What do you think?

Rate this book

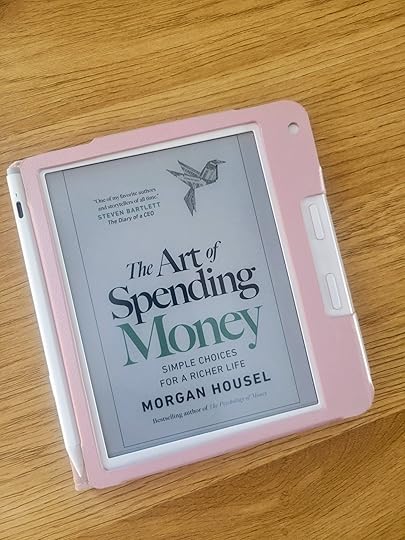

288 pages, Paperback

First published October 1, 2025

"People sometimes think they're buying something nice because it will make their life more pleasant, comfortable, interesting, or fulfilling. But unknowingly what they're paying for is a chance that other people will look at them, ideally in a positive light."

"The highest use of money is to use it to control your time, granting freedom and independence, and living life the way you choose."