Jeff Carter's Blog: Retirement Income Planning

March 30, 2016

Tim Knox Interviews Jeff Carter Best Selling Author about his book Retirement Boom™

The Roadmap for Turning Your Retirement Savings into Guaranteed Lifetime Income. The book helps you prepare for the longest vacation of your life, Retirement.

Interviewing Authors Interview Transcript of Jeff Carter – Retirement Boom

Tim Knox: Hi everyone and welcome into a special book spotlight edition of Interviewing Authors. Jeff Carter is my guest today. Jeff is an entrepreneur, financial expert, financial planner, and the author of one of my favorite new books Retirement Boom, Turning Your Retirement Savings Into Guaranteed Lifetime Income, which gives financial strategies and advice to baby boomers who are quickly approaching retirement age, many of us, without a retirement plan or income.

The reason this is one of my new favorite books is I am Jeff’s target audience. I’m a baby boomer and admittedly I can use all the sound advice I can get, especially now that I’m quickly approaching what traditionally has been called the “retirement years”. But people are now living longer, which means will be the need to have income well into your elderly years and sadly, many of us are not as prepared as we should be.

Jeff calls on his 25 years of experience as a financial planner for this book and offers up a number of strategies and ideas that every boom can benefit from, myself included.

Here then is my interview with entrepreneur, financial expert, and author, Jeff Carter, on his book Retirement Boom, Turning Your Retirement Savings Into Guaranteed Lifetime Income, on this book spotlight edition of Interviewing Authors.

Tim Knox: Jeff, welcome to the program.

Jeff Carter: Thank you Tim. It’s my pleasure to participate.

Tim Knox: Well, I’m very excited to have you here. You’ve got a new book that is the Retirement Boom and it is written specifically I think for baby boomers, of which I am one. So I’m going to learn a lot on this interview as well our audience. But before we get started, if you will, give us a little background on you.

Jeff Carter: Well, thank you Tim. I was actually born in Charleston, Illinois. My parents were going to Eastern Illinois University at the time and then after my father graduated college, he moved up to the Chicago land area and that’s where I was raised in – after my schooling, I moved West of the Mississippi to pursue opportunities that existed. That took me to Denver where I was involved with a childhood friend who actually started a cable television construction company. So I was involved in the early stages of the cable television industry and ultimately grew that into a company with 120 employees with offices across United States.

At the time, I was in LA. It was roughly when I was about 29 years of age, 30 years of age. I had an administrative assistant who had a financial services professional call on me and wanted to meet with me. So I scheduled an appointment. His timing was impeccable in that I had recently had a young baby and I needed to do some planning, buy some life insurance, do some estate planning to get my affairs in order so that in the event of a premature death, I wouldn’t leave my wife and child in the lurch.

So that’s what brought me into the financial services arena. After working with this gentleman, he was able to enlighten me about the importance of planning and one thing led to another and shortly thereafter, I sold my cable television business and entered the financial services profession and that’s where I’ve been now for the past 25 years.

Tim Knox: So you’re an old entrepreneur who was in the cable industry early. I remember having only three channels. Do you remember those days?

Jeff Carter: I do. I do. I remember Tim the remote control was the person that got off the couch and turned the channel.

Tim Knox: Exactly right. I remember that. The next generation remote control actually had a wire. Remember that? That ran from the control – if I told that to my kids now, they would look at me like I was talking science fiction.

So you were an entrepreneur and you kind of got into the financial services profession when someone called on you. Now, what really appealed to you? What attracted you to financial services?

Jeff Carter: The opportunity to help people. When I was in the construction industry, I just didn’t feel like I was touching people’s lives and helping them in a meaningful way. I saw the financial services industry as an opportunity to do that because I saw how this gentleman working with me doing my personal planning really changed my life. So that is really what was the catalyst that motivated me to pursue this career.

Tim Knox: Now have you ever been surprised by the number of people that know very little about financial planning and planning for retirement? Does it ever amaze you how little thought some people give to that, looking after their own money?

Jeff Carter: Well, it does and it doesn’t Tim. Actually, to be very candid, I think I was in that place at one time where it was just go to work and earn a check and pay the bills and move forward day by day like that, not really worrying about the long range planning. I think that at least for me, as I was younger, I was invincible. I thought I would live forever. Didn’t think – I thought retirement was so far out into the future that it just didn’t make any sense to worry about it.

As you and I both know, being baby boomers ourselves and personally I’m 55 years of age, it sneaks up on you very quickly. So yes, I have – through my years of working with individuals the past 25 years, I’ve seen just about every different aspect of – perspectives people take as it pertains to their money and planning.

I think it really goes back to the early years when we were in grade school, K through 12. Those skills or classes really weren’t something that were taught. So it was pretty much left up to – through osmosis. You pick it up through your parents or you observe how they behave and what they do in the home that you grow up in. You embrace whatever that environment was. That’s kind of how you carry it forward in your life.

It tends to perpetuate itself from one generation to the next and obviously that has a lot to do with it.

Tim Knox: I think that’s a very good point. The kids really do learn a lot from their parents, even how to manage money or how to mismanage money. So – I think the world has changed considerably. Now, you’ve been doing this for 25 years. Years ago, the retirement goal was find a good job, keep it until you’re 65, retire and go off into the sunset. But now people are living longer. They’ve got to have that money longer and so I think it has probably changed the way that you do your job as a financial planner.

Now let’s talk a little bit about your new book, the Retirement Boom. What motivated you to write this book?

Jeff Carter: Well, after all of these years of working with thousands of clients, I’ve been blessed to be embraced and allowed to participate in their lives. Through that process, I have learned a lot from both successful people and people that have made mistakes. What I have found is that all too often, very few people really understand the intricacies of what it means to actually plan for their retirement income.

There’s a process one goes through and it’s comprehensive. But if you have the roadmap to do that, it’s like anything else. You start at point A and you end up at point Z and there are just things that are done along the path to ultimately get to where you need to be with the plan that you need.

So what I decided was I – after doing this for so many years and meeting with so many people, there’s only so many hours in a day. So I can only impact or touch a finite amount of people in life and have any significant impact.

So I thought that writing this book would give me an opportunity to share my 25 years of knowledge with millions of people that would allow them to basically buy a master’s course in the form of a book that will walk them through the process.

So if they decide to do it themselves, all the answers are there for them to do that. If they decide to engage another professional in the financial services arena, they’re able to do that because it spells out exactly how to go about looking for those individuals and interviewing them and making decisions on who they want to work with.

So I would give them all of the tools they need in the toolbox to accomplish this goal or this task and ultimately the goal that they have, that they identify through the process.

So to answer your question specifically, I wanted to touch more lives than I was able to touch on one-to-one interviews.

Tim Knox: Right. Do you believe – and your experience I guess will back this up, the old saw, that people probably give more attention to planning a vacation than planning a retirement.

Jeff Carter: No question about it. If you stop and think of it, it’s an analogy that’s used quite a bit and – but it’s so true. If you think about it – us baby boomers as an example and I will use myself as an example. My wife and I have been blessed and so we’re able to take off usually six weeks in the summer to travel.

When we do that, it’s an elaborate process we go through to plan where we’re going to be staying, the time it takes to drive between one location and the next, how long we will be staying at each location, what sort of activities we will be involved in at those locations. Where will we eat and so on?

So we put every year probably close to 80 hours in the planning of a six-week vacation each year. That’s just the vacation. That’s not a 20-year retirement. So you can see how important it is. If you’re going to be deciding to stop working at some point and retiring, whether it’s retiring for 10, 15, or 20 years, that’s a long time to be living on a fixed income. So you want to make sure that you have the plan in which to carry out that length of time so that it’s happy, joyous and free.

Tim Knox: Sure, sure. Do you find that a lot of baby boomers – first of all, let’s define what is a baby boomer.

Jeff Carter: Well, that’s a great question. Today in this country, there are actually 79.4 million individuals that are classified baby boomers and the last – the tail end if you will, not the leading edge. But the tail end of the baby boomers, they will be turning the last one age 50 December of 2015. So they’re basically individuals that were born between the years of 1946 and 1964. So it’s a significant time and it’s basically when World War Two ended and then our economy took off and there were a tremendous amount of babies that were born in the United States of America.

Tim Knox: Yeah. I can remember my dad coming back and I’m about your age. I was born in 1960 and he and I one time I remember, we were talking about the time when he came back from World War Two, which was in 1945, and I asked him. I said, “Well, why would they call it the baby boom?” He said, “Son, we all came back looking for women.” I will never forget that. It was just – like OK, I get it. That was a bonding moment.

So are you finding with the baby boomers who – and that’s who you’re focusing your book on primarily. Are they prepared? Are we – now that people are living longer and you got to stretch those dollars out a little more, are you finding your clients especially the ones that are our age and older, are really prepared for retirement?

Jeff Carter: Well, the answer to that question is it depends and what I mean by that Tim is if you listen to the news reports and you listen to the commercials that Wall Street firms play on different radio and TV commercial spots, they all shoot for this grandiose number. What is your number? You need $1.5 million to live retirement the way you want to live it.

Well, the fact of the matter is, is that we – baby boomers in our generation, we have not accumulated that sort of money. There are multiple reasons for it. The thing that we have to keep in mind is that we have been through a significant couple of overheated stock market peaks and valleys. One of them was the internet bubble that burst and then the second was the real estate bubble that burst.

So we all had really good intentions and we were savings and we were banking on a lot of us to sell our home when we’re ready to retire. As you recall, the real estate market just exponentially increased over a period of several years.

When we got to about 2006, most home values had doubled. So if you had bought a house for a half a million, it was now worth a million as an example. Looking at that, people felt pretty confident and comfortable that hey, when I get ready to retire, I will sell my home and I will have plenty of equity in it and that’s going to be a big part of my retirement plan.

Well, we all know what happened to that plan. It evaporated when the real estate market went south. Then we had the stock market debacle. Not only the internet bubble that burst back in the 80s. But we also had in 2008 the stock market crash.

So there has been a lot of contributing factors that have kind of played havoc in our planning as a generation. So I really – I don’t agree wholly with the message that is sent out from Wall Street and the banks and the investment companies and insurance companies saying that we’re in big trouble and baby boomers are never going to be able to retire.

Actually in the book that I’ve written, I talk about no matter how much you saved or how little you saved, there is planning you can do to position yourself so you can retire.

So it’s good for people to know that you don’t need to have millions of dollars accumulated in a savings account to retire. There are some strategies you can employ that will allow you to retire and obviously we will all have to adjust our wants and focus more on what our needs are. But that’s OK. At the end of the day, it’s – money doesn’t make you happy. It’s spirituality. It’s family. It’s love. It’s all of those things that you can’t buy with money that make you happy. So that’s the good news.

Tim Knox: Well, that is good news. Money doesn’t buy happiness, but it sure is nice to have.

Jeff Carter: Yeah, it helps.

Tim Knox: It helps. It does help. Well, let’s talk a little bit about the book. Let’s dive in here. There are – I think you’ve got three parts to the book that – part one, part two, part three. Talk about each one of those parts and how – how do they apply to your audience?

Jeff Carter: Well, that’s a great question. I appreciate you asking that. So, primarily what we have to do when we’re talking about retirement income planning is we have to have a roadmap to traverse down. I like to use the acronym of SMART.

S standing for specific, meaning the mind is able to picture a goal better if it’s a written description in a very detailed manner.

M standing for measurable, meaning you evaluate your progress and you recognize success. So a goal is measurable.

A is for achievable, meaning you maintain a positive outlook about realizing your goal by making it achievable.

R for realistic. Develop increased self-confidence and positive self-esteem by setting realistic goals and you notice the word “realistic” is in this description a lot because obviously you have to do the planning that you can do that’s within your means financially.

T for time. Goals are time-sensitive and no one will benefit from working towards an elusive destination.

So basically with that in mind, what I did is I said, “OK. Let me lay out a roadmap for people to turn their retirement savings into a guaranteed lifetime income that’s going to allow them to prepare for their longest vacation of their life, which is their retirement.”

So I broke the book into, as you mentioned Tim, into three sections. The sections, the first is the importance of a plan. So what basically that is going to talk about is what are the steps that we have to go through to develop a plan and gather the information necessary so that ultimately it can be implemented.

So chapter one is defining your goals and as I mentioned, we talked about that in the acronym of SMART. Then chapter two is gathering all of the pertinent information that’s necessary and in the book, I have – there are links for people to go visit and download the different tools that they’re going to need. As an example, gathering data, there’s a checklist that they can utilize that will keep them on track and show them exactly what to do.

Chapter three is about analyzing information. Obviously you’ve gathered all of these facts. But now what does it all mean? There’s a worksheet to help you do that and then we move on to chapter four, which is evaluating your options.

That’s very important because there are so many different financial products in the marketplace that one has to decide whether or not it’s valuable to their situation and what are the pros and cons of using those vehicles.

So we get into discussing that. Then I lay out actually some specific strategies in the book. There are four specific strategies that one can employ, if they choose to, that may fit their situation.

Obviously that will be determined by going through the process or the steps I’ve just described. Then chapter five is – of part one is implementing your plan. Obviously now you’ve got all the information. You’ve done the analyzing of the information and now you need to put the plan in action. Then chapter six is how do you monitor your plan, to make sure that it is on course.

As you know, if we use some medical analogies here, if you have high blood pressure, you’re going to check your blood pressure at home periodically to make sure that it’s not spiking and make sure the medicating that the physician has prescribed is working properly. Well, doing your financial analysis and monitoring of that plan takes some effort and so I walk you through how that can be done.

So basically to summarize part one of the book, we’re going to talk about planning for your retirement income. We’re going to talk about your retirement readiness checklist, the definition of retirement planning as well as life planning, because there’s more that goes into retirement planning than just numbers. There’s also life planning which talks about how is retirement going to affect you personally, psychologically, emotionally, mentally.

There are a lot of things that are triggered when a person retires, that they really don’t think about until after they’ve transitioned out of the work world into a retirement world. So we will touch on that in the book as well.

Tim Knox: There really is a lot to know and there really is a lot to learn. I think it’s very helpful to have someone like you guide us down this path because again, I am your target demographic here and as you were mentioning earlier, I’m inundated daily with bad news. I am not going to – I am going to outlive my retirement. I’m going to have to get a reverse mortgage. I’m going to have to move in with my kids. It seems like we are constantly barraged by this sort of thing. So I think it’s very important to have someone like you and something like this book that will help you plan.

I’m an old entrepreneur too and I think one of the reasons people fail in business primarily is a lack of planning and I think that could be the same here. A lot of planning, if you’re going to have the longest vacation of your life, you need to plan for it and you need to figure out how to finance it, correct?

Jeff Carter: Correct, Tim. You touched on a very, very important point, which I’m a firm believer in what you think about, you become. So if in fact all you’re doing is hearing negative messages in the media because they’re trying to motivate people through fear and greed with their marketing, you tend to take on that message and think that well, that’s me. I’m never going to be able to do it. I just got all of these things stacked up against me. It’s just not going to happen. So why even try?

What I have found for me personally is that if I think negative thoughts, I will become negative. If I think positive thoughts, I will become positive. Obviously, the fact of the matter is, is if you have $10, you have $10. But there are things that you can do with those $10 that are wise versus foolish. We need to keep in mind that as you said, it’s really about the planning. Let’s plan on what you need to do based on where you are in life and let’s help you move forward to get to where you ultimately want to be. So thank you for bringing up that very important point.

Tim Knox: Yeah, great advice. Let’s talk a little bit about some of the mistakes that you’ve seen people make over the years. You’ve been doing this for 25 years. What are some of the biggest mistakes you’ve experienced people making?

Jeff Carter: Well, that is a great question because there’s many. I think overconfidence in their investing skills. I’ve seen it. I’m sure you’ve seen it. You may go to a social gathering and you will be talking to somebody and they will say, “You see that gentleman over there? Yeah, he’s really successful. He just bought a bunch of stock and he rode it up from $10 to $40 and he sold it and he walked away with a wheelbarrow full of money.”

So of course the first thing is, is you want to find out, “OK. What did this guy do? Because I want to do the same thing,” and you never really hear – if you reflect back on it, you never really hear someone talk about all the money they lost in a deal at a social gathering. It’s only about the money they made. So what you tend to see over time when you do what I do for a living is you find that it’s the old tail wagging the dog, not the dog wagging the tail scenario.

So you’ve got people chasing returns, thinking that they’re going to jump in and make a bunch of money, because their cousin or their brother or their associate at work did it or so they said they did it. They’re going to try to get in on that action and they attempt to do it and they lose money.

So now all of a sudden, they are in a place psychologically where they are not sure what the right decision is. Then they start making bad decisions and then they get overconfident thinking that well, I’ve learned my lesson and I’m going to do this maneuver now and I’m going to make up everything I’ve lost in the past.

That happens a lot and it’s really a psychology that goes all the way back to the caveman. The old hunt and gather mentality. You would leave the cave with a club and you would go out into the woods and you would have to find something and drag it back to feed the family. So there are some biases that we have as human beings that go back thousands of years that are perpetuated from one generation to the next.

What I see is there are some cognitive biases that come into play, that really cloud people’s judgment and hampering their ability to make rational and impartial decisions.

One of them is called the “gambler’s fallacy” and basically it’s one of the biggest issues that individuals face when they’re investing. They’re emotionally-driven as human beings, as we all are, and we tend to put a tremendous amount of weight on previous events believing that our future outcomes will somehow be the same.

So what I’m trying to say here is that past performance is no guarantee of future results and despite that statement being plastered everywhere across the financial universe, we human beings consistently dismiss that warning. Instead we focus on past returns, hoping and expecting that that’s going to happen in the future.

One of the other things Tim that I find is pretty fascinating is the herd bias and that is an unconscious action that us humans tend to go with the crowd. So much of the behavior relates back to wanting confirmation of our decisions and also needing to be accepted. Throughout the process, it’s rooted in the belief that if everyone else is doing this, then geez, I must do it too because it’s accepted. So basically it’s conforming to the norm socially and that is what drives stock market movements.

So when the market takes off for no given reason and the fundamentals aren’t there and we’ve got all these problems in the world economies and government debt, et cetera, and the stock market keeps going up, and people look at each other and wonder how in the world is this happening, well, it’s the herd bias that drives it, because everyone else is doing it. So everybody wants to jump on and go for the ride.

The same thing will happen when the market goes south, which inevitably it always does and it will again. You will see the herd bias drive itself just as it drives it into higher territory. So that’s a very interesting concept that we should all learn from but we tend to forget.

Tim Knox: Yeah. There are a couple of things that you touched on and in the pre-call materials, a couple of things that really stood out for me, number one, was the human brain is simply not wired for investing. Number two, planning for a retirement is fundamentally different from managing money on a daily basis. I find both of those concepts so interesting. What are your thoughts there? How do people get their head around it? If we have been genetically predisposed to hunting and gathering and not save over all of these many years and then if we think we’re managing our money on a monthly basis, our retirement is just going to be there and that’s not the case.

Jeff Carter: Well, great point. What I like to use as an analogy is when we’re all younger and we’re hustling, working, raising a family, and trying to save the best we can based on our circumstances, we have what I call a wealth accumulation hat that we wear.

Basically it drives us to try to earn money, make money and save money and grow money. We’re in that mindset. We’re in that psychology from the time that we get our first job until the time we decide to retire. So that’s the majority of our adult life.

Now all of a sudden, you come to a point where a fork in the road, where it’s now time to slow down and do some other things that you want to do in life and you need to break away from the work world to do that. So you decide to retire. Now it’s time to put on what we call the wealth preservation hat. Well, the wealth preservation hat is completely 180 degrees in the other direction of the wealth accumulation hat.

So now we’re trying to take all of these habits that we have formed over many years of working and say, “OK. We no longer want to try to grow our assets aggressively. We want to preserve what we have and create that – use that money to create a stream of income that will pay out to us for the remainder of our life, making sure that we don’t outlive that bucket of money, because obviously we’re not going to be able to go back to work later in life. We probably won’t want to and most likely won’t be able to, because of possibly health or not having the up-to-date talents with the ever-changing economy and the world.”

As you and I both know, technology changes by the hour. So what you knew five years ago is not even really relevant today and it’s exponentially exploding and it’s going to continue to happen for the remainder of our lives.

So once you’re out of the workforce, it’s kind of hard to keep up with the changes and keep your finger on the pulse. So going back to work probably isn’t a real great option.

So that’s the primary difference I see Tim is between accumulating and then switching and going in a different direction to draw down on those savings to cover your essential monthly living expenses and retirement.

Tim Knox: Exactly. So what is your advice then? If baby boomers are looking to retirement and whether they’ve done planning or not – I think all of us are concerned about what’s coming. We can’t predict the stock market or the economy. What are boomers supposed to do about this concern?

Jeff Carter: Great question. My first recommendation is educate yourself and I think a great place to start would be to read my book. I have taken 25 years of frontline experience working with people that have millions of dollars all the way down to people that have very little. I have seen all of the mistakes that can be made. I know all of the strategies that can be employed and I have taken all of that knowledge and put it between the covers of my book. I’ve held back no secrets. Everything is in there that will take people from A through Z, giving them all of the pertinent information they need to educate in themselves and become better informed.

The second part of that Tim is once you know what you have to do, you have to take action. Without action, nothing happens. So the next step would be once they go through the book, they need to start at point A and they need to start planning. They need to start walking through the tasks that are outlined in the book and tackle them one at a time.

Now some people may say, “I don’t like doing that. I don’t even like balancing my checkbook. That’s fine.” You can engage the services of a professional. If you decide to do that, at least when you go out and look for one, you’re now going to be able to talk their language because you’ve read this book and it educates you from an insider’s perspective. So you are going to know the questions to ask. You’re going to know what kind of people to look for to help engage you in the process and hold you accountable.

In my personal life, using myself as an example, what we’re talking about right now obviously is second nature to me. This is what I do for many, many years. However, there are things that I don’t do all of the time. So I hire professional coaches to help me. One of the things I did is I hired a professional coach to help me write my book. I had all the knowledge. I just needed someone to hold me accountable to put the words on paper.

I tried to work on that for 10 years on my own and it wasn’t – I would pick it up. I would write a few words. I would set it down and this went on for 10 years. So I’m a perfect example of needing professional help to get something done that I’ve dreamed of doing for a long, long time but I needed somebody to help me and hold me accountable and that’s why I hired a professional coach to help me stick to a timeline to get this book written and published.

So I would recommend the same for anyone. Obviously if you have a urinary tract infection, you’re certainly not going to go to a podiatrist. You’re going to go to a urologist and it’s the same thing with money. It’s the same thing with your automobile. It’s the same thing with repairing your computer.

If you don’t do it every day, you don’t know. You don’t know what you don’t know. That’s OK. We’re all that way. You have to trust other people and the way that you’re going to get there is by first educating yourself. I think my book is a great place to start.

Tim Knox: Well, I agree. Going through the book, I was impressed by not only the amount of experience that you’ve had but the real world examples, you have done this professionally for so long with so many clients. I think there are a lot of books on the market now that preach this sort of advice. But they do not have the backbone and years to back it up and you certainly do, so kudos to you on that.

Now let’s talk in a few minutes that we have left specifically. What can our audience, our baby boomers and even – I think anyone in general I think can benefit from the advice in this book. But what can the audience expect to learn by reading the Retirement Boom?

Jeff Carter: Well, I think to sum it up, they are going to learn how to access their retirement savings no matter how much or how little they have and be able to create a guaranteed income stream that will last them the rest of their lives.

So if you would think of it Tim as designing a personal pension plan and a personal pension plan is what social security is. So your social security benefit, you’ve worked your whole life. You’ve had W-2 income or possibly self-employment income. But either way, there has been FICA taxes paid and those taxes that have been paid are to cover your social security benefit and your Medicare benefits when you retire.

That’s the same thing you can do with your retirement savings and I teach you how to do that in the book. Also beyond that, there are some other strategies that you learn if you have more of a propensity to be a little bit more aggressive with your investments and you still want to be in the stock market. I explained to you some strategies that you can employ in the book that will help you do that and minimize your risk in the process.

So that’s a couple of things that they will learn. The other thing that I would like to mention Tim and I was reminiscent in mentioning this earlier, I didn’t write this book to make money. That was not my goal. On a personal note, I have had in my family both immediate and extended family, I have had challenges with individuals that have had various addictions, whether they be alcohol or drug. I have seen the wonders of what a 12-step program can do in people’s lives.

I have seen it take people’s lives from absolute shambles to turning them completely around and having a life that anyone could hardly ever even dream of. It takes them through that process obviously. If anyone knows about the journey of a 12-step program, it’s really about spirituality and it’s about taking personal responsibility and it’s learning about how not to be selfish and to be selfless and help others.

So 50 percent of the proceeds from this book are going to be donated to a 12-step program that was created here in Phoenix, Arizona called The Crossroads and they’ve – since 1960, they have helped tens of thousands of people recover from the despair of different addictions into productive, happy citizens.

So 50 percent of the book proceeds will go to that charity to help with that endeavor and then the other 50 percent will go to cover the cost of printing books and marketing to get the word out about the book, so that I can help the Crossroads’ charitable foundation.

So I wanted to mention that and that’s – if somebody decides to get involved in buying the book, not only will they be helping themselves, but they’re going to be helping other people and I think that that’s a beautiful thing.

Tim Knox: I agree totally. Jeff Carter, this has been fascinating. I think we could go on and on forever. Where can our listeners learn more about the book? Where can they go purchase the book and learn more about you?

Jeff Carter: Thank you Tim. It’s www.RetirementBoom.org. So that again is www.RetirementBoom.org and that website will give them access to information about me, opportunity to buy the book. There’s also a link to my blog. So if they would like to share any feedback, I welcome that and Tim, I have had a wonderful time with you. I feel like I’m sitting across the table from an old friend. So thank you for making me feel comfortable.

Tim Knox: Well, it has been a pleasure and again I think you and I can talk much more on the subject. So the website is www.RetirementBoom.org, Jeff Carter, 25 years as a financial adviser and strategist. I encourage everyone to go get this. I am your target audience Jeff. I’m going to read the book and boy, if you can help me, you can help anybody.

Jeff Carter: We can help you Tim. There is nobody that’s beyond help.

Tim Knox: Well, would you tell that to my wife? Jeff Carter, it has been a pleasure. Folks, go check out this book, the Retirement Boom. The website www.RetirementBoom.org. Jeff, it has been a pleasure. I hope to have you back on again soon.

Jeff Carter: My pleasure Tim. Thank you for the opportunity and God bless you.

The post Tim Knox Interviews Jeff Carter Best Selling Author about his book Retirement Boom™ appeared first on Retirement Planning.

February 5, 2016

How Much Is My Business Worth?

A much better question to ask:

What is the most I can get for my business under the most favorable terms and conditions?

The answer to this question is found by developing your business exit plan.

What exactly is a Business Exit Plan and how do you create it? To determine where you stand in developing your Exit Plan take the following quiz…

1) Do you know your primary planning objectives for leaving the business:

a. Departure date?

b. Income needed to achieve financial security?

c. To whom you want to leave the business?

2) Do you know how much your business is worth?

3) Do you know how to increase the value of your ownership interest through enhancing the most valuable asset of your company – the employees?

4) Do you know the best way to sell your business to a third party which maximizes your cash, minimizes your tax liability and reduces your risk?

5) Do you know how to transfer your business to family members, co-owners or employees while paying the least possible taxes and enjoying maximum financial security?

6) Have you implemented all necessary steps to insure that business continues if you don’Have you provided for your family’s security and continuity if you die or become incapacitated?

If you only answer “yes” to a few of these questions and not ALL of these questions you will not successfully exit your business maximizing your value and minimizing your taxes.

If you have questions or comments call me at 888-252-7941. It’s a great way to take the first step on your road to a successful exit.

Jeff Carter, RICP, CSA, RFC, LUTCF has spent the last 25+ years working with individuals and business owners creating retirement income plans.

The post How Much Is My Business Worth? appeared first on Retirement Planning.

October 28, 2015

Key Retirement Income Risks

Understanding the risks you may face in retirement has never been more important. There is an increased need to protect retirement income from market downturns, low interest rates, and increased longevity. Since fewer workers in the private sector retire with traditional defined benefit pension plan income, the number of those who are vulnerable to these risks is increasing.

Although the possibility of stock market losses has traditionally garnered greater attention, low interest rates over an extended period of time can also be very damaging to the retirement security of those saving for retirement, as well as those drawing income during retirement.

Guaranteed lifetime income products help protect retirement income from market downturns, as well as an extended period of low interest rates, while guaranteeing that income can be generated for life.

Currently, the median retirement savings in 401(k) plans, 403(b) plans, and IRAs for households approaching retirement is approximately $80,900 at the end of the first quarter of 2013. The income that these savings can generate will not be sufficient for the vast majority of retirees, even with Social Security benefit retirement income.

Therefore, it is imperative that individuals save more in their workplace retirement plans and personal investment accounts while measuring their progress in terms of an income goal, not a savings goal.

After all, once you retire, you will need to shift gears from saving money to managing the income from those savings. The challenge is withdrawing enough money to cover your needs without depleting your savings before your death.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Key Retirement Income Risks appeared first on Retirement Planning.

October 14, 2015

Healthcare Costs

Most Boomers look forward to retirement as a time to shift gears and enjoy a slower pace of life. However, that reality can quickly change and include sticker shock when it comes to paying for health care. A couple retiring today is expected to need approximately $240,000 to cover health care costs in retirement.

Rising health care expenses are forcing people to make educated decisions now more than ever concerning at what age they should choose to retire. And of course some people do not have a choice about when they retire because health issues or occupational restrictions can play a role. So it is critical to plan for the considerable cost of health care well in advance by making it part of an overall retirement income planning process.

As life expectancies increase and people spend more years in retirement, the money set aside to pay for health care will have to last longer as well. Clearly, factoring in health care expenses has become a critical part of retirement income planning.

The Medicare health insurance program is still the primary source of health coverage for American retirees. Most individuals automatically qualify for basic Medicare hospital insurance (known as Part A) as soon as they reach age 65. This coverage costs nothing if you or your spouse paid Medicare taxes during your working years.

However, Medicare medical insurance (known as Part B), which covers doctors’ services, outpatient hospital care, and some other medical services, such as physical and occupational therapy and some home health care, is not free. You pay a monthly premium for Part B, and there is no annual limit on your out-of-pocket expenses as there is with many private insurance policies.

One option to consider is Medicare Advantage plans, which combine Medicare Parts A and B and supplemental coverage into a single policy. Private insurance companies manage Medicare Advantage plans, and they can offer lower premiums and/or better benefits than the traditional Medicare where each part is treated separately.

As we all know, prescription drug costs have also gone up each year. To cover prescription drug cost in retirement, you can also purchase Medicare Part D prescription coverage as part of a Medicare Advantage plan.

If you retire before age 65, you cannot take advantage of Medicare right away. So if you do not have other coverage in the interim, you will need to find a source to pay for your medical insurance while you await eligibility for Medicare. Your choices may include paying to continue your current employer coverage for a specified time under COBRA, joining your spouse’s company health care plan, purchasing your own medical insurance policy through a local insurance broker,

utilizing Veteran’s Administration benefits if you are a veteran, or Medicaid if you qualify.

So what is COBRA?

The Consolidated Omnibus Budget Reconciliation Act (COBRA) health benefit provisions amend the Employee Retirement Income Security Act, the Internal Revenue Code and the Public Health Service Act to require group health plans to provide a temporary continuation of group health coverage that otherwise might be terminated.

Cobra is a Federal law that may allow you to temporarily keep health coverage after your employment ends, or if you lose coverage as a dependent of the covered employee, or another qualifying event. If you elect COBRA coverage, you pay 100% of the premiums, including the share the employer used to pay, plus a small administrative fee.

COBRA can be used as a bridge until you qualify for Medicare or purchase another health insurance policy. It requires that continuation coverage extend from the date of the qualifying event for a limited period of 18 or 36 months. The length of time depends on the type of qualifying event that gave rise to the COBRA rights. A plan, however, may provide longer periods of coverage beyond the maximum period

required by law.

When the qualifying event is the covered employee’s termination of employment or reduction in hours of employment, qualified beneficiaries are entitled to 18 months of continuation coverage.

You may also want to consider purchasing long-term-care insurance. The cost is based on age, so the earlier you purchase a policy, the lower the annual premiums will be.

One of the biggest misconceptions Boomers have is that Medicare covers long-term care. Medicare does not pay the largest part of long-term care services or personal care, such as help with bathing, or for supervision often called custodial care. Medicare will help pay for a short stay in a skilled nursing facility, for hospice care, or for home health care if you meet the following conditions:

1. You have had a recent prior hospital stay of at least three days.

2. A Medicare-certified nursing facility admits you within 30 days of your prior hospital stay.

3. You need skilled care such as skilled nursing services, physical therapy, or other types of therapy.

If you meet these conditions, Medicare will pay for some of your costs for up to 100 days. For the first 20 days, Medicare pays 100 percent of your costs. For days 21 through 100, you pay your expenses up to $140.00 per day, and Medicare pays any balance. You pay 100 percent of costs for each day you stay in a skilled nursing facility after day 100.

Planning for health care expenses in retirement has never been more important. By carefully considering your needs, expenses, and financial resources ahead of time, you will likely be in a better position to handle these costs during retirement.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Healthcare Costs appeared first on Retirement Planning.

October 12, 2015

Retirement Savings and Peach Trees…What do they have in common?

Developing a retirement income plan one must consider the importance of liquidity. A liquid asset is an asset that can be converted into cash quickly with little or no loss in value. Examples of Liquid assets such as certificate of deposit or money market account would be considered the same as cash.

The question is – what percentage of your assets should be liquid as you enter retirement?

The thought of being able to access your assets at any time is very appealing. However, when it comes to generating income during retirement, having your assets liquid at all times may increase the risk that your money won’t last as long as you do. Here’s why….

Your retirement peach tree! Imagine that your retirement assets are one peach tree with branches (your principal) producing enough peaches (income) so you can live comfortably during retirement. In the beginning, you may think there’s no harm chopping off a branch or two (liquidity) for firewood (discretionary spending) because the tree is large.

Doing this, however, impacts your tree in two ways over time:

The number of peaches produced would be lower

If you keep chopping off branches, there may come a point when your tree cannot produce enough peaches and cannot grow new branches, ultimately reducing the life of your tree. No more tree, no more peaches.

Now, think of your retirement savings as being multiple peach trees. Instead of one tree, you have many trees. You fence off some trees – giving up your access (liquidity) – so that their only job is to produce enough peaches to cover your necessary expenses. The remaining trees are for producing peaches and firewood that you can access when needed. With this approach, you have established sources that solely produce income and other sources to meet your liquidity needs.

Should you create one peach tree or an orchard? As you enter into retirement, one of the many financial decisions facing you is what to do with the assets you accumulated for retirement. One of the main reasons that you save for retirement is to produce income (peaches) for your necessary expenditures (essentials), like paying your mortgage/rent, food and utilities, so you can live comfortably during these years. In addition, a portion of your income should be independent from and not reliant on market performance. As you consider your asset distribution and financial strategies for retirement, here are some things to keep in mind:

Take a long-term view when retirement planning since the length of your retirement years is an unknown

Explore financial products that can provide income for your lifetime (annuities) and that of your spouse’s lifetime

Create a distribution/withdrawal plan to access different pools of assets at certain points in time during retirement (laddered annuity orchard)

Work with a financial professional for developing your retirement income plan (orchard of peach trees)

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Retirement Savings and Peach Trees…What do they have in common? appeared first on Retirement Planning.

October 7, 2015

Inflation Risk

You may not have given inflation much thought. The double-digit inflation rates of the seventies and eighties are only a distant memory. But because inflation lowers the purchasing power of money, even a modest level of inflation can take a significant toll on your retirement purchasing power and lifestyle over time. That is why it is important to take inflation into account when developing your retirement income strategy.

Inflation is the rise in prices over time, with the result that a dollar will buy fewer and fewer goods and services, which decreases your purchasing power. Even low inflation is threatening to the security of those who rely on fixed incomes, as many retirees do. We Baby Boomers can remember when a McDonalds pure beef hamburger cost $0.15, and today that same hamburger cost $1.29. Now that is inflation!

The impact of inflation can mean loss of purchasing power. Less purchasing power can result in hard choices regarding the necessities of life such as food, medical care, gasoline, home utilities, etc. Indeed, during periods of runaway inflation, individuals may find it necessary to move in with family members or downsize to a smaller residence.

Everyone understands that as prices go up, purchasing power decreases because each dollar buys a smaller portion of goods and services. But when you look at inflation in concrete terms – the cost of things you pay for every day – its impact is more understandable.

Consider this: At three percent inflation, the monthly phone bill you pay for $100 today might run $103 next year. While you might not think that is a big deal, factor those three percent increases over a longer period, and it takes a serious toll on your standard of living. If prices continue to grow by three percent each year, in 25 years you will need $209 to pay for that same phone bill, which is an increase of 109 percent. So if your income is not keeping up with the pace of inflation, you will lose financial ground over the long term.

Sound retirement planning, therefore, requires that you take the effect of inflation into account. Thankfully, Social Security benefits receive annual cost-of-living adjustments. That is helpful, but most people cannot survive on Social Security alone, so this is not a viable solution to bank on when planning to offset inflation risk.

How can you minimize the effects of inflation on your retirement income? Although you certainly cannot control the rate of inflation, there are some steps you can take to minimize the financial impact of inflation, regardless of how close or far away you may be from full time retirement. Plan for both best and worst case scenarios:

Include both conservative and aggressive inflation rates in your future assumptions and estimates. Make sure you also adjust your assumptions regarding required retirement income to compensate for actual inflation rates.

Maximize your savings and investments to meet worst-case inflation scenarios.

Include the impact of future taxes to determine how to allocate your investments between taxable, tax-deferred, and tax-advantaged programs.

Do not wait! Procrastination is one of the primary reasons that inflation begins to take its toll. Even small positive steps can minimize the effects of inflation over time.

If you are receiving retirement income, include an inflation assumption in your income needs. Determine the percentage of your budget spent on items that increase at a rate greater than inflation. Compare your results with the average inflation rate to see how your spending habits vary.

Consider incorporating equity investments in your retirement income portfolio to increase the likelihood of staying ahead of inflation.

Develop a sound tax strategy around the goal of keeping a greater share of what you earn during retirement.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Inflation Risk appeared first on Retirement Planning.

October 1, 2015

Guaranteed Lifetime Income Utilizing Annuities

The simplest way to provide lifetime income is with an income annuity. You transfer a lump sum (known as a premium) to an insurance company when you retire, and the insurance company pays you a monthly check for life. It is a guaranteed income to supplement traditional guaranteed income sources like Social Security and defined benefit pensions. You select a payout option, including payouts for a certain period of time, lifetime income, or income for joint lives. Stock market swings does not impact the monthly income payment, and you receive preferential tax treatment on income from after-tax savings by virtue of the Internal Revenue Code.

Over my 25-year long career, I have been asked hundreds of times, “What is the best annuity?” The answer to this question depends on your unique situation. After going through the retirement income planning process you have just read about, the answer will present its self. Below are a few types of annuities that may be used in your retirement income plan.

SPDA (Single Premium Deferred Annuity) helps you grow and protect funds for retirement. You can purchase one before or after you retire. The money in your annuity, which you invest as a lump sum, earns a guaranteed, fixed rate of interest for a period you select. You do not pay taxes on your earnings until you withdraw them. All guarantees are subject to contract terms, exclusions and limitations, and the claims-paying ability of the issuing insurance company.

DIA (Deferred Immediate Annuity) allows you to build your own “pension-like” stream of guaranteed lifetime income by offering a way to help guarantee that you have the retirement income you need to cover everything your retirement plans have in store for your entire life. A stream of guaranteed lifetime income starts when you need it to, up to 40 years in the future. You can tailor your payout option and other features to meet your unique retirement planning needs including leaving a legacy to your loved ones. The income payments are locked and free from market volatility. All guarantees are subject to contract terms, exclusions and limitations, and the claims-paying ability of the issuing insurance company.

SPIA (Single Premium Immediate Annuity) provides you with a worry-free stream of guaranteed income. You can purchase a SPIA before or after you retire. The money in your annuity, which you invest as a lump sum, generates a stream of income paid out to you for life. The amount of income you receive depends on several factors, including your age, gender, premium amount, interest rates in effect, and your chosen payout option. All guarantees are subject to contract terms, exclusions and limitations, and the claims-paying ability of the issuing insurance company.

FIA (Fixed Indexed Annuity with Lifetime Income Options) helps protect your financial future in these important ways: The movement of a stock market index (i.e. S&P 500 Index) calculates the growth of your money. If the index goes up, you receive a portion of the upside (depending on the contract provisions). If the index goes down and results in negative returns, you receive zero percent interest crediting, and you do not lose previous gains or value due to the market

downturns. This is because the minimum index credit applied to your account value is guaranteed never to be less than zero percent. So even when the index shows a negative performance over the contract calculation duration, your account value remains intact. Any earnings grow tax-deferred until you take withdrawals by virtue of the Internal Revenue Code. If you should die while your annuity contract is in force, your heirs will receive a death benefit amount equal to the contract value or the total guaranteed value, whichever is greater. You can

choose to purchase a guaranteed minimum withdrawal benefit rider that will provide you with a guaranteed income stream for as long as you live. All guarantees are subject to contract terms, exclusions and limitations, and the claims-paying ability of the issuing insurance company.

VA (Variable Annuity with Fixed Payout Options) is a contract between you and an insurance company, under which the insurer agrees to make periodic payments to you, beginning either immediately or at some future date. You purchase a variable annuity contract by making

either a single purchase payment or a series of purchase payments. A variable annuity offers a range of investment options. The value of your investment as a variable annuity owner will vary depending on the performance of the investment options you choose. The investment options for a variable annuity are typically mutual funds that invest in stocks, bonds, money market instruments, or some combination of the three.

Although variable annuities are typically invested in mutual funds, variable annuities differ from mutual funds in several important ways.

First, variable annuities let you receive periodic payments for the rest of your life (or the life of your spouse or any other person you designate). This feature offers protection against the possibility that, after you retire, you will outlive your assets.

Second, variable annuities have a death benefit. If you die before the insurer has started making payments to you, your beneficiary is guaranteed to receive a specified amount – typically at least the amount of your purchase payments (less any withdrawals or surrenders). Your beneficiary will get a benefit from this feature if your account value is less than the guaranteed amount (per contract provisions) at the time of your death.

Third, variable annuities are tax-deferred. That means you pay no taxes on the income and investment gains from your annuity until you withdraw your money. You may also transfer your money from one investment option to another within a variable annuity without paying tax at the time of the transfer. When you take your money out of a variable annuity, however, you will be taxed on the earnings at ordinary income tax rates rather than lower capital gains rates. In general, the benefits of tax deferral will outweigh the costs of a variable annuity only if you hold it as a long-term investment to meet retirement and other long-range goals.

You choose from various variable investment options (i.e. stock or bond mutual funds), which will fluctuate, so your total contributions and earnings may be worth more or less than their original value when you redeem them. All fixed payout option guarantees are subject to contract terms, exclusions and limitations, and the claims-paying ability of the issuing insurance company.

Variable annuities have become a part of the retirement and investment plans of many Americans. Before you buy a variable annuity, you should know some of the basics and be prepared to ask your financial professional many questions about whether or not a variable annuity is right for you.

Ask questions about the general description of variable annuities such as what they are, how they work, and the charges you will pay. Before buying any variable annuity, however, you should find out about the particular annuity you are considering, Request a prospectus from the insurance company or financial professional, and read it carefully. The prospectus contains important information about the annuity contract, including fees and charges, investment options, death benefits, and annuity payout options. You should compare the benefits and costs of the annuity to other variable annuities and other types of fixed annuities.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Guaranteed Lifetime Income Utilizing Annuities appeared first on Retirement Planning.

September 23, 2015

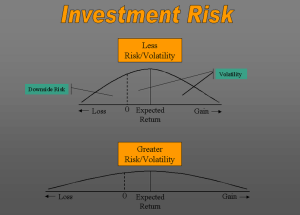

Investment Risk

The more risk you take, the higher the potential rewards are. However, most successful investors do not always take the highest risk nor do they try to avoid it. Avoiding the risk altogether can be a risk itself. Money that you have not invested will likely lose value due to inflation. So potentially making money through investments requires you to consider the various kinds of risk and find a balance among a range of investments to manage that risk.

Risk tolerance is to some degree a function of time. Investors who have more time (generally ten years or more) to let their investments grow may be in a better position to use higher-risk and higher-yield investments than someone who needs their money sooner. So you may wish to consider and reconsider both your feelings about risk and your investment time horizon when choosing investments for your retirement savings accounts.

It is important to remember that bond portfolios will decline in value with a rise in interest rates. For example, older bonds paying a lower rate of interest becomes less valuable than a newer one that pays a higher rate. Higher interest rates also tend to reduce stock prices, because they increase the cost of borrowing for companies. Both stocks and bonds carry the risk that a particular company or industry will not perform as expected.

Another investment risk exists if changes in the exchange rate between currencies occur and can affect the value of foreign investments, for better or worse. This type of risk can also affect investments held by U.S. companies issuing stocks or bonds, changing the value of those investments as well.

One strategy to help reduce investment risk is asset allocation and diversification. Asset allocation is the process of investing your money in various types of investment asset classes (such as stocks, bonds, and fixed value investments), thereby spreading out your investment risk.

Diversification takes asset allocation one step further by investing in a variety of investments within those asset classes. Since different investments react differently to varying market conditions, asset allocation and diversification should work in tandem in order to help manage

the risk you might face if you held only one type of investment in one asset class.

It is highly recommended that you work with a retirement income planning professional throughout this process. Please keep in mind that asset allocation and diversification concepts do not ensure a profit or protect against a loss in a declining market, and it is possible to lose

money by investing in securities.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Investment Risk appeared first on Retirement Planning.

September 17, 2015

Longevity Risk

Your Retirement Income Plan should take into account longevity risk. Buying longevity insurance is an option when purchasing a lifetime payout annuity. Instead of guessing how to stretch your retirement investments out over an uncertain lifetime, longevity annuities let you defer payments up to 40 years into the future. The idea is that you can plan a retirement until the annuity kicks in and then receive annuity income after that until death.

In early 2015, the Treasury Department announced a final rule to facilitate access to longevity annuities in workplace retirement plans and individual retirement accounts.5 The Treasury Department made lifetime income options more readily available in qualified plans. This rule will help enhance retirement security at a time in Americans’ lives when most are vulnerable to outliving their financial assets or facing reduced standards of living. The advent of qualifying longevity annuity contracts (QLACs) will greatly advance retirement security in the United States.

The Treasury Department’s new rule allows the value of longevity annuity contracts, up to certain limits, to be excluded from calculations for required minimum distributions – overcoming a significant impediment to their use in qualified plans.

Government regulators also issued new guidance making it clear that plan sponsors may offer deferred income annuities in target date investment options that are designated as the default investment alternative in 401(k) and other defined-contribution plans.

Longevity risk is becoming more of an issue as the Baby Boomer Generation moves into its retirement years. With today’s longer life spans, an individual retiring at 65 will most likely live another 20 years. This reality is motivating many people who reach retirement age to put off retirement and work a few more years adding more to their retirement savings while they still have their health and a job. Your primary financial objective in retirement is to maintain a suitable standard of living for the remainder of your life. This can be a delicate trade off between wanting to spend as much as possible without overdoing it and triggering old age poverty.

The pursuit of lifetime income options in retirement plans will go a long way toward helping Americans prepare for their income needs in retirement.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Longevity Risk appeared first on Retirement Planning.

September 10, 2015

Withdrawing from Your Retirement Savings

Withdrawing from your retirement funds so you generate a steady, reliable income after you stop working presents a set of challenges. How much can you safely withdraw from your nest egg every year during retirement without running out of money? That is a question many pre-retirees and retirees ask.

Is there a magical formula to ensure that you do not outlive your savings? Unfortunately, the answer is a resounding no. Choosing a withdrawal strategy for your lifestyle requires careful decision-making. No two situations are alike, and the withdrawal strategy that works for your relatives, friends, and colleagues probably will not be appropriate for your unique needs. However, with careful planning, you can achieve an appropriate withdrawal strategy.

Jeff Carter, one of 1,204 financial advisors in the United States to earn the designation of Retirement Income Certified Professional (RICP) as of Jan. 2015. The total number of financial advisers in the United States is roughly 300,000. The RICP™ designee is trained to understand how to structure effective retirement income plans, how to mitigate risks to the plan and how to create a sustainable stream of income to last throughout retirement years. These college-level courses include: Retirement Income Process, Strategies and Solutions, Sources of Retirement income and Managing the Retirement Income Plan. Jeff has assisted Job Changers, Baby Boomers and Retirees since 1990 answering pressing retirement income planning questions.

This Post is for educational and/or general information and is not intended to provide specific legal, accounting, investment, tax or other professional advice. For specific advice on these aspects of your personal situation and/or circumstances please engage the service of professional advisors.

The post Withdrawing from Your Retirement Savings appeared first on Retirement Planning.

Retirement Income Planning

- Jeff Carter's profile

- 4 followers