Beni Rusani's Blog

November 15, 2024

Berita dari saya – The Journey continues

Salam hormat kepada Tuan & Puan yang mungkin juga menerima rawatan & follow up bersama saya di Hospital IJN.

Saya ingin berkongsi satu berita penting. Saya telah berusaha untuk memaklumkan perkara ini kepada beberapa pesakit semasa di klinik, tetapi saya sedar tidak semua dapat dimaklumkan secara peribadi. Oleh itu, saya mengambil peluang ini untuk berkongsi maklumat ini dengan anda yang mungkin ada mengikuti saya di media sosial.

Di sini saya ingin maklumkan bahawa hari terakhir saya di IJN adalah pada 17 Disember 2024.

Mulai 1 Januari 2025, saya akan mula bertugas di KPJ Damansara Specialist Hospital 2 (DSH2), di Petaling Jaya.

Di hospital DSH2 saya akan menyertai barisan doktor pakar jantung Dr. Daud Sulaiman & Dr. Lee Zhin-Vin dan doktor pakar bedah jantung Prof Dr. Shahrul Amry.

Selain jantung disini juga ada beri rawatan untuk sistem2 lain seperti pernafasan respiratori (Dr Arif), ENT (Dr Rajveer, Dr Sazafi), O&G, mata, kanak-kanak, tulang dan lain2.

Sekiranya Tuan & Puan ingin meneruskan temujanji & rawatan bersama saya: Sila maklumkan kepada saya melalui “direct message” di Instagram, Twitter atau e-mel saya di benirusani@gmail.com sebelum 17 Disember 2024  – Btw Pastikan di bahagian DM, dan bukan di ruangan komen. Info anda adalah privasi.

– Btw Pastikan di bahagian DM, dan bukan di ruangan komen. Info anda adalah privasi.

Sekiranya Tuan & Puan ingin untuk kekal menerima rawatan di IJN: anda tidak perlu mengambil sebarang tindakan. Mulai 1 Januari, sistem secara automatik akan menetapkan anda kepada doktor baru yang akan meneruskan rawatan anda.

Di sini saya juga ingin mengambil kesempatan ini untuk memohon maaf sekiranya terdapat sebarang kekurangan di pihak saya.

Terima kasih kerana memberi kepercayaan kepada saya selama ini untuk menjadi sebahagian daripada penjagaan kesihatan anda. Saya mendoakan tuan & puan kekal sihat dan sejahtera di masa hadapan.

Salam hormat,

Dr. Ben

Tuan & Puan juga boleh follow DSH2 di social media — dan juga boleh memilih tarikh follow up secara atas talian di https://www.kpjhealth.com.my/damansara2/.

Saya rasa slot online appointment untuk klinik saya akan di mula di buka pada penghujung December.

Cara ke DSH2 –> GOOGLE MAP:

Di rasmikan oleh Yang di-Pertuan Agong Kebawah Duli Yang Maha Mulia Seri Paduka Baginda Yang di-Pertuan Agong Sultan Ibrahim, pada May 2023.

Di rasmikan oleh Yang di-Pertuan Agong Kebawah Duli Yang Maha Mulia Seri Paduka Baginda Yang di-Pertuan Agong Sultan Ibrahim, pada May 2023.

Hospital KPJ yang ke-29. Kini KPJ Healthcare mempunyai lebih 3700 katil di seluruh negara.

Hospital KPJ yang ke-29. Kini KPJ Healthcare mempunyai lebih 3700 katil di seluruh negara.

DSH2 mempunyai kapasiti 300 katil. 7 dewan bedah, 10 katil ICU, dan 54 klinik konsultasi.

DSH2 mempunyai kapasiti 300 katil. 7 dewan bedah, 10 katil ICU, dan 54 klinik konsultasi.

Kawasan seluas 670,785 kaki persegi

Kawasan seluas 670,785 kaki persegi Di sebelah lebuhraya LDP. Berdekatan Mont Kiara, Taman Tun, Mutiara Damansara & Desa Park City.

Di sebelah lebuhraya LDP. Berdekatan Mont Kiara, Taman Tun, Mutiara Damansara & Desa Park City.  Bangunan 11 tingkat bersama 4 basement parking. Mula di buka sejak September 2022.

Bangunan 11 tingkat bersama 4 basement parking. Mula di buka sejak September 2022.

DSH2 features a state-of-the-art medical facility, including advanced technologies such as Da Vinci Surgical system, Magnetom Lumina MRI machine Somatom Dual Source CT Scanner, Azurion B20/15 Angiography machine for precise navigation, and Hologic Selenia Dimensions 3D Mammography machine among others.

DSH2 features a state-of-the-art medical facility, including advanced technologies such as Da Vinci Surgical system, Magnetom Lumina MRI machine Somatom Dual Source CT Scanner, Azurion B20/15 Angiography machine for precise navigation, and Hologic Selenia Dimensions 3D Mammography machine among others.

July 26, 2024

“You kena start dialysis sebab buah pinggang dah rosak.”

Hi readers, biasanya orang hospital panggil penyakit buah pinggang ni CKD, nama penuh dalam kad pengenalan = Chronic Kidney Disease iaitu penyakit buah pinggang kronik.

Ramai ke orang Malaysia ada CKD?Ramai gak la. Setiap 15 dari 100 orang yang anda jumpa di KL Sentral ada CKD. Sebab ramai orang kita ada kencing manis dan darah tinggi. Kencing manis jer adalah penyebab lebih 50% kes dialysis. Mana taknye kedai jual makanan melambak sampai ke pagi. Semua pakat nak overweight dan kurang exercise.

Rawatan hemodialysis: kena pegi pusat dialysis cuci darah 4 jam, 3x seminggu. Sehingga bila2. Nak pergi ke tanah suci atau melancong memang susah. Kos dalam RM2,000 – 2,500 sebulan. Macam mana nak check CKD?

Rawatan hemodialysis: kena pegi pusat dialysis cuci darah 4 jam, 3x seminggu. Sehingga bila2. Nak pergi ke tanah suci atau melancong memang susah. Kos dalam RM2,000 – 2,500 sebulan. Macam mana nak check CKD?Untuk check CKD, cara standard adalah check darah yang dipanggil eGFR (biasanya dalam ujian renal profile). eGFR beri anggaran sejauh mana buah hati pinggang anda menapis darah. But, ramai yang tak sedar bahawa ujian ini sahaja tak cukup.

Satu lagi ujian penting yang harus di buat adalah UACR (Urine albumin creatinine ratio). Walau eGFR sukat fungsi buah pinggang, UACR pulak ukur jumlah albumin (sejenis protein) dalam air kencing. Tahap albumin yang tinggi dalam air kencing boleh menjadi tanda awal kerosakan buah pinggang, walaupun tahap eGFR masih normal.

Apa Nilai Normal UACR?Nilai normal UACR sepatutnya kurang daripada 30 mg/g (kalau makmal di IJN pakai 3 mg/mmol). Kalau lebih buah pinggang anda mungkin ada problem

KesimpulanMenggunakan kedua-dua ujian eGFR dan UACR untuk periksa CKD adalah penting untuk kesan CKD. Tengok carta di bawah.

Cari warna kotak anda: Carta ni dari garis panduan KDIGO (satu organisasi badan buah pinggang sedunia). Padankan nilai UACR & GFR dan check tafsirannya di bawah kotak. Biasanya, G4 dah kena jumpa doktor buah pinggang (nephrologist) dan G5 tu dah start dialysis.

Cari warna kotak anda: Carta ni dari garis panduan KDIGO (satu organisasi badan buah pinggang sedunia). Padankan nilai UACR & GFR dan check tafsirannya di bawah kotak. Biasanya, G4 dah kena jumpa doktor buah pinggang (nephrologist) dan G5 tu dah start dialysis. Untuk bacaan lanjut, anda boleh click link ni –> Persatuan Buah Pinggang Malaysia.

Kongsikan pendapat dan soalan anda di ruangan komen di bawah. Sehingga berjumpa lagi, jaga diri!

PS: BTW, cuba tanya agent Takaful kalau anda masih boleh apply Medical card atau Critical Illness kalau anda dah ada CKD (kalau masih boleh, ada syarat ke eg. setakat level / warna kotak mana di atas?”

Anda baca sampai habis? Saya beri bonus link –> tempat percuma nak check CKD free di Malaysia.

Salam mesra,

Dr. B

July 13, 2024

Raiz Australia tarik diri.

Hi guys,

I am sorry. Nampaknya blog post terbaru saya mengenai Raiz Invest last week was 5 minutes too late and Elvis had left the building, kerana syarikat induk dari Australia telah memutuskan untuk menarik diri daripada kenderaan pelaburan ini selepas empat tahun menjalankan perkhidmatan di Malaysia — alasan yang mereka beri adalah nak fokus kat negara mereka.

Namun, menurut Permodalan Nasional Berhad (PNB), rakan kongsi Malaysia dalam projek ini, mereka telah meyakinkan semua pelabur untuk bertenang kerana mereka akan memastikan peralihan yang lancar ke peringkat seterusnya, walaupun mereka belum menjelaskan secara terperinci.

Bagi mereka yang merancang untuk melabur dalam Raiz, nasihat saya adalah untuk mempertimbangkan platform lain seperti Versa, atau broker seperti Moomoo, untuk melabur dalam pasaran saham pilihan anda, sama ada di Bursa Malaysia atau di Amerika Syarikat. Moomoo mungkin lebih menjimatkan kerana tiada caj bulanan untuk menguruskan akaun anda.

Di bawah adalah screenshot FB post on Raiz Malaysia/PNB.

Untuk mengelakkan sebarang kekeliruan saya pun dah tarik balik blog post saya on Raiz yang saya post minggu lepas.

As they said, “Nothing is certain in life except death & LHDN.”

July 5, 2024

Melabur serendah RM5.

Hari tu ada yang tanya saya di Instagram selain dari Versa ada ke pilihan lain?

Jawapannya: Ada… RAIZ.

Straight to the point saya rasa Raiz ni senang diguna untuk mereka yang nak cuba test try dunia pelaburan secara kecil-kecilan. Jangan tersilap dengan Rize yang adalah bank digital macam GX tu.

Dulu saya keliru jugak tapi lepas tengok klip ni — baru saya faham, tekan sini YouTube:

Apa Itu Raiz?

Apa Itu Raiz?Raiz adalah pelaburan mikro (maksudnya pelaburan boleh di buat dalam jumlah kecik2 seperti secara round-up (baca bawah) dan dengan jumlah yang kecil serendah RM5). Ia berasal dari Australia dan kini telah bertapak di Malaysia.

Selamat ke Raiz ni?Raiz ni berdaftar dengan Security Commission Malaysia (License eCMSL/A0363/2020) — kalau nak tahu lebih lanjut boleh tekan sini. Maksudnya kalau Raiz ni nampak dodgy dan unsur2 scam maka tak dapat lesen SC. Dan ia bekerjasama dengan Permodalan Nasional Berhad (PNB) — yup badan yang uruskan ASB kita; dan Raiz Invest Limited, sebuah syarikat yang disenaraikan di bursa saham Australia.

Oh ya Halal ke?Macam melabur di ASB juga – hukumnya Harus bagi Muslim Investor.

Ciri-Ciri Unik RaizPembulatan (Roundups): Raiz kasi kita chance untuk labur duit baki lebihan masa shopping. Contohnya, jika anda beli kopi harga RM4.50, Raiz akan membulatkan jumlah tersebut kepada RM5 dan melaburkan lebihan RM0.50 ke dalam akaun Raiz anda. Seolah2 mcm Opportunistic investor:Contoh: Saya beli kopi pakai credit card Maybank yang saya link kan dengan Raiz.Bila dah “dapat angka genap” — Raiz akan ambil duit melalui debit kad yg saya yang link dgn akaun simpanan di bank contoh: akaun simpanan di Maybank (banyak pilihan bank lain) akan transfer RM0.50 dari my savings account ke tabung Raiz saya.Pelaburan Berterusan: Anda boleh menetapkan pelaburan berulang setiap hari, minggu, atau bulan mengikut keselesaan anda.Maklumlah kita ni kadang2 lupa.… dan banyak kerja lain lagi.Jenis PortfolioKalau anda tak nak pening2 kepala, Raiz dah siapkan siap-siap beberapa portfolio yang anda boleh pilih. Setiap portfolio ni ada tahap risiko yang berbeza:

Konservatif: Portfolio ini sesuai untuk mereka yang tak suka risiko tinggi. Ia banyak melabur dalam bon Islam (sukuk) dan aset yang stabil.Sederhana (Moderate): Portfolio ini adalah gabungan antara aset yang stabil dan saham yang mempunyai potensi pertumbuhan. Sesuai untuk pelabur yang boleh ambil sedikit risiko.Agresif: banyak di laburkan dalam saham (stocks) seperti Microsoft, Adobe etc.Anda nak customize pun boleh. Ini contoh Portfolio Agresif: Portfolio ini mengandungi peratusan % besar dalam saham dan aset yang risiko tinggi. Sesuai untuk pelabur yang mencari pulangan yang lebih tinggi. Kat sini Islamic World Equity mereka dah set 55% dan sukuk 5% (Kalau you pilih konservatif nilai ni akan terbalik).

Ini contoh Portfolio Agresif: Portfolio ini mengandungi peratusan % besar dalam saham dan aset yang risiko tinggi. Sesuai untuk pelabur yang mencari pulangan yang lebih tinggi. Kat sini Islamic World Equity mereka dah set 55% dan sukuk 5% (Kalau you pilih konservatif nilai ni akan terbalik).

Anda juga boleh semak apa kompeni2 yang ada dalam tabung2 ni — ini contoh kompeni2 dalam “abrdn Islamic World Equity”. Trivia: kenapa nama pelik abrdn, sebenarnya ia berasal dari Aberdeen – sebuah bandar di Scotland.

Anda juga boleh semak apa kompeni2 yang ada dalam tabung2 ni — ini contoh kompeni2 dalam “abrdn Islamic World Equity”. Trivia: kenapa nama pelik abrdn, sebenarnya ia berasal dari Aberdeen – sebuah bandar di Scotland.

Anda nak customize pun boleh: Kita boleh ubah portfolio ikut selera. Ini bolehkan kita untuk pilih aset yang kita percaya akan beri pulangan terbaik. Katakan kita nak Nomura 40% saham semiconductor — kita boleh scroll & pilih berapa % yang kita nak. Ini contoh saya punya sebab saya anggap semiconductor ni ada potensi besar dalam dunia AI yang tengah rangup krup krup (psst NVDIA, AMD) Kalau Aiiman Growth tu ada Tenaga Nasional, TIMEdotCom. Dan Global Balance ada Apple, Amazon. Jadi apa keuntungan yang saya dah dapat setakat ni?

Anda nak customize pun boleh: Kita boleh ubah portfolio ikut selera. Ini bolehkan kita untuk pilih aset yang kita percaya akan beri pulangan terbaik. Katakan kita nak Nomura 40% saham semiconductor — kita boleh scroll & pilih berapa % yang kita nak. Ini contoh saya punya sebab saya anggap semiconductor ni ada potensi besar dalam dunia AI yang tengah rangup krup krup (psst NVDIA, AMD) Kalau Aiiman Growth tu ada Tenaga Nasional, TIMEdotCom. Dan Global Balance ada Apple, Amazon. Jadi apa keuntungan yang saya dah dapat setakat ni?

Jika anda tertanya2 apa hasil saya. Ini hasil pelaburan saya untuk 3 bulan. Ada RM21.14 atau 2.82%. Itu pun saya ada tukar2 portfolio 2x (saja nak test try). Expert cakap kalau kita tak selalu tukar portfolio akan dapat lebih banyak hasil.

Jika anda tertanya2 apa hasil saya. Ini hasil pelaburan saya untuk 3 bulan. Ada RM21.14 atau 2.82%. Itu pun saya ada tukar2 portfolio 2x (saja nak test try). Expert cakap kalau kita tak selalu tukar portfolio akan dapat lebih banyak hasil.

Masa mula2 masuk saya pilih custom, pastu ambik aggressive, tapi selepas 1 bulan tukar balik ke CUSTOM. Ini Pecahan peratus % custom yang saya pilih sendiri.

Masa mula2 masuk saya pilih custom, pastu ambik aggressive, tapi selepas 1 bulan tukar balik ke CUSTOM. Ini Pecahan peratus % custom yang saya pilih sendiri.

Ini adalah pecahan RM ikut peratus % tadi. So transparent jugak le Raiz ni.

Ini adalah pecahan RM ikut peratus % tadi. So transparent jugak le Raiz ni.

Mereka pun ada bagi Dividend dalam bentuk REWARD.

Mereka pun ada bagi Dividend dalam bentuk REWARD.

Ni contoh akaun saya. Yang paling atas tu PENDING: RM10.26, beli barang pakai kredit card, pastu tengah tunggu kelulusan bank untuk masuk duit dari akaun saving (secara auto). Yang jumlah RM25 tu saya set kan auto setiap minggu — nak set RM5 pun boleh.

Ni contoh akaun saya. Yang paling atas tu PENDING: RM10.26, beli barang pakai kredit card, pastu tengah tunggu kelulusan bank untuk masuk duit dari akaun saving (secara auto). Yang jumlah RM25 tu saya set kan auto setiap minggu — nak set RM5 pun boleh.

Nak taruk lump sum pun boleh, serendah RM5.Kesimpulan

Nak taruk lump sum pun boleh, serendah RM5.KesimpulanRaiz adalah platform pelaburan yang sesuai bagi kita yang ingin mencuba dunia pelaburan. Dengan yuran yang berpatutan, pelaburan mikro, dan pelbagai jenis portfolio yang ditawarkan, Raiz beri kita chance untuk kumpul tabung pelaburan secara beransur-ansur.

Contoh mcm mana nak setkan setiap minggu (atau bulanan) ikut kemampuan. RM5 pun boleh.

Contoh mcm mana nak setkan setiap minggu (atau bulanan) ikut kemampuan. RM5 pun boleh.

Kalau anda nak buka tabung untuk anak2 anda, mana tau by the time dia masuk kolej, dah lepas yuran belajar. Tak perlu ambil pinjaman PTPTN

Kalau anda nak buka tabung untuk anak2 anda, mana tau by the time dia masuk kolej, dah lepas yuran belajar. Tak perlu ambil pinjaman PTPTN

Ada program reward kalau anda beli barang2 kat kedai2 ni melalui Raiz,

Zalora pun ada

— contoh jer ni, banyak lagi kedai lain. Kedai tu akan laburkan beberapa % ke dalam tabung anda

.

Tengok contoh MAS di bawah.

Ada program reward kalau anda beli barang2 kat kedai2 ni melalui Raiz,

Zalora pun ada

— contoh jer ni, banyak lagi kedai lain. Kedai tu akan laburkan beberapa % ke dalam tabung anda

.

Tengok contoh MAS di bawah.

Contoh kalau beli flight MAS, baca kat situ apa MAS tulis. Yuran dan Kos

Contoh kalau beli flight MAS, baca kat situ apa MAS tulis. Yuran dan KosRaiz mempunyai struktur yuran yang saya anggap berpatutan:

Yuran Bulanan: RM1.50 sebulan jika baki akaun anda di bawah RM6,000.Yuran Pengurusan: 0.3% setahun jika anda ada baki akaun RM6,000 ke atas.Yang boleh saya simpulkanRaiz adalah platform pelaburan yang sangat sesuai untuk mereka yang ingin mencuba dunia pelaburan. Secara ringkas antara best Raiz ni (yang feature kat bawah ni anda boleh pilih, kalau tak nak pun tak mengapa):

Automatik invest melalui ’round-up’ dari perbelanjaan harian yang guna credit card.Auto invest ikut kemampuan anda. Nak set up setiap hari / minggu / bulan.Raiz Rewards: Jika berbelanja dengan kedai2 tertentu mereka akan invest back certain % to your tabung invest (setiap kedai berlainan). Contoh beli flight ticket dgn MAS. Boleh mula kan tabung invest untuk anak2 Jika anda rasa anda nak cuba RaizAda tawaran hebat buat masa ni RAIZ akan beri kita berdua RM5 setiap seorang jika anda guna link saya ni — tekan link di bawah:

https://links.raiz.com.my/btSQYc8odpRCoxJ28

Hanya ikut je steps di web page itu. Good luck and melabur lah untuk masa hadapan kita.

Okay cukup setakat itu buat kali ni. Kita jumpa lagi Insya-Allah.

Okay what it actually means is Pelaburan adalah seperti menanam pokok.

Okay what it actually means is Pelaburan adalah seperti menanam pokok. The best time to plant a tree was 20 years ago. The second-best time is now.”

PS: This is not a sponsored article. Although I am waiting for one. Ehem.

Dan seperti biasa setiap artikel berkenaan pelaburan mesti disertai dengan Disclaimer dj bawah:

“Maklumat ini hanya untuk tujuan perkongsian semata2 dan tidak sepatutnya dianggap sebagai nasihat pelaburan kewangan profesional. Prestasi lepas tidak menunjukkan keputusan masa depan. Sila buat penyelidikan sebelum membuat keputusan pelaburan.”

June 17, 2024

Persiapan masa depan kita.

Pertamanya, saya suka kongsi benda baru yang saya belajar (so I can remember it better) hence maybe saya akan tulis 2-3 lagi post on finance from POV of a non-financial person.

Okay let’s begin.

Kita selalu dengarkan penggunaan ‘main saham’ di kalangan orang Malaysia kita ni — contohnya “eh sejak bila ko main saham?”

Saya sebenarnya tak berapa gemar expression main saham, pada saya stocks investment is not a game. Silap hari bulan ada juga berbaur negatif ala2 seperti main judi. Kita kena terapkan pada anak2 muda kita bahawa pelaburan adalah suatu benda positif yang berpotensi menjana ekonomi orang Malaysia. Kalau besok saya naik, besok harga minyak turun. Eh.

Okay2 but this is a serious matter. We should not invest into something we do not understand, tapi saya juga percaya bahawa untuk memahami sesuatu, kita perlu melakukannya. Sebanyak mana pun kita membaca, kita tak akan faham betul2 apa jua subjek dalam dunia ni. And the only way is to get our feet wet.

Saya rasa VERSA ni memberi orang2 awam yang beginner macam kita yang takde formal investment/financial background untuk berjinak-jinak dengan dunia pelaburan.

So, kali ni saya nak share pengalaman saya belajar melabur di pasaran antarabangsa seperti U.S.A & Eropah sambil masih menggunakan Ringgit Malaysia (MYR).

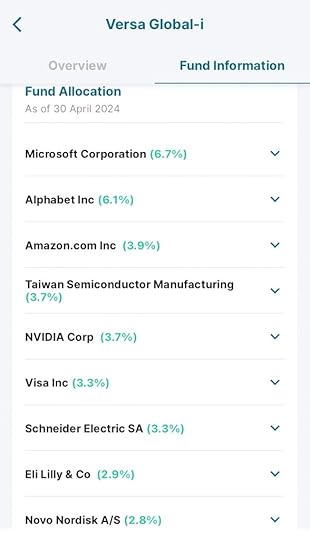

Maksudnya saya dah boleh melabur dalam syarikat2 global terkemuka seperti Microsoft, Apple, Amazon, dan NVIDIA. Eli Lilly pun ada!

List ni hanya top 10 holdings. Bermaksud kalau kita masuk kan RM100. Fund manager akan pecah2 kan ikut % dalam carta di atas: contoh 6.7% = RM6.70 di laburkan dalam Microsoft. 3.9% = RM3.90 ke dalam Amazon dan seterusnya.

List ni hanya top 10 holdings. Bermaksud kalau kita masuk kan RM100. Fund manager akan pecah2 kan ikut % dalam carta di atas: contoh 6.7% = RM6.70 di laburkan dalam Microsoft. 3.9% = RM3.90 ke dalam Amazon dan seterusnya.Tapi sebelum tu saya nak cerita yang sebenarnya VERSA ni ada 3 produk asas, kalau anda masuk app dia nanti anda akan nampak 3 benda ni (lihat gambar bawah kucing tu)

1. Save

2. Invest

3. Retirement

*Produk Save (simpanan) adalah yang saya mentioned dalam post saya baru-baru ini iaitu Money Market Fund. Produk Retirement (persaraan) ni adalah PRS, ia macam EPF tapi swasta, anda boleh abaikan buat masa ini.

Dalam post ni saya nak cerita kategori “Invest” iaitu pelaburan.

Dan dalam kategori Invest ni pula ada banyak tabung yang anda boleh pilih, seperti:

Jadi Apa Itu Versa Global-i?

Versa Global-i ialah tabung pelaburan unit amanah (unit trust) yang diuruskan oleh AHAM Capital (dulunya dikenali sebagai Affin Hwang) dengan nama tabung yg dipanggil AHAM Aiiman Global Multi Thematic Fund. Kalau nak kaji tabung ni dengan lagi detail boleh klik website ni. Yang pentingnya ia patuh syariah & bertujuan untuk memberi pelabur peningkatan modal (Capital gain) dalam jangka sederhana hingga panjang (biasanya 5 hingga 10 tahun).

Di ambil dari Annual report.

Di ambil dari Annual report.Kenapa saya Pertimbangkan Versa Global-i?

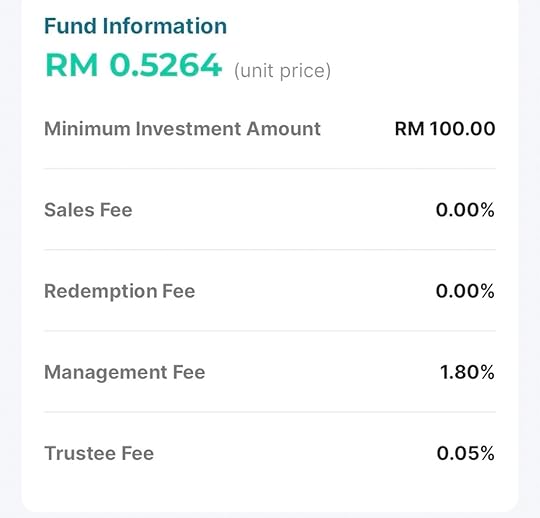

Saya miliki sebahagian Syarikat Gergasi Global: Dengan Versa Global-i, kita boleh cakap yg kita ada pegangan dalam syarikat ehem2 “Yeah we own a piece of that company.” Saya tak Perlu Pantau Setiap Hari: Saya tak perlu risau tentang memantau pasaran saham setiap hari sebab ada banyak lagi kerja lain nak buat. Pengurus dana di AHAM Capital akan buat kerja berat untuk kita. Mereka menilai pasaran dan memutuskan syarikat mana yang patut dimasukkan dalam dana, jadi kita boleh melabur dengan selesa tanpa stress100% online: Urus pelaburan kita pada bila-bila masa, di mana sahaja dengan hanya beberapa klik.Pelaburan Mampu Milik: Perlaburan minimum bermula dari RM100, dan kita boleh masukan ikut jadual yang kita nak maybe setiap 1, 2 atau 3 bulan dan kalau tak cukup modal boleh kumpul dulu hingga mencukupi RM100. Idea di sini adalah konsisten, bukan extreme tapi tak juga “tak buat apa-apa”. Nak buat auto-debit pun boleh.Yuran Pengurusan Rendah: Berbanding unit amanah lain yang mengenakan yuran pendahuluan tinggi, Versa Global-i mempunyai yuran pengurusan nominal tanpa caj jualan. Ini menjadikannya mampu dimiliki oleh orang biasa seperti kita:0% Caj Jualan: Tiada caj pendahuluan bermakna lebih banyak wang anda digunakan untuk menambah kekayaan.Tiada Yuran Broker: Melabur tanpa risau tentang kos tambahan (lihat gambar bawah). Kalau beli unit trust ni kat luar VERSA ada upfront sales fee, tapi kalau pakai VERSA sales fee is waived. **nota: ketika artikel ini di tulis harga se-unit adalah RM0.52 sen, boleh berubah dari masa ke semasa.

Kalau beli unit trust ni kat luar VERSA ada upfront sales fee, tapi kalau pakai VERSA sales fee is waived. **nota: ketika artikel ini di tulis harga se-unit adalah RM0.52 sen, boleh berubah dari masa ke semasa.Okay bab ni PENTING.

Saya juga ingin share bahawa pasaran saham akan turun & naik seperti terjadinya siang dan malam. Jadi kita jangan cepat panik bila graf tabung/dana kita jatuh seperti di bawah.

Graf ni tunjuk yang harga tabung ni jatuh pada awal tahun 2022, ini adalah kejatuhan yang melibatkan boleh kata semua stock di USA. Antaranya disebabkan peperangan Rusia-Ukraine dan sentimen market. Tapi pasaran akan pulih kembali selepas itu.

Graf ni tunjuk yang harga tabung ni jatuh pada awal tahun 2022, ini adalah kejatuhan yang melibatkan boleh kata semua stock di USA. Antaranya disebabkan peperangan Rusia-Ukraine dan sentimen market. Tapi pasaran akan pulih kembali selepas itu.Dan AHAM dah benchmark kan performance tabung ni kepada: Dow Jones Islamic Market World Index. Kalau anda perasan kenapa takda performance fund ni untuk 5 tahun. Sebab fund ni baru lagi di launch pada 12 OGOS 2021. So malang sikit nasib fund ni sebab baik2 jer launch terus kebetulan terjadinya isu Russia-Ukraine. TETAPI adalah suatu petanda yang baik, sebab fund ni naik balik dalam masa beberapa bulan. Kiranya lepas la ujian tu.

So ingat walaupun ia jatuh — ia bukanlah kerugian yang nyata — malah ia hanya dipanggil sebagai “unrealized loss”. Kita hanya akan betul2 rugi jika kita WITHDRAW duit kita semasa tabung ini jatuh. Teknik yang betul adalah “ride the fall” atau tunggang yang jatuh tu.

So ingat saya ulang –> let the investment

Kalau anda tertanya2 apa keuntungan yang saya perolehi dari Global-i ini setakat ni, saya share sikit sejak saya start awal bulan 4 hingga sekarang: saya masuk kan sikit2 hingga RM700, untung setakat ni adalah RM49.84. Ini juga kita namakan “Unrealized Profit” sebab profit ini bukan di dalam tangan saya, tapi dalam fund. Dan strategi saya bukan untuk withdraw RM49 ni, tapi biarkan nilainya berganda dan beranak pinak (compounded) dalam tu dengan setiap unit yang saya beli kelak untuk jangka masa lama.

Kalau anda tertanya2 apa keuntungan yang saya perolehi dari Global-i ini setakat ni, saya share sikit sejak saya start awal bulan 4 hingga sekarang: saya masuk kan sikit2 hingga RM700, untung setakat ni adalah RM49.84. Ini juga kita namakan “Unrealized Profit” sebab profit ini bukan di dalam tangan saya, tapi dalam fund. Dan strategi saya bukan untuk withdraw RM49 ni, tapi biarkan nilainya berganda dan beranak pinak (compounded) dalam tu dengan setiap unit yang saya beli kelak untuk jangka masa lama. Jadi saya dah join Versa Global-i! Anda bagaimana pula?

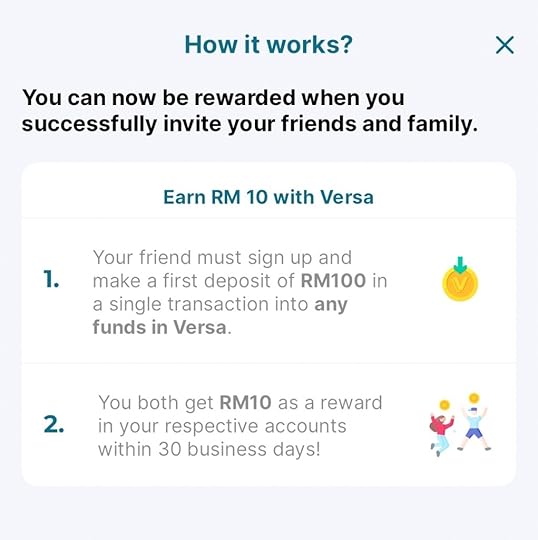

Sekiranya anda berminat nak sertai saya, sekarang ni ada promosi di mana VERSA hadiahkan kita berdua percuma RM10. Yup, hadiah percuma for you and me.

Anda cuma perlu:

Klik sini (atau jika anda lebih selesa untuk boleh juga download the app dari Apple Store atau Google Play – pastikan app yang legit)Jangan lupa masukkan nombor rujukan saya: 5XLT86D7Masukkan deposit pertama RM100 dalam mana2 tabung pilihan anda (tak semestinya Global-i)

Dan nanti bila anda dah ada akaun, anda pula boleh share dengan rakan2 anda seperti di bawah dan dapat RM10 every time rakan anda tekan link anda.

Okay guys, selamat melabur! Tapi sebelum melabur pastikan anda dah cover benda2 asas seperti keperluan asas & simpanan kecemasan seperti yang saya tulis dalam blog lepas.

PS: This is not a sponsored article. Although I am waiting for one. Ehem.

Dan seperti biasa setiap artikel berkenaan pelaburan mesti disertai dengan Disclaimer:

“Maklumat ini hanya untuk tujuan pendidikan dan tidak sepatutnya dianggap sebagai nasihat pelaburan kewangan profesional. Prestasi lepas tidak menunjukkan keputusan masa depan. Sila buat penyelidikan sebelum membuat keputusan pelaburan.”

June 9, 2024

Bagaimana nak plan belanje bulan2.

Dr Beni’s style.

Dear para pembaca,

Harap korang semuanya okay. Sebagai seorang rakyat Malaysia, saya nak share sikit plan kewangan perbelanjaan yang saya gunakan untuk capai matlamat jangka panjang. Cara ni saya panggil Plan 50/30/10/10. Saya modify sikit dari Ramit Sethi punya — Youtube’s financial guru “I will teach you to be rich.” Boleh cikidaut.

So plan ni senang je, kita bahagi pendapatan kepada beberapa kategori untuk pastikan kita belanja dan simpan dengan seimbang.

Pelan 50/30/10/10:50% – Perbelanjaan Wajib:

Guna 50% dari pendapatan untuk bayar semua benda yang wajib. Contohnya:

30% – Perbelanjaan Kehendak Gaya Hidup:

Guna 30% dari pendapatan untuk benda-benda yang kita suka tapi tak wajib. Contohnya:

10% – Simpanan Persaraan:

Simpan 10% dari pendapatan untuk persaraan dalam KWSP (EPF). But kalau anda ada majikan yang dah buatkan untuk anda. 10% ni boleh laburkan dalam ASB (Amanah Saham Bumiputera). Penting sangat jangan sentuh duit ni sampai kita bersara umur 55 – 60 tahun. Biarkan dia bertambah dengan faedah kompaun 5-6% setahun, nanti simpanan persaraan kamu akan bertambah banyak dengan kesan ajaib kompaun.

10% – Simpanan untuk Acara Besar:

Simpan 10% lagi untuk benda-benda besar macam:

Dengan ni, kita boleh urus acara besar tanpa stress kewangan. Dan yang paling penting anda tak “curi” dari wang ASB atau EPF persaraan anda. Ramai orang lupa bab ni.

Dana Kecemasan:

Dana Kecemasan:Okay sebelum kita invest dan simpan wang persaraan. Yang paling penting untuk kita ada tabung kecemasan yang boleh cover perbelanjaan bulanan selama 3-6 bulan. Ni penting kalau ada kejadian tak dijangka macam hilang kerja atau kecemasan perubatan. Boleh simpan dalam akaun simpanan dalam bank — tapi bank biasenya bagi interest sangat la ciput biasanya 0.25% setahun. Contoh: Kalau simpan RM1000 dalam Maybank dapat dividend RM2.50 setahun atau 20 sen sebulan (tengok gambar bawah).

Jadi… jika anda nak dividend lebih banyak, boleh try simpan dalam “money market fund” ada yang offer 3.5 hingga 4% setahun. Contoh macam Versa cash-i (sila lihat promo terkini). Yang latest sekarang ni adalah:

Kalau anda berminat nak buka VERSA akaun boleh guna link saya. Kita berdua akan dapat RM10.

Cara-cara nak buka Akaun Versa anda dengan Dr Beni:

Download Versa app: https://download.versa.com.my/1bAf/referral?deep_link_value=5XLT86D7Sign up isi kod saya 5XLT86D7Dan letak cash minimum RM100Buat masa ni VERSA ada buat ekstra promotion sampai hujung tahun 2024.

Fleksibiliti dan Penyesuaian:Ingat, plan ni fleksibel dan boleh diubah ikut keadaan kita. Kalau ada lebihan dari 50% perbelanjaan wajib atau 30% perbelanjaan kehendak, boleh kita masukkan yang ekstra tu ke dalam tabung simpanan ASB atau persaraan KWSP (especially bagi kawan2 kita yang kerja gig ekonomi macam Grab Rider dan pelakon atau penyanyi negarawan seperti Dato’ Siti Nurhaliza yang tiada majikan untuk carumkan KWSP –> mereka kena buat sendiri). Lagi banyak kita simpan dan labur dengan bijak, lagi terjamin masa depan kewangan kita.

Tapi Ingat! Fleksibel ni TIDAK BERMAKSUD kita ambik wang dari tabung simpanan & persaraan untuk beli handphone baru.

Dengan ikut peraturan 50/30/10/10, kita boleh belanja dan simpan dengan seimbang, pastikan keperluan semasa dipenuhi sambil bersiap untuk masa depan. Disiplin kewangan dan perancangan bijak hari ini akan bantu capai kehidupan yang stabil dan puas hati esok.

Kalau ada soalan atau nak nasihat lanjut, jangan segan-segan tanya saya. Saya sentiasa ada untuk bantu.

Salam hormat,

Dr Beni

Tip2 di sini adalah atas dasar kongsi info dan bukan bersifat nasihat dari Pakar Kewangan yang berdaftar. Sila Rujuk Pakar kewangan untuk perkhidmatan profesional.

April 11, 2024

Kesilapan definisi dalam polisi insurans

Mula2 saya cuba tulis dalam BM tetapi disebabkan terlalu banyak terminology perubatan. Ia lebih sesuai di tulis dalam BI. Let me know in the comments if you prefer me to write in BM or BI in future articles.

I also hope this article doesn’t land me in trouble. Disclaimer: This article solely represents my personal opinion and does not reflect the views of my employer.

In the complex world of healthcare, accuracy is not just important, it’s vital. But what happens when a misclassification triggers a wave of misunderstanding? During my deep dive into health insurance policies (I sometimes do this to get familiarize with policies to assist my patients with their claims), I discovered an inaccuracy inside a critical illness policy from a leading Malaysian insurance company.

I provide the link here (which remains uncorrected as of 11 April 2024) that will lead you to “Big 3 Critical Illness Protection Plan.”

Then click on: 24 conditions (at the bottom of the screenshot) which would bring you to another page.

Look at row #6: Enhanced External Counterpulsation. The description is inaccurate and is more suited to another procedure called IABP.

Look at row #6: Enhanced External Counterpulsation. The description is inaccurate and is more suited to another procedure called IABP.Understanding EECP Therapy

EECP, or Enhanced External Counterpulsation, is an FDA-approved therapy for long-term stable chest pain, may sound complex, but its core concept is simple. It’s a non-invasive treatment typically administered in outpatient clinics, and sometimes even in shop lots. During EECP treatment, cuffs are applied to your legs to apply pressure to blood vessels, thereby enhancing blood circulation to your heart. Patients usually undergo this therapy for a total of 35 hours: one hour per day, five days a week, for seven weeks.

EECP: cuff applied to legs. Nothing is placed inside the body. She looks stable and not seriously ill.

EECP: cuff applied to legs. Nothing is placed inside the body. She looks stable and not seriously ill. This therapy is recommended for a specific group of patients suffering from long-term (chronic) chest pain that could limit their activities. It’s often considered when other interventions, like angioplasty or coronary artery bypass graft, have been performed or aren’t feasible; or when symptoms persist despite optimal medication and/or without other therapeutic options.

However, it’s crucial to note that there is no data indicating EECP prolongs survival. Therefore, if you don’t experience any chest pain, there’s no justification for undergoing EECP.

The scientific mechanism suggests it may stimulate the development of small blood vessels supplying the heart. The American College of Cardiology currently labels it as Class IIb, backed by moderate-quality evidence (Level of evidence B) supporting its usefulness.

(Class IIb: indicates that the usefulness or efficacy of a procedure or treatment is less well established by evidence).

From: 2023 AHA/ACC Guideline for the management Chronic coronary disease.

From: 2023 AHA/ACC Guideline for the management Chronic coronary disease. Regrettably, there are centres in Malaysia that unethically offer EECP as a first-line therapy to clients who do not need it. And most of these clients have not undergone proper assessment and treatment by cardiologists. These centres often charge exorbitant price.

And how about IABP?

IABP, or Intra-Aortic Balloon Pump, is a medical device considered as an invasive procedure performed inside hospitals by cardiologists for unstable patients experiencing shock from a heart attack or in preparation for coronary artery bypass graft surgery.

A cardiologist performing IABP in a hospital setting. The patient does not look well. Look at the face.

A cardiologist performing IABP in a hospital setting. The patient does not look well. Look at the face.The procedure involves inserting a slender tube called a catheter into the aorta, the main artery leaving the heart, with a balloon at its tip. This balloon inflates and deflates in coordination with the heart’s rhythm, aiming to provide mechanical support and improve blood flow to the heart, thereby reducing the heart’s workload. It’s a lifesaving intervention for patients in critical condition, such as those experiencing cardiac shock.

The Confusion

The dilemma arises as it’s uncertain which therapy the insurance company intends to cover, whether EECP or IABP. To navigate this confusion, it’s advisable to reach out to the insurance company directly or consult with your insurance agent for clarification. So far, I have not been able to reach the company for clarification. I called them before the fasting month, but their agents have not returned my call. This article is not intended to cast a negative light on this company. I am sure it is an honest oversight which might be explained further in their full policy. And I am sure they have their own medical panel that double-checks their policies. I hope they would come across this article and amend that part.

Your homework

If you come across the term EECP or IABP in your policy with your own company, please check if a similar error takes place. You could even check with your agent for clarification; they are there to help you. The dedicated ones will definitely help you to answer any uncertainty in your policy.

Conclusion: The Way Forward

In the intricate landscape of healthcare, effective communication and accuracy are pivotal. It’s imperative for insurance companies and their agents, healthcare providers, and patients to have a clear understanding of the treatments and procedures and which illness covered by their policies.

Terima kasih. I hope this helps. I welcome your feedback and any suggestion.

March 16, 2024

“Sikit2. Lama2 jadi bukit.” – Warren Buffet.

As of Q4 2022Let me confess one thing upfront: I initially had some apprehensions about writing this article because it’s about money and finance, and I’m not a financial advisor. But curiosity drives me to learn more about the world we live in.

As of Q4 2022Let me confess one thing upfront: I initially had some apprehensions about writing this article because it’s about money and finance, and I’m not a financial advisor. But curiosity drives me to learn more about the world we live in.I’m not an investor. My resume is I invest in ASB. I can’t even read a stock chart—but I can tell you about one guy who can, and you already know his name: Warren Buffett. Although he insists I call him “Warry.” Okay, kidding.

Mr. Buffett is an investment wizard with the talent to predict which stocks to pick. As a result of 80 years of hard work, he’s now worth more than USD100 billion (1 billion = 1000 million). Because of this, people give him the nickname “the Oracle of Omaha,” a place where he lived. He’s also 93 this year, but interestingly, 99% of his wealth came after his 50th birthday. That’s the magic of compound interest, a topic for another day.

While Buffett’s success may seem elusive to some, BUT he himself has famously recommended index funds / ETF for the average investor like you and me, even going so far as to instruct the trustee of his estate to invest 90% of his wealth into a low-cost S&P 500 index fund upon his passing.

And what is S&P 500, you might ask? The S&P 500 is a stock market index that measures the stock performance of 500 large companies (Apple, Microsoft, Google, Facebook, Tesla, etc.) listed on stock exchanges in the United States. It is considered one of the best representations of the U.S. stock market. The US equity market has been one of the best performing markets in the world over the long term. The benchmark S&P 500 has grown steadily through various crises and events from 1970 through 2022.

Not exactly S&P 500. This index looks at 3000 companies around the world in developed & emerging markets. Despite many crises, the trend goes up in the end.

Not exactly S&P 500. This index looks at 3000 companies around the world in developed & emerging markets. Despite many crises, the trend goes up in the end.While we can’t directly invest in an index, we can invest in index funds or ETFs (exchange-traded funds) that track them. There are subtle differences between an index fund and ETF; however, they share more similarities. For simplicity, I will stick to ETF.

And here are some ETF that track S&P 500 index:

SPDR S&P 500 ETF (SPY)iShares Core S&P 500 ETF (IVV)Vanguard S&P 500 ETF (VOO) Example of an ETF named VOO and the Top 10 companies on its list- as of 31 Dec 2023. This list looks almost identical to any ETF that track S&P 500.

Example of an ETF named VOO and the Top 10 companies on its list- as of 31 Dec 2023. This list looks almost identical to any ETF that track S&P 500.Pro tip: The letter inside the bracket e.g. VOO is called Ticker/symbol. Go on and type that on your web browser, and you will get to see the fund performance in real time online. But don’t worry about it because remember our target is long-term.

So, these ETFs use an algorithm that seeks to replicate the performance of a specific market index, like in this case the S&P 500 — which offer investors a simple and low-cost way to gain broad exposure to the overall market. On the other hand, traditional private unit trust (example Public Mutual) would rely on fund managers who use your money to pick a portfolio of investments (stocks, bonds, REITs) to beat the market, which explains why their upfront fees and sales charges are expensive.

I do not intend to watch the financial market. It’s just too much work, and I have a day job to do. But I also don’t want to leave my investment money in the hands of a fund manager. Suffice to say I had a bad experience with private unit trust in the past.

So these days I would just invest in ETF. The market will definitely go up and down in the short term, but over the long run, it will correct itself and will go up. All I need to do is just consistently make a deposit into the ETF each month and then sit back and watch it grow.

Now, you might be wondering, why the US market? Why not invest in ASB? Well, you should invest in ASB — it is time tested and safe.

But on the other hand, U.S market is where the moolah sits and it’s your chance to sit at the main table with big companies like Apple & Microsoft, instead of local companies like Maybank and Sime Darby (which you already have invested in if you have ASB account).

But what is Wahed?

Now here comes the dilemma. For Muslim investors who want to invest in ETFs that track a popular overseas index like the S&P 500— you might get exposed to non-Shariah stocks.

To overcome this, there is a Shariah-compliant ETF called HLAL (pronounced halal). Nama surat beranak on NASDAQ is Wahed FTSE US Shariah ETF.

Did you know? Alphabet is the parent company of Google. Like Meta for Facebook.

Did you know? Alphabet is the parent company of Google. Like Meta for Facebook.HLAL is developed by Wahed invest, a digital halal investment platform based in New York since 2015 and has now expanded to various regions including the UK, Malaysia and UAE with more than 300,000 customers. It is also known as a robo-advisory that uses algorithms to automate your investment portfolio. It has successfully obtained a regulatory license from the Securities Commission (SC) Malaysia.

Now HLAL doesn’t track S&P 500 per se, instead it uses FTSE USA Shariah Index as its benchmark, and not surprisingly it also contains the hot stocks in the S&P 500 with > 40% shares are in the big companies listed above. The whole deal is to provide everyday investors like you and me with an opportunity to gain exposure to the Halal US market stocks and even Halal global market through their UMMA fund.

Wahed HLAL: aggressive portfolio. Kalau lah aku menabung 3 tahun lepas, dah dapat 4,936 extras.

Wahed HLAL: aggressive portfolio. Kalau lah aku menabung 3 tahun lepas, dah dapat 4,936 extras.Comparing this to the returns from our ASB, which typically hover around 5%, the potential for profit with Wahed seems better with an average performance of around 11% (for a very aggressive portfolio; depending on your risk appetite—you can choose this to be moderate or conservative).

But please remember that investments give you the best return in the long term, say 5 to 10 years (even longer). While short-term investing can be tricky, one thing remains constant: over the past 100 years, the market has shown consistent growth.

Wahed Pricing

In their website, Wahed Invest stated that they charge a single fee, called the “Wrap Fee”, for all management, custodian, and transaction fees. The fee structure is as follows:

RM100–RM499,999: 0.79% (ppst… I think of us are going to be in this category)

RM500,000 and over: 0.39%

This is per year amount but charged monthly.

For example, if you have RM5,000 in your account, their fee is 0.79% x 5,000 = RM39.50 per year or RM3.29 per month.

How about ASB?

Unlike HLAL which has variable price (similar to Amanah Saham Nasional), ASB is a unit trust fund with a fixed price of RM1 per unit. According to ASB 2020 Annual Report, the largest sector that ASNB heavily invests in are the Monetary Sector (27%) – perhaps because it is an income type-fund and need stability to ensure distribution to Malaysian. Look at the table. It’s quite ironic to imagine that whenever Malaysians default on their Maybank credit card debt payment might potentially lead to higher ASB dividends. I dunno.

ASB invests our money in these companies. List is non-exhaustive. Pump minyak kat Petronas yok.

ASB invests our money in these companies. List is non-exhaustive. Pump minyak kat Petronas yok.In contrast to popular belief, ASB is not a capital guaranteed or capital protected fund. Since ASB is an investment product, not a deposit, so it is also not covered by PIDM (Perbadanan Insurans Deposit Malaysia) like our money in bank accounts (up to RM250K).

ASB is also not FOC. There is management fee and trustee fee as shown below, it’s just that as far as I know “mereka dah tolak siap2” before declaring the dividend distribution.

ASB fund fact sheet: What?! 1 million?

ASB fund fact sheet: What?! 1 million?ASB vs Wahed

First of all, we cannot compare them as they belong to different types of investment (income vs passive equity) with different objectives and portfolios. It’s like comparing apples to oranges – but nevertheless, they are still fruit. Just for illustration, let’s have a look at these two charts. Let’s be conservative and give Wahed an 8% return and ASB with its 5% average. And let’s put RM100 per month into each fund and track them for 10 years.

ASB – RM100 monthly with 5% dividend annually for 10 years

ASB – RM100 monthly with 5% dividend annually for 10 years

RM100 monthly into any fund that has 8% dividend annually for 10 years.

RM100 monthly into any fund that has 8% dividend annually for 10 years.(Not a real HLAL fund, just as an example for any fund that has 8% average return).

That’s RM2,682.12 difference after 10 years.

So, would I put all of my investment into Wahed and forget about ASB? Definitely not. Because ASB is indirectly owned by Malaysian government and is relatively safer for obvious reasons.

So, what would I do if I have RM300? I will put RM200 in ASB and RM100 in Wahed at least I know I have some exposure to the U.S. market.

Investment strategies

There are 2 ways to deposit your hard-earned money. First is lump sum works fine for ASB as the price is fixed at RM1. Second is dollar-cost averaging by placing a deposit every month consistently without fail, no matter whether the market is up or down throughout the year. Research have shown that the DCA is better than lumpsum for variable pricing stock like ETFs because it’s able to take advantage of the average stock’s price given in a long run.

How to open your account

Interested to join? Well first, I suggest you visit their website here and get yourself familiarized with the original source. Do your homework and due diligence.

You can’t open account on their website.

You can’t open account on their website.Once you’re satisfied, to open an account, you have to download the app on your smartphone. Either from Apple App Store or Google Play Store. Make sure you download a genuine app and not from another 3rd party that can scam you.

The registration is quite easy and straightforward. Just follow the instruction in the app. You need to answer a few questions in which they will ask you about your risk-tolerance and will decide which portfolio is suitable for you, i.e. aggressive, moderate or conservative. The rest is confirming your identification such as scanning your IC and taking a selfie (the usual KYC). Once your account is up you can start depositing your money via your savings account.

Make sure you download genuine app.

Make sure you download genuine app.On the app:

Select one time option (bank charges RM1 for recurring deposit)Select your bank.They will give you the bank account & payment reference.Log into your bank and do the usual transfer method by filling in Wahed bank account number and don’t forget payment reference.And wait for 2-3 working days before you see your deposit in your Wahed account. Minimum deposit is RM50.

Minimum deposit is RM50.BONUS

Here is the fun part, Wahed is doing a promotion through referral system. You can get a free RM10 ringgit to jumpstart your investment by inserting my referral code: benrus1.

Can’t believe I’m doing this. Maybe can fund a new stethoscope. Old one is missing.

Can’t believe I’m doing this. Maybe can fund a new stethoscope. Old one is missing.With the conditions:

** Sejak bulan April 2024 Wahed dah ubah syarat referral now — latest as of 16 April 2024, ianya adalah:

Ajak 2 org kawan anda join Wahed dan mereka deposit RM300 / seorang dalam akaun baru mereka dgn menggunakan kod rujukan anda. Maka anda dapat RM40 & rakan anda dapat RM10.

So, fellow readers, if you’ve been contemplating to go beyond ASB and local markets, I recommend giving Wahed Invest a shot.

The only thing that will give us money during our retirement is how much we invest today.

Sementara tunggu boke pose. Check market kejap. Not bad.

Sementara tunggu boke pose. Check market kejap. Not bad.

Disclaimer: The information provided in this article is for educational purposes only and is not intended as financial or investment advice. Past performance of the market does not guarantee future returns. Every investment comes with risk, and investors may lose some or all of their investment. Readers should seek advice from a licensed professional before making any investment decisions. Always do your own research and consider your financial condition and investment goals before investing.

“Sikit2. Lama2 jadi bukit.” – Warren Buffet. Previously entitled ASB, Apple stocks and benrus1.

As of Q4 2022Let me confess one thing upfront: I initially had some apprehensions about writing this article because it’s about money and finance, and I’m not a financial advisor. But curiosity drives me to learn more about the world we live in.

As of Q4 2022Let me confess one thing upfront: I initially had some apprehensions about writing this article because it’s about money and finance, and I’m not a financial advisor. But curiosity drives me to learn more about the world we live in.I’m not an investor. My resume is I invest in ASB. I can’t even read a stock chart—but I can tell you about one guy who can, and you already know his name: Warren Buffett. Although he insists I call him “Warry.” Okay, kidding.

Mr. Buffett is an investment wizard with the talent to predict which stocks to pick. As a result of 80 years of hard work, he’s now worth more than USD100 billion (1 billion = 1000 million). Because of this, people give him the nickname “the Oracle of Omaha,” a place where he lived. He’s also 93 this year, but interestingly, 99% of his wealth came after his 50th birthday. That’s the magic of compound interest, a topic for another day.

While Buffett’s success may seem elusive to some, BUT he himself has famously recommended index funds / ETF for the average investor like you and me, even going so far as to instruct the trustee of his estate to invest 90% of his wealth into a low-cost S&P 500 index fund upon his passing.

And what is S&P 500, you might ask? The S&P 500 is a stock market index that measures the stock performance of 500 large companies (Apple, Microsoft, Google, Facebook, Tesla, etc.) listed on stock exchanges in the United States. It is considered one of the best representations of the U.S. stock market. The US equity market has been one of the best performing markets in the world over the long term. The benchmark S&P 500 has grown steadily through various crises and events from 1970 through 2022.

Not exactly S&P 500. This index looks at 3000 companies around the world in developed & emerging markets. Despite many crises, the trend goes up in the end.

Not exactly S&P 500. This index looks at 3000 companies around the world in developed & emerging markets. Despite many crises, the trend goes up in the end.While we can’t directly invest in an index, we can invest in index funds or ETFs (exchange-traded funds) that track them. There are subtle differences between an index fund and ETF; however, they share more similarities. For simplicity, I will stick to ETF.

And here are some ETF that track S&P 500 index:

SPDR S&P 500 ETF (SPY)iShares Core S&P 500 ETF (IVV)Vanguard S&P 500 ETF (VOO) Example of an ETF named VOO and the Top 10 companies on its list- as of 31 Dec 2023. This list looks almost identical to any ETF that track S&P 500.

Example of an ETF named VOO and the Top 10 companies on its list- as of 31 Dec 2023. This list looks almost identical to any ETF that track S&P 500.Pro tip: The letter inside the bracket e.g. VOO is called Ticker/symbol. Go on and type that on your web browser, and you will get to see the fund performance in real time online. But don’t worry about it because remember our target is long-term.

So, these ETFs use an algorithm that seeks to replicate the performance of a specific market index, like in this case the S&P 500 — which offer investors a simple and low-cost way to gain broad exposure to the overall market. On the other hand, traditional private unit trust (example Public Mutual) would rely on fund managers who use your money to pick a portfolio of investments (stocks, bonds, REITs) to beat the market, which explains why their upfront fees and sales charges are expensive.

I do not intend to watch the financial market. It’s just too much work, and I have a day job to do. But I also don’t want to leave my investment money in the hands of a fund manager. Suffice to say I had a bad experience with private unit trust in the past.

So these days I would just invest in ETF. The market will definitely go up and down in the short term, but over the long run, it will correct itself and will go up. All I need to do is just consistently make a deposit into the ETF each month and then sit back and watch it grow.

Now, you might be wondering, why the US market? Why not invest in ASB? Well, you should invest in ASB — it is time tested and safe.

But on the other hand, U.S market is where the moolah sits and it’s your chance to sit at the main table with big companies like Apple & Microsoft, instead of local companies like Maybank and Sime Darby (which you already have invested in if you have ASB account).

But what is Wahed?

Now here comes the dilemma. For Muslim investors who want to invest in ETFs that track a popular overseas index like the S&P 500— you might get exposed to non-Shariah stocks.

To overcome this, there is a Shariah-compliant ETF called HLAL (pronounced halal). Nama surat beranak on NASDAQ is Wahed FTSE US Shariah ETF.

Did you know? Alphabet is the parent company of Google. Like Meta for Facebook.

Did you know? Alphabet is the parent company of Google. Like Meta for Facebook.HLAL is developed by Wahed invest, a digital halal investment platform based in New York since 2015 and has now expanded to various regions including the UK, Malaysia and UAE with more than 300,000 customers. It is also known as a robo-advisory that uses algorithms to automate your investment portfolio. It has successfully obtained a regulatory license from the Securities Commission (SC) Malaysia.

Now HLAL doesn’t track S&P 500 per se, instead it uses FTSE USA Shariah Index as its benchmark, and not surprisingly it also contains the hot stocks in the S&P 500 with > 40% shares are in the big companies listed above. The whole deal is to provide everyday investors like you and me with an opportunity to gain exposure to the Halal US market stocks and even Halal global market through their UMMA fund.

Wahed HLAL: aggressive portfolio. Kalau lah aku menabung 3 tahun lepas, dah dapat 4,936 extras.

Wahed HLAL: aggressive portfolio. Kalau lah aku menabung 3 tahun lepas, dah dapat 4,936 extras.Comparing this to the returns from our ASB, which typically hover around 5%, the potential for profit with Wahed seems better with an average performance of around 11% (for a very aggressive portfolio; depending on your risk appetite—you can choose this to be moderate or conservative).

But please remember that investments give you the best return in the long term, say 5 to 10 years (even longer). While short-term investing can be tricky, one thing remains constant: over the past 100 years, the market has shown consistent growth.

Wahed Pricing

In their website, Wahed Invest stated that they charge a single fee, called the “Wrap Fee”, for all management, custodian, and transaction fees. The fee structure is as follows:

RM100–RM499,999: 0.79% (ppst… I think of us are going to be in this category)

RM500,000 and over: 0.39%

This is per year amount but charged monthly.

For example, if you have RM5,000 in your account, their fee is 0.79% x 5,000 = RM39.50 per year or RM3.29 per month.

How about ASB?

Unlike HLAL which has variable price (similar to Amanah Saham Nasional), ASB is a unit trust fund with a fixed price of RM1 per unit. According to ASB 2020 Annual Report, the largest sector that ASNB heavily invests in are the Monetary Sector (27%) – perhaps because it is an income type-fund and need stability to ensure distribution to Malaysian. Look at the table. It’s quite ironic to imagine that whenever Malaysians default on their Maybank credit card debt payment might potentially lead to higher ASB dividends. I dunno.

ASB invests our money in these companies. List is non-exhaustive. Pump minyak kat Petronas yok.

ASB invests our money in these companies. List is non-exhaustive. Pump minyak kat Petronas yok.In contrast to popular belief, ASB is not a capital guaranteed or capital protected fund. Since ASB is an investment product, not a deposit, so it is also not covered by PIDM (Perbadanan Insurans Deposit Malaysia) like our money in bank accounts (up to RM250K).

ASB is also not FOC. There is management fee and trustee fee as shown below, it’s just that as far as I know “mereka dah tolak siap2” before declaring the dividend distribution.

ASB fund fact sheet: What?! 1 million?

ASB fund fact sheet: What?! 1 million?ASB vs Wahed

First of all, we cannot compare them as they belong to different types of investment (income vs passive equity) with different objectives and portfolios. It’s like comparing apples to oranges – but nevertheless, they are still fruit. Just for illustration, let’s have a look at these two charts. Let’s be conservative and give Wahed an 8% return and ASB with its 5% average. And let’s put RM100 per month into each fund and track them for 10 years.

ASB – RM100 monthly with 5% dividend annually for 10 years

ASB – RM100 monthly with 5% dividend annually for 10 years

RM100 monthly into any fund that has 8% dividend annually for 10 years.

RM100 monthly into any fund that has 8% dividend annually for 10 years.(Not a real HLAL fund, just as an example for any fund that has 8% average return).

That’s RM2,682.12 difference after 10 years.

So, would I put all of my investment into Wahed and forget about ASB? Definitely not. Because ASB is indirectly owned by Malaysian government and is relatively safer for obvious reasons.

So, what would I do if I have RM300? I will put RM200 in ASB and RM100 in Wahed at least I know I have some exposure to the U.S. market.

Investment strategies

There are 2 ways to deposit your hard-earned money. First is lump sum works fine for ASB as the price is fixed at RM1. Second is dollar-cost averaging by placing a deposit every month consistently without fail, no matter whether the market is up or down throughout the year. Research have shown that the DCA is better than lumpsum for variable pricing stock like ETFs because it’s able to take advantage of the average stock’s price given in a long run.

How to open your account

Interested to join? Well first, I suggest you visit their website here and get yourself familiarized with the original source. Do your homework and due diligence.

You can’t open account on their website.

You can’t open account on their website.Once you’re satisfied, to open an account, you have to download the app on your smartphone. Either from Apple App Store or Google Play Store. Make sure you download a genuine app and not from another 3rd party that can scam you.

The registration is quite easy and straightforward. Just follow the instruction in the app. You need to answer a few questions in which they will ask you about your risk-tolerance and will decide which portfolio is suitable for you, i.e. aggressive, moderate or conservative. The rest is confirming your identification such as scanning your IC and taking a selfie (the usual KYC). Once your account is up you can start depositing your money via your savings account.

Make sure you download genuine app.

Make sure you download genuine app.On the app:

Select one time option (bank charges RM1 for recurring deposit)Select your bank.They will give you the bank account & payment reference.Log into your bank and do the usual transfer method by filling in Wahed bank account number and don’t forget payment reference.And wait for 2-3 working days before you see your deposit in your Wahed account. Minimum deposit is RM50.

Minimum deposit is RM50.BONUS

Here is the fun part, Wahed is doing a promotion through referral system. You can get a free RM10 ringgit to jumpstart your investment by inserting my referral code: benrus1.

Can’t believe I’m doing this. Maybe can fund a new stethoscope. Old one is missing.

Can’t believe I’m doing this. Maybe can fund a new stethoscope. Old one is missing.With the conditions:

Deposit at least RM100.Keep it there for at least 30 days.Once you have successfully deposited your money, you will also be given your unique referral code in which you can invite your friends an extend the RM10 as a free gift to them as well. And you will also get RM10 / RM20.So, fellow readers, if you’ve been contemplating to go beyond ASB and local markets, I recommend giving Wahed Invest a shot.

The only thing that will give us money during our retirement is how much we invest today.

Sementara tunggu boke pose. Check market kejap. Not bad.

Sementara tunggu boke pose. Check market kejap. Not bad.

Disclaimer: The information provided in this article is for educational purposes only and is not intended as financial or investment advice. Past performance of the market does not guarantee future returns. Every investment comes with risk, and investors may lose some or all of their investment. Readers should seek advice from a licensed professional before making any investment decisions. Always do your own research and consider your financial condition and investment goals before investing.

February 23, 2024

Eh claim critical illness ‘Serangan jantung’ tak lepas.

“Eh doktor cakap saya kena serangan jantung, tapi tuntutan Penyakit Kritikal (Critical illness, CI) saya tak lepas. Apa ni wei. Bayar mahal.”

Ada antara anda yg mungkin keliru kenapa ini berlaku, tapi jawapannya ada dalam definisi serangan jantung polisi CI anda. Anda kena berhati-hati dan check polisi anda.

Kerana untuk penuhi syarat serangan jantung (myocardial infarct), anda perlu penuhi ketiga-tiga kriteria:

Sakit dadaPerubahan ECGUjian darah jantung3 jenis serangan jantung popular:

STEMINon-STEMIUnstable anginaNo 1 & 2 biasanya penuhi ke tiga2 syarat. Tapi no 3. Unstable angina adalah sejenis serangan jantung di mana dua kriteria pertama dipenuhi, tetapi kriteria ketiga masih normal dan ia TIDAK termasuk dalam senarai penyakit kritikal.

Jom tengok contoh definasi serangan jantung dalam polisi CI yang ada kat Malaysia yg saya screen shot dari Internet — (disclaimer: mungkin polisi anda berbeza).

So jom tgk balik apa 3 kriteria tu.

Sakit dada: Atau yang sewaktu dgn nya. Sebab kadang2 sakit tu mungkin tak tepat atas dada. Mungkin ia atas sikit kawasan perut perut atau kawasan leher.

Saya ‘sakit hati’, tapi jantung saya okay.

2. ECG: kena nampak luar biasa atau ada perubahan yang menunjukkan serangan jantung.

Tips: Perkataan ST dalam STEMI & non-STEMI – merujuk pada perubahan ECG.

3. Ujian darah: Tahap enzim darah jantung yang tinggi, biasanya dipanggil CKMB dan troponin. Yang ni banyak yang tak lepas. Sebab nilainya perlu tinggi untuk POSITIVE (abnormal) menunjuk kan ada otot jantung yang cedera. Maksudnya serangan tu major.

Jadi, ingatlah, semua tiga kotak semak perlu ditanda untuk tuntutan yang berjaya.Pokok pangkal fahami polisi anda. Benda ni bukan beli selalu.

“Maka Sebelum beli polisi tanya agen anda.“

Yang ikhlas,

Dr Beni