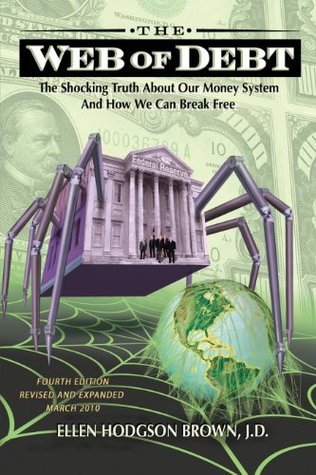

EXPLODING THE MYTHS ABOUT MONEY. Our money system is not what we have been led to believe. The creation of money has been privatized, or taken over by a private money cartel. Nearly all of our money is now created as loans advanced by private banking institutions -- including the Federal Reserve, the stock of which is 100% privately owned. Banks create the principal but not the interest to service their loans. To find the interest, new loans must continually be taken out, expanding the money supply, inflating prices -- and robbing you of the value of your money. Web of Debt unravels the deception and presents a crystal clear picture of the financial abyss towards which we are heading. Then it explores a workable alternative, one that was tested in colonial America and is grounded in the best of American economic thought, including the writings of Benjamin Franklin, Thomas Jefferson and Abraham Lincoln. If you care about financial security, your own or the nation's, you should read this book.

Never schooled in finance myself, I am admittedly not someone whose opinion you want to rely on in this matter. Nonetheless, I am offering it, for one reason: Since its 2007 publication, many of the alarming economic predictions in this book have come to pass exactly as described.

I don't suggest that Ms. Brown is a prophet -- virtually everything in her book is drawn from other sources (and scrupulously cited) -- but simply that she has got her facts straight. This being the case, her book should be read by anyone who wants a modicum of understanding of our global financial situation. It should also, I think, be required reading for everyone in the Legislature.

In reading this book, I was amazed at how coherently the monetary system could be described to a lay person. I'd never have guessed, from all the boring, jargon-filled discourses of our venerable "financial experts," that this was an issue that could be addressed in common sense language. And before anyone thinks I'm just some lay person who is delighted to understand SOMETHING about global finance and hasn't analyzed the data: I have in fact heard and read many arguments against the salient points in this book. I've also posted questions to some of them online -- in particular, about tallies and local currencies, two alternatives Ms. Brown mentions. I've been fascinated to see that no one so far has even acknowledged my questions, even though both tallies and local currencies have long been used with great success in many places in the world up to the present time. Instead, people more informed than I continue to call for "a return to the Gold Standard," a system guaranteeing scarcity and inflation, as far as I can see. It seems that the human urge to ignore "the Emperor's clothes" continues even into this current historic economic crisis. We humans hate considering a new paradigm. And so we continue along the old routes, keeping the major players in their jobs and the current structures afloat, despite their catastrophic track record and the alarming future staring us in the face.

I think it's worth pointing out that this book is strongly supported by world-renown economist Bernard Lietaer, among other high-profile financial and economic experts. These are people who know what they're talking about, and they believe Ms. Brown does, too. Some people may scoff at Ms. Brown, but I can't see how her supporters can be easily dismissed.

The information in this book needs to be common knowledge to every citizen of every country in the world. If the price of liberty is eternal vigilance, so is the price of financial freedom. The economic crisis did not start in 2008. Its roots are deep and far-spreading -- it is the logical result of a centuries-long systemic shell game. We could cut the taproot if we only identified it correctly. Then, with the right steps, we could create a flourishing garden. I wonder if we will ever do so.

There is a huge flaw in the world we live in and almost no-one talks about it. This book explains the monetary and banking system that enslaves us. In depth view to the history of banking, how we got to this point and what should we do about it.

Fairly easy reading. No excessive use of difficult terms. As an non-native english speaker I had no difficultues reading this book.

This is an excellent book to read if you want misleading, incomplete and confusing information regarding this history of banking and finance. Her core argument is that a fractional reserve banking system is dangerous and that the federal reserve system in the United States does not operate in the best interests of the citizenry - topics that could be effectively argued. But the author fails miserably in this poorly researched, confusingly-argued screed. On basic theory she is simply wrong. She confuses the gold standard and the gold currency standard. She gives simplistic explanations of specific financial crises that turn reality on its head. For example she argues that the inflation during Germany in the 1920's was caused by international short-selling of the currency, and not the deliberate and massive injection of large quantities of bank notes into the economy by the government in their effort to pay off the reparations from WWI. She finds conspiracy and cover-up in all corners of history. Any episode in history that benefits a particularly evil group of men, i.e. bankers - must have happened because of a giant conspiracy. Did you know that President Abraham Lincoln may have been shot as revenge for issuing Greenbacks that challenged the hegemony of the British banking cartel? She offers little evidence to back up these assertions, because they're conspiracies. Give me a break. The majority of her references are secondary sources that constantly juxtapose opinion and fact. For example, to confirm that the Federal Reserve is evil, she quotes congressmen and senators who say that it is evil. Knocked out that chapter before breakfast, eh Ms. Brown? The author also manages to cite Wikipedia - extensively - as a source. Blogs, political speeches, fellow conspiracy-theorists - these are passed off as factual sources. Classy, eh? The whole book has the feel that it was researched and written with a few Internet searches over the course of a few months. Any historical episode that promotes her "Federal Reserve = Bad" argument is thrown in the mix. You would need another book just to correct all the errors in this book.

This book suffers from a reliance on The Creature From Jekyll Island regarding it's history sections. It propagates the myth of The Russian Revolution being a Wall Street revolution which has no basis in actuality among other mistakes- I found myself crossing out passages and adding marginalia expressing dissatisfaction quite frequently. I'll applaud her however for making a good call for bank nationalization, and for keeping a bottom view of society. She is in favor of universal healthcare and infrastructure repair and rebuilding, but she still misses the whole mess: capitalism is an economic system based completely around debt. All she advocates is a relatively minor reshuffling of the system, and she yet retains that curious mystique of some type of constitutional purity.

Well-researched, interesting book, but in my opinion way too long. The most important factor of why government borrows money from private bank instead of issuing the money itself is not emphasized enough. Every human born is born under an obligation of government debt which makes that person a serf from the birth.

In my opinion, there should exist two banking systems in a country. The government banks which give money for useful development, and private system which should finance itself from wealthy individuals willing to extend credit to risky enterprises. Otherwise everything ends up the same. The private entity pockets all the profits, and taxpayer carries all the loses. We had this system in place for 600 years and its obviously NOT working.

We have put the fox in charge of the hen-house and the time to end it before complete collapse of our economic system is short.

Here are some basic facts.

The government of this country can, under the Constitution, issue money without going into debt to do so. It did so during the Revolutionary War and the Civil War. However, under pressure from wealth, the government has given up this power to the banks in what is called a fractional reserve lending system.

The Federal Reserve (the central bank of the United States) is not a government agency but a corporation of the banks who hold its shares.

When the government needs money to pay for the goods and services needed, instead of directly buying these goods and services from providers by paying in money that it can issue free of interest, it issues debt (bills and bonds) which it sells to the banks for bank-issued money, allowing the banks to make money on interest. This is allowing private profit out of thin air at public expense.

If you doubt that the dollar bills in your wallet are bank money, take one out and look at what it says on the face at the top - FEDERAL RESERVE NOTE - which means you are holding a piece of paper issued by the Fed, not the government.

Every time the U.S. government needs to pay for anything at all, it must either do so with tax income, which is bank money cycled through the productive economy into paychecks from which taxes are taken, or it must do so with borrowed bank money. This is how we have arrived where we are, with a towering debt to banks (both foreign and domestic) and a tax income that is hardly sufficient to pay the interest on that debt, let alone pay it off.

But it gets worse. With the debt the banks buy from the government, those banks can then create many times the amount (typically ten times the amount) and lend it out to the public, again for profit (interest). This money to lend is created out of thin air as bank accounting entries. Now you know how the amount of money in circulation can grow.

You might think it a good idea to keep track of how much money is in circulation, to know if there is too much (inflation) or too little (deflation) circulating. It would be good idea, but the Fed decided in 2006 to stop publishing that figure.

The fox in charge of the hen-house. The banks, who make profit from issuing money, are the folks charged with keeping tabs on that money so that too much is not issued. It is a recipe for disaster and that disaster, the "bust" in the boom and bust economic cycle has occurred repeatedly, including the Great Depression and the recent housing bust that has put America hopelessly in debt at all levels of government, in industry, and with private loans. The country is floating in a deep sea of debt. The system that brought that about remains untouched with a Congress captive to wealth unmotivated to change it.

Now you have the basic information any American citizen needs to understand the most colossal scam of all time - the independent, privately owned banking system of the United States.

Ellen Brown gives a complete picture of how America has arrived at our terrible financial position by starting at the beginning in the colonial days of the 18th century, reviewing the attempts to stop bank tyranny that were only temporarily successful but inevitably fell victim to the relentless drive of wealth to put the banks back in the driver's seat. The reader also learns how the banks, when their activities led to their own downfall, were propped up again and again with public funds.

Brown's writing is clear and concise, in sharp contrast to that in the book by Michael Hudson, "The Bubble and Beyond" that I have reviewed here. Concepts are made easy to understand, there is no needless repetition and the flow of the story of banking is maintained throughout. No essential topic is left unaddressed and Brown offers a comprehensive plan for getting out from under the banking system we have. This is not a doom and gloom book, but a powerful history lesson with a plan for a different future. The afterward that brings the story up through 2010 is a must read that naturally follows from the main text.

Sad to say, of all the candidates running for the presidency, only Bernie Sanders is talking about banking while in Congress only Bernie and Elizabeth Warren are on the banks case. This must change if we are to have hope for the American economy and to spark that change people need the education this book gives. There is no better mark than the person who has no idea what is being done to him or her.

“The real truth of the matter is that a financial element in the large centers has owned the government since the days of Andrew Jackson.” – Franklin D. Roosevelt

Ellen Hodgson Brown, J.D., is author of the recently published Public Banking Solution, but also the incisive and well documented The Web Of Debt – The Shocking Truth About Our Money System And How We Can Break Free. Her latter work is what will be covered lightly here.

For most of the modern world, money has been a staple of everyday life. A great deal of our daily functions revolve around this much used, but poorly understood economic tool.

In recent years, the monetary system has grown to untold levels. With the dollar losing value year after year, student loan debts reaching preposterous levels, and debt itself growing unabated in many different sectors of finance, it’s no wonder that the ‘too-big-too-fail’ economic system has its issues.

This is not to say a collapse is imminent as many alternative media pundits espouse. In fact, am more of the mind that what we are in fact in is what has been called a ‘controlled descent” by former Assistant Secretary of Housing and Urban Development, Catherine Austin Fitts.

Getting back on track, many of the above issues stem from our inherent corrupt monetary system. However, what this book does not cover is how the black-budget has been leeching money from the public sector, and transferring by the trillions [according to Ms. Fitts] to the black sector.

The modern birth of this [public] financial control grid is covered in extensive and mind-blowing detail in Brown’s Web Of Debt book. [Note: For a deeper analysis into the covert side of the off-the-books financial control grid, please take a gander at Joseph P. Farrell’s Covert Wars And Breakaway Civilizations – The Secret Space Program, Celestial Psyops and Hidden Conflicts.]

Pulling no punches, this historic piece has got gall. Not afraid to name names, and branching through centuries of historical data, Brown’s work showcases what the financial, political, and elite minds of these times were pondering.

This particular piece also offers data/ideas on some of the vital issues we face and how we might overcome said issues.

From the inception to the private, and heinous Federal Reserve, up to current times, the reader will get ample evidence of the financial mishaps/crimes that are taking place. This is important, because much of the populace is unaware of these dealings.

If you wish to know the truth about our financial monetary system, the truth about its wide-ranging and sinister history, and ways in which to enrich your knowledge on this esoteric subject, then this book is definitely for you.

This is a book that everyone in the USA should read. It gives extensive history of our monetary system and how it has been usurped by the bankers. It also gives some very good and well researched alternatives for us to make currency into a tool that can assist mankind instead of enslaving them.

Ellen Hodgson Brown makes the whole story interesting with a great writing style as well as by bringing to light the whole monetary allegory that is behind the all American fairy tale The Wizard of Oz.

Possibly the most important single book of the last 50 years. Who knew anything about the struggle between banks and people that has been underway throughout the history of this country? This book offers a history of money in the U.S... where it comes from, why it matters and what should be done about it.

An amazing portrayal of the debt system in America told in a well-researched story that correlates to Frank Baum's Wonderful Wizard of Oz. I'll let you decide if it's based in conspiracy or truth.

Definitely the best book I have ever read pertaining to the unsustainable debt of the United States of America, and the world.

Highly detailed, and masterfully written!

I highly recommend this book to any and all of my fellow finance geeks. It truly reveals the wreckless path we are headed down, and cleary explains in detail the doom that it will bring upon us all if we don't correct course soon.

Wow! Is this ever a great look at the underpinnings of our stinking financial quagmire. I had no idea that the "Wizard of Oz" was based completely on the financial drama of its day but Ellen pulls meaningful quotes from it throughout her book to highlight the salient issues. This is a fantastic piece of research. Ellen has pulled together financial interests, tied them to historically significant events in world history and suddenly all the murky motives and ill-conceived logic of the past is revealed. The only reason I don't give this book a 5 star rating is because it seems to reiterate the same facts and dwells on some material longer than I thought relevant. Overall I believe this should be required reading for every single person in the world and if you are illiterate you should find someone to read it to you.

Really good book and probably a companion or follow-on book to the Creature from Jekyll Island. It explains the context of Baums's book The Wizard of Oz as a fight against the progressives and the bankers in the late 1800's and early 1900's. And while doing so, explains quite a bit about our money system and why we're in the problem we are now. There is a lot of reference material for which you can checkout. It also spends some effort toward the end of the book to present alternative ideas to money as debt too. Not pure Austrian, Chicago, or even Keynesian, it covers all them in some sprinkling of what happens in our monetary system.

Well worth the read just to help give you a clue on how we got here.

If governments and countries are at the mercy of the money cartels, how can changes be effected? Hodgson Brown paints a big and grim picture in this book and recommends changes in her next one, on Public Banking. Luckily, in this book, she does give some examples of people and places that have side-tepped the crooked global monetary system, or we will really feel despair after reading it. When I read writings like these, I realize why in history, revolutions occur.

It's a great insight into the banking mafia that is trying to control the whole world. Great peaces of history and facts also.

Idea that money should be created by the government and municipality is a miss. It just can't work because it doesn't stop corruption and human greed. No mention of the assymetrical informations problem and lack of transparency.

Hope the author does more research and write another one right.

a friend sent this to me & like another reviewer I found it seemed a bit muddled at first but realized it's possibly the result of gathering a number of related articles or essays.

This is a good read, though, for someone looking to learn about the history of how the US monetary system works, and what the future can look like if we can change it (and what the future will be like if we don't)

Very interesting read regarding the history of money & how the money system works in modern society. Although I suspect parts of this book is speculation / educated guessing, it certainly challenged my view of government & the idea of larger governing organizations for world power.

Great book. Once read, you will never look at our financial institutions in the same way. Great tie ins with the Wizard of Oz. A pity more people haven’t paid attention to the man behind the curtain.

A reasonably interesting history of the Federal Reserve is spoilt by a flawed argument, extensive repetition and the widespread use of Wikipedia as a source material. Wikipedia. Seriously.

Really dense but with a lot of good content, if you have the time to shift through it all.

The first few hundred pages of the book lays the foundation for the subject matter further into the book; how fiat currency was first formed in the United States, the struggles that Andrew Jackson had against the formation of a central bank, the shift from bimetallism to the gold standard, the Great Depression, the dollar being taken off the gold standard and the current economic climate of spiralling federal debt with each subsequent recession.

Although mainly America-centric, it does pop into the world economic situation on occasion, which brought an interesting concept to me of one of the main reasons for the Chinese economic miracle of the 1980s/90s was because they weren't balancing their books, the reason being that so long as the money stays inside China then the CCP is happy to let money go down the hole in a business.

It then moves onto proposal section, seeking to resolve the federal debt through a horde of radical monetary policies, including several against the cancerous derivatives market, that it proposes will eventually trickle away the need for an income tax.

As I said, it is a dense tome with a lot of content to sift through, but still pretty interesting for the time it was written.

ESSENTIAL READING if one is sincerely working to comprehend the American ( thus Global ) experience of 'Monied Capital' & the History of 'Financial Intere$t$'.

The correlation and basically unknown ( at least to those I would talk to about the book 2010-2017 ) metaphorical representations of Frank L. Baum's "Wizard of OZ" to the story of The Federal Reserve Banking System,

Which tied together a profound weaving of the narrative of the Development of the Monetary $ystem.

Read this Book in order to develop an insight into how we can become more Economically Literate in order to NOT BE FOOLED BY THE BOURGEOI$ CLA$$ & THE DOMINANT CULTURE OF COMPLICITY...........

There's just a few things to get out of this book, the federal reserve is private, money is created out of thin air, the government (and everyone) is in debt and wall street is a huge casino. Other than that, the author starts from an incorrect foundation, with wrong details on the history as well as the how/why of the monetary system therefore her conclusions (or solutions) are inherently wrong. I recommend reading the following book for accurate history, details and a correct explanation of the whole system: "Money, Bank Credit, and Economic Cycles" by Jesus Huerta de Soto.