mutual fund, then here are three excellent options that you can’t go wrong with:

Vanguard’s 500 Index Fund Admiral Shares Ticker Symbol: VFIAX

Fidelity’s 500 Index Fund Ticker Symbol: FXAIX

Schwab’s S&P 500 Index Fund Ticker Symbol: SWPPX

If you decide to go with an ETF, below are three highly recommended options with which you can’t go wrong:

The SPDR S&P 500 ETF Ticker Symbol: SPY

Vanguard’s S&P 500 ETF Ticker Symbol: VOO

iShares’ Core S&P 500 ETF Ticker Symbol: IVV

these types of divergent asset classes are referred to as being “uncorrelated,” in Wall Street parlance, with the most common example being stocks and bonds.

Occasionally they will move in the same direction at the same time, as they did in 2022. However, just to be clear, this blip in time was the exception to the rule. If you look at five-year time periods over the last hundred years, you won’t nd a single one when both the stock market and the bond market went down simultaneously for the period.

not putting all your eggs in one basket

you’re not just going to apply to one school; you’re going to apply to a bunch of schools to make sure that he gets into at least one, right? It’s simple logic. And the same is true with friendship. You don’t want to have just one best friend in your life and no other friends. Why? Because if something happens with that relationship, then you’ll have no one else to hang out with.”

“Anyway, I can go on and on with this, because it’s such a crucial point. I mean, take the Mormons, for example. Some of those bastards have three or four wives, and they all seem to be pretty happy about it. Not to mention all the evolutionary benets of having hundreds of millions of sperm going after one lonely egg…” And as I continued to share my thoughts on the biological virtues of Mormonesque polygamy, I watched my wife’s expression morph from confusion to bewilderment to downright hostility. Even worse, before I had a chance to stop her, she started translating my words for Gordita, with a vengeance.

A few seconds later, Fernando started laughing out loud.

you should have approximately 80 percent of your total portfolio there. The other 20 percent should go into a high-quality bond fund.”

“This assumes that you guys have sucient living expenses set aside in cash, in case of an emergency. You should have somewhere between six and twelve months. If you don’t, then you’ll have to carve that out of the 100 percent, and then split the remainder 80-20.”

For people without a family to support, six months is probably enough, but if you have a family, then you should probably increase that cushion to closer to twelve months. Anything more than that and you are probably playing it too safe, because if push comes to shove, you can always dip into the other assets in your portfolio

she had explained the lack of furniture to us in a rather comical way. She said, “If you turn me upside down right now and shake me, not a single penny will fall out!”

Notice how a 20 percent allocation into bonds reduces the portfolio’s average annual return by only .6 percent, while it reduces the maximum annual loss by over 8 percent. And a 40 percent allocation reduces the portfolio’s average annual return by only 1.3 percent, while reducing the maximum annual loss by 16.5 percent. Finally, a 60 percent allocation reduces the portfolio’s average annual return by only 2.2 percent, while reducing the maximum annual loss by 30 percent.

According to the great Jack Bogle, the general rule of thumb is to use your age as the guideline. In other words, if you’re thirty years old, then you should have 30 percent of your portfolio allocated towards bonds. If you’re forty years old, then it should be 40 percent.

It’s important to remember that you’re almost certainly going to have more than one nancial goal, and your asset allocation plan needs to accurately reect that. For example, your primary goal might be to save for your retirement, but you also might be looking for a down payment on a new house or to pay for your children’s college education. Or maybe you’re interested in starting a new business or simply spoiling yourself rotten by buying a new sports car or taking a trip around the world.

If any of those goals is less than three to ve years out, then you’ll denitely need to account for that by increasing your allocation of bonds relative to stocks.

In its worst year, 1931, the index lost 48 percent of its value as America fell into the throes of the Great Depression. Even worse, it had already lost 20 percent in 1929 and another 25 percent in 1930, for a total loss of 90 percent over that three-year period.

The same thing happened after the dotcom bubble burst in March of 2000. Over a three-year period, the tech-heavy Nasdaq lost 90 percent of its value, and the S&P 500 lost 50 percent of its value.

Now, just imagine if you had put all your money into stocks in the weeks leading up to the dot-com crash, and you had to pay for your daughter’s college education in twenty-four months, and then she got into Harvard. What would you say to her? “Oh, don’t worry, honey. The local community college is just as good!”

this one’s a true story—I’ve had multiple friends who’d decided not to pay any estimated taxes throughout the year and put the money into the stock market instead. Well, guess what happened? Yes, you got it. The stock market tanked that year, they couldn’t pay their taxes, and some grim-faced IRS agent came knocking on their door

the Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX) is a perfect solution for any investment portfolio with a time horizon of more than five years. With an expense ratio of only .05 percent, the fund holds approximately six thousand individual bonds of investment-grade quality with an average maturity date of ve years. If your portfolio’s time horizon is less than ve years, then the Vanguard Short-Term Bond Index Fund Admiral Shares (VBIRX) will be a much better t, although the average annual return is approximately 33 percent lower (2.19 percent for the VBIRX, versus 2.95 percent for the VBTLX)

For those of you who’d prefer a solution other than Vanguard, the SPDR Portfolio Aggregate Bond ETF (SPAB) and the Schwab US Aggregate Bond Fund ETF (SHCZ) are both excellent options for time horizons of ve years or more. For a time horizon of less than ve years, the SPDR Short-Term Corp Bond ETF (SPSB) and the iShares Core 1–5 Years US Bond ETF (ISTB) are much better ts.

A solid starter book with some history about Wall Street and their tricks. If you are looking for leveling up your strategies, then look somewhere else.

When I first saw this book at the bookstore, I assumed it wouldn’t offer much value—after all, I’m a finance student who’s already read a lot about investing and personal finance. Surprisingly, this book is not your typical finance or investing guide. Instead of focusing on technical concepts or the usual “school-taught” math, it takes a comical, refreshing approach. The author uses humor brilliantly to make complex topics accessible, and honestly, getting finance people to laugh is no small feat—he pulls it off effortlessly.

What stood out most is how the book breaks down the history and mechanics of Wall Street, revealing how the markets really work—beyond what university courses teach. One of the biggest takeaways for me was the shift in mindset: instead of hunting for undervalued stocks or trying to beat the market, the author convincingly explains (with plenty of wit and evidence) why passive investing, like simply buying the S&P 500, is the smartest long-term strategy. Even Warren Buffett agrees, and the book makes a strong case for it.

Reading this actually changed my approach: I’ve moved from active management to passive management, and I can already see the benefits. Beyond that, the book covers the origins of the Dow, exposes old fund manager scams, and makes you think twice about trusting the “pros.” Overall, this was one of the most entertaining and insightful finance books I’ve read. I highly recommend it for anyone—student or not—who wants to actually enjoy learning about how markets work.

This entire review has been hidden because of spoilers.

I truly can’t get enough of Jordan Belfort’s writing. His short, witty, at times offensive and raw style of conveying his message is incredibly comprehensible. It’s so easy to get trapped in his web of words and pull out the multitude of information he’s trying to get across. He clearly is well versed in finance and although this book may be the most powerful to a young investor or someone new to financial books, this was still a very interesting read and extremely useful to me. I particularly enjoyed the stock market history sections and his unique opinion on not getting f**ked by Wall Street; a service he once worked the front lines on and has firsthand experience. Who better to teach you how to not get taken advantage of by the finance world other than the convicted con man himself. Awesome.

As Stevo’s Novel Ideas, I am a long-time book reviewer, member of the media, an Influencer, and a content provider. I received this book as a review copy from either the author, the publisher or a publicist. I have not been compensated for this recommendation. I have selected it as Stevo's Business Book of the Week for the week of 1/7, as it stands heads above other recently published books on this topic.

Total left turn from what one would expect seeing the author, the cover and title. Worth reading once to beat home the point to DCA in to Vanguard index funds. Provides almost no new information and spends 3/4 of the book on the history of the stock market. Which..is probably best read on Wikipedia.

I had originally heard about this book from a podcast that Jordan was in. He spoke about what the average person can do in order to be financially successful later on in their life. He also pointed out all the bullshit out there when it comes to financial advice. I looked up what he was talking about and ended up seeing the research back up what he was saying. I ended up buying his book along with Psychology of Money and I think they do work well together. The Wolf of Investing in my opinion expands a bit of what Psychology of Money covers where Jordan explains what Wall Street is and why people aren't open to getting into the stock market and investing for their future. He also dives into the S&P 500 and a suggestion on what type of portfolio you should build for yourself.

People can say he was or is a total piece of shit for what he did long ago but the contents in this book really are more worth to a beginner and maybe someone who dove into stocks and either lost or gained a little. He explains a lot in a fun manner that you never want to put the book down. In all, if the description for the book interests you and you want to learn how you can invest in yourself and not fall for the traps of "financial advice" from some questionable people, I highly recommend this book. He does by the way go into the various ways to spot someone who will use you for their own financial gain and bleed all they can out of you before leaving you out in the dirt with nothing.

Obviously and please do this, do your own research and see more answers for yourself. Jordan Belmont and Morgan Housel (author of Psychology of Money) do communicate this, make sure you also know your margin of risk, all your debt is cleared, and you have saved enough funds for emergencies. Both cover this in their books and just be open to what they have to tell you. It has proven to make many people's retirement a happy one

Recenzie a cărții “The Wolf of Investing” de James Belfort

James Belfort oferă o combinație captivantă de umor și sfaturi simple despre investiții, care atât distrează, cât și educă. Limbajul său amuzant transformă conceptele financiare complexe în ceva accesibil, adesea adăugând anecdotă și replici incisive care mențin cititorii amuzați. Stilul său irreverențios transformă ceea ce ar putea fi un subiect plictisitor într-o conversație vie, ca și cum un prieten experimentat își împărtășește lecțiile dobândite.

Abordarea lui Belfort în privința investițiilor este surprinzător de simplă. El elimină jargonul și prezintă pași clari și aplicabili, pe care oricine îi poate înțelege, indiferent de background-ul financiar. Această claritate este unul dintre cele mai mari puncte forte ale cărții, permițând cititorilor să se simtă împuterniciți, nu copleșiți.

La baza “The Wolf of Investing” se află și căutarea lui Belfort de a-și răscumpăra greșelile trecutului. El recunoaște deschis problemele din trecut și consecințele acestora, prezentându-și filosofia de investiție nu doar ca pe o modalitate de a acumula avere, ci ca pe un mijloc de auto-reflecție onestă și de creștere personală. Prin împărtășirea călătoriei sale, el încurajează cititorii să abordeze investițiile cu integritate și autenticitate.

În concluzie, “The Wolf of Investing” este o lectură utilă pentru un viitor investitor, care îmbină umorul, simplitatea și utilitatea. Povestirea candidă a lui Belfort și sfaturile sale practice fac din această carte o lectură esențială pentru oricine dorește să navigheze lumea investițiilor financiare.

Honestly, I was surprised by how well the book is written. This is definitely one (other way, including the tons of classes he’s made about selling) of the ways he has redeemed with society, by telling the truth behind all of the Wall Street Fee Machine, and being honest on his advice. Additionally, I find so valuable how he gives a “For example…” after any technical concept being mentioned: he makes sure you are understanding everything. He definitely is a master at teaching. Also if you are kind of new in these topics, he makes sure to explain every detail of how investing works; since how the trade is made; to how the history behind it has caused the today’s financial system. Well done Jordan, I hope lots of people can read this book, it will turn into a MUST of the financial books in a couple of years.

There was a lack of citations to support the author's claims. He included graphs with unlabeled axes. He stated ETFs don't allow fractional share purchases which is incorrect since that can be done in Vanguard. That said, it was interesting to learn that the stock market recovered much earlier from the Great Depression than the official date due to deflation and other factors. Some jokes were forced but they were humorous. I liked the table comparing the short length of bear markets to the long length of bull markets which corroborated what I read in "Same As Ever". The author was correct that hedge funds have atrocious fees that eat away at profits and that stock and bond index funds/ETFs with low expense ratios are the best path to wealth; I liked that he included having 5% of one's wealth to speculate with for the risk-takers.

It’s sound advice that has been beaten to death at this point, however, always good to read anyway. Fundamentals never change and that’s what matters

Anyone looking for something new, are just speculating or doing high risk trading, with the next “hot stock” which might or might not work out. We hear of all the people that bought a certain company for .10 cents and sold it for 1000. But those stories just cloak the vast majority of people that tried something like this and lost all their money.

While the author is very well known for the movie depicting his character in real life, this book gives the readers some insights into what he thinks on how to make a fortune on Wall Street.

In short, he cited Buffet on how most funds can't beat the S&P500, we should just invest in a low cost index fund, and watch the magic of compounding.

I liked his honesty in the last chapter on Meet the F-ers. He goes on to give a very honest opinion on why those folks / entities he mentioned are bad for your investment journey.

This book tells you a lot about investing in the eyes of a beginner investor. In addition, tells you the positive overall benefit’s of being a S&P 500 investor. Specifically the index’s ability to compound if you buy it over your lifetime. The individual stories in the book aren’t particularly fascinating, but I can see how they fit into the storyline. If you’re new to investing and you want to learn how to make money over your lifetime in long-term trades, I would highly recommend this book. Long term trades are what make you generationally rich.

Jordan doesn't add much to the already existing swaths of financial literature advocating the slow lane path to wealth. As a matter of fact, Jordan did NOT get wealthy following the methods he teaches in this book: Investing in the S&P500.

There are better books that break down slow lane investing, such as "The Simple path to Wealth". If you'd rather not wait 40 years and have a foot in the grave to be wealthy, checkout MJ Demarco's "The Millionaire Fastlane".

The book is rife with profanity and lacks substantial content. The author condemns everyone on Wall Street, labeling them as charlatans, despite his own SEC conviction and a $3 million fine. The crucial advice distilled from this book to save time and money is as follows:

1. Invest in an S&P 500 index fund that has a historical return of 10%. 2. Allow your money to compound over the long term, spanning decades. 3. Consistently make additional contributions.

Really enjoyed this. Funny way of writing and references to the movie. Lots of details but simple explanations of financial terms and tools that everyone uses and talks about. It gives the history behind how things were created, why people use them, and how to approach investing our own money. It doesn’t go into full detail about everything but lots of examples why hedge funds and other people in the field will try to take your money and it gives reasons why and how to avoid the traps.

I thought this book would give me a lot of new insights on how Wall Street works and it really doesn’t. It made a lot of concepts more simple and I think that this book would be a good idea for those that want to familiarize themselves with the way the market works but overall I would recommend other books. I am a big fan of Jordan Belfort but this was just not it. 4/10.

Pretty decent book. The whole book could have been condensed to a chapter. Moral of the book is buy a low cost index fund, make sure you are properly diversified, and don’t touch your money. The rest of the book is for people who may want to be day traders.

Finally a book that explains real things about investing, not a crappy scam, its basic and introduction staff, but probably the real deal because most "investors" dont make more than the S & P 500 anyway.

The book doesn't "teach" you how to buy, sell, hold, etc. It's just some basic information. That's why this book is easy to read. Author made it a lil funny aswell. But that's about it. Fun book for beginners.

A fun and practical read — full of humour yet packed with no-nonsense advice. It shows the value of avoiding high fees, investing long-term across a broad range of stocks, and steering clear of cheaters.

The investment advice, though basic, is sound. The dialogue, when it was written in the third person, is pretty funny — see chapter 5. But by god did this book need an editor, as well as someone to correct the Spanish.

Entertaining and occasionally funny but financial advise is nothing new. He draws on his Wolf of Wall Street persona to provide an entertaining story and history of Wall Street. In the end the financi al advice is well known since Bogle.