Ezra Roizen's Blog

June 11, 2025

Magic Box Paradigm Audio Book

Have for years been asked to produce an audio version of the MBP.

Amazon offered to produce an AI version - and it’s live! You can grab it here.

The voice intonations are a bit funky - but it works.

The MBP in earbuds near you!

June 5, 2025

The Secret to Startup M&A

Sat down with Jacob Mullins, Venture Partner at Village Global, to break down the MBP and startup M&A as part of his VC Mastermind series.

Listen here!

April 3, 2025

MBP on the Profit Streams™ podcast

Luke Hohmann was kind enough to invite me on to the Profit Streams™ podcast.

Links are here:

🎧 Listen on Apple Podcasts: https://lnkd.in/g8D_GfEs

🎧 Listen on Spotify: https://lnkd.in/g5cQNCKS

Luke’s questions come from all different directions, which makes it a fun and free-flowing conversation, diving into topics that I don’t normally discuss. It’s very much framed in an “operator” mindset which I think folks will find both informative and practical.

Software Profit Streams™

In getting to know Luke, I also had the chance to learn about the book he authored with Jason Tanner: Software Profit Streams™. If you’re a student of the Magic Box Paradigm - then, like me, you’re probably a frameworks junkie. And wowza, is this book packed with frameworks?!

What’s also remarkable about this book is the design. I struggled to get half a dozen images in the MBP book, and they ended up looking like smudges that came off a dot matrix printer. Software Profit Streams is a work of art. Beyond being your guide to strategic frameworks, it could also anchor your coffee table selection! Both the concepts and the visualization of those concepts are tremendous.

My take on the book, much like the MBP, is that it isn’t trying to give you a paint-by-numbers approach to strategy, but is instead giving you a baseline set of frameworks that you can then debate, modify, and adjust to match your specific situation.

The book covers a lot of beachfront, from understanding customer priorities and determining pricing models to ROI calculations and financial modeling. It’s a book designed to spark your thinking and get you from zero-to-one on a great many critical topics.

Grab a copy on Amazon: Software Profit Streams™

MBP Office Hours

And there’s more. Next Friday April 11th 9-10am PT I’ll be holding MBP office hours. If you’re a paid subscriber to MBP.co then sign on and let’s discuss your big idea, partnership, and M&A questions!

Links for the office hours are here:

February 26, 2025

Urgency: Breaking it Down, So You Can Build It Up

If you haven’t already - get the second edition of the MBP here.

Startup founders have a tough time with other people’s lack of urgency. Why is everyone so slow? Can’t they see how important this is?

It comes up constantly, but what is urgency? How does it come into being? What does it take to create it? Let’s break it down so we can learn how to build it up.

Urgency = Direction % x (Reward / n x Risk)

That’s it, that’s the MBP urgency equation. As with all we do on MBP.co, we want to understand how this phenomenon works so that we can turn things in our favor.

Let’s get to it.

Urgency

The definition of urgency is typically some variant of what I found in the Cambridge online dictionary: the quality of being very important and needing attention immediately. I asked ChatGPT to define urgency and this is what I got: Urgency is the quality or condition of requiring immediate attention or action due to its importance or time sensitivity. It often arises in situations where delays could lead to negative consequences, increased risks, or lost opportunities. Urgency can be driven by external deadlines, critical needs, or a sense of pressure to act quickly.

So for something to be urgent it has to be important, and it also must require immediate action. What I like about the ChatGPT definition of urgency is it begins to speak to the consequences of urgency (increased risks, lost opportunities) and the drivers (external deadlines, critical needs). If we want to create it, then we need to understand what it’s made of.

I would add to these definitions that urgency means the state of being where someone acts with greater speed than they normally would. It’s important to remember that people get all kinds of not particularly urgent things done. They just get them done slowly. A lack of urgency doesn’t mean something will never get done, it just means it isn’t going to get done very quickly. Urgency translates to speed. What we are trying to do when creating urgency is to increase the speed at which something is going to get done.

For MBP purposes, we’re talking about understanding, and potentially increasing, the speed at which a potential strategic partner (“PSP”) is advancing an opportunity.

Direction %

The dictionary definitions of urgency give us a hazy understanding of what’s going on, but they’re frankly a bit muddled and murky. To turn knowledge into action we need greater specificity as to the underlying dynamics. The first variable in the MBP urgency equation is Direction %. 100% being perfect directional alignment.

PSP Strategic Direction

The PSP has a conceptualization of where it is going. A set of critical priorities, and how best to achieve them. For each PSP there’s a Zone of Actionability. This zone is the area within the outer bounds of the degrees of alignment required for an idea to be potentially acted upon. Some PSPs are entrepreneurial, innovative, and aggressive and their Zone of Actionability can be quite wide. For others who are very conservative the zone will be very narrow. So in understanding Direction % you’re both trying to understand how close this big idea is to perfect directional alignment, and also get a sense for how wide this particular PSP’s Zone of Actionability is.

But there’s one more thing to understand about Direction % and the Zone of Actionability: they’re moveable. The big idea and the PSP’s strategic direction affect each other. The big idea may actually change the PSP’s strategic direction, and the strategic direction may impact the big idea. The two aren’t static, but constantly evolving and adjusting - and it’s possible that they both move. Maybe they move closer together and create perfect alignment, or maybe new forces emerge that move them further apart.

Don’t underestimate the gravitational pull of a big idea, but also don’t underestimate the importance of the alignment of the big idea to the PSP’s strategic direction - PSP inertia isn’t something to be taken lightly! The big idea doesn’t exist in open space, it exists in the context of the PSP’s priorities.

Competition of ideas

In addition to existing in the context of the PSP’s priorities, the big idea also exists in relation to other competing ideas. PSP executive teams are most assuredly going to do something, at some point (they are paid to do stuff!). In fact, they will likely do many things. The question is will any of them be with you. The power of understanding urgency is in having a framework for increasing your urgency score - and in doing so - out-competing the other ideas upon which they could act.

Create the urgency required to knock the other ideas out of the way by aligning with Direction %, increasing the size of the Reward numerator, and decreasing the size of the n x Risk denominator.

Reward

The Magic Box Paradigm book is in large part a treatise on the Reward part of the equation. The Partner Big Idea (“PBI”) buildup is the development of the potential gain to be had by the PSP. As a practical guide to building Reward read the three part series on building a PBI (part 1, part 2, part 3). What I’ll add here to the topic of Reward is that it’s ultimately going to be heavily modified by the Direction %. So the stronger the alignment of the PBI is with the core direction of the PSP, the greater the amount of Urgency. As you’re building the PBI continue to work to understand the PSP’s driving priorities. It may be that the PBI is creating enough gravity to pull those priorities towards it, or it may be that you need to help adapt the PBI to better track to a set of priorities that are firmly positioned. What you don’t want is to have a PBI that exists detached from the ultimate direction the PSP is heading.

n x Risk

n is the degree of risk aversion for the PSP. This element has a multiplier effect on the amount of Risk the PSP anticipates it will take in pursuing the big idea. For example if Reward = 10 and Risk = 1, but the PSP is highly risk averse and has an n of 10 then the calculation is 10 / 10 x 1 (with the next effect being 10/10, or “1”) so even a 10x Reward return over the Risk of 1, is in fact only perceived to be even when you account for the intensely risk averse nature of the PSP.

Risk is the headwind pushing against the tailwind of the PBI. And the Risk headwind can be so powerful that it brings the PBI to a complete halt. To understand Risk we need to both develop a sense of the risk appetite of the PSP (what’s their “n” value?), as well as quantify the actual amount of Risk they would be taking in pursuit of this PBI. It might be tempting to focus the PBI conversation solely on Reward, but there’s a very good chance that the lurking monster of Risk will rise up and crush the PBI before it becomes reality.

Just as it’s safe to assume most PSPs won’t be experienced in developing full fledged PBIs, it’s just as safe to assume they aren’t great at calculating the risk of a bold new venture (often over estimating vs underestimating Risk). So you’ll likely have to help them develop a framework for considering the actual risks the venture poses. Naturally the contributing elements to Risk are going to be contextual to the situation at hand. But some things to consider are the cost to launch and operate the business line, the cost to acquire or partner with your startup, the opportunity cost of pursuing this big idea vs. alternatives, regulatory exposure, management distraction, and so on…

Once you (and the PSP) have a sense for baseline risk dynamics you’ll want to incorporate ways to de-risk the big idea. How can you show that this effort has all the earmarks of success? Customer demand is there, product launch (and market fit) and clearly achievable, distribution channels are primed, monetization is realistic. What are the areas that the PSP sees as most risky and how can you counteract those risks? De-risking will positively impact both the “n” value for risk aversion, and the aggregate value of the Risk itself.

Expanding on the PBI buildup in the MBP book, I’d add elements to the Methodology and Execution layers of the PBI that anticipate and de-risk the strategy. Get in front of the dynamics that will start to raise the larger risks and show how they can be accounted for through a well considered Method, and a thoughtful Execution plan.

Running the urgency calculation

Let’s run through an example.

Say at this moment the PBI that the PSP and you have created is about 75% aligned with their Direction, it has about 1,000 points of Reward, their organization has a medium level of risk aversion, so n=5 and the Risk of this strategy is around 100 points.

Urgency = 75% x (1,000 / 5 x 100)

Urgency = 1.5

The alternate project they are considering has 90% alignment with direction, but a smaller Reward of only 400 and much smaller Risk of just 10. It’s not nearly as big an idea, but it’s better aligned with Direction and way less risky.

Urgency = 90% x (400 / 5 x 10)

Urgency = 7.2

And pow, it’s got a MUCH higher urgency score. 7.2 for the smaller idea vs 1.5 for the big idea. Like it or not, when building PBIs with PSPs this is ultimately the calculation they are running. When you wonder why they aren’t moving faster, it’s because you aren’t aligned closely enough with their Direction, the Reward isn’t big enough, or there is just way too risk averse relative to the Risk they would have to take. If you want them to move faster, you’re going to need to change their inputs to this calculation.

Attention vs. urgency

There’s a secondary dictionary definition of urgency that’s important to understand: an earnest and insistent need. This definition of urgency has a durable quality. A need that is earnest and insistent isn’t simply going to go away. It has deep roots and is going to require attention. Most folks seriously misunderstand this deep and enduring aspect of urgency.

Many people mistake getting attention for creating urgency. There are levers you can pull to attract attention. For example by running a time limited process, or leveraging the FOMO that an opportunity is going to be gone if one doesn’t act now. In these cases attention and urgency are so close together they can become almost indistinguishable. However, as a transaction increases in complexity so does the gap between attention and urgency.

Say you’re a car dealer and you’re running a 4th of July sale. You get the customers attention with the sale banner, and you’re able to leverage the short duration of the sale period to create sufficient urgency to close the sale. Attention and urgency are almost indistinguishable. Now say you’re a startup and you leverage some exogenous force to compel a PSP to notice you. There’s a good chance you’ll get their attention. However, a startup M&A transaction is at least 1,000 times more complicated than, say, buying a car (and 1,000 times more complicated is probably a massive understatement). It’s not going to take a couple hours to get this deal done, it’s going to take months. You may get their attention based on their fear of missing a good deal, or losing an opportunity to a competitor, but if you don’t quickly leverage that attention to uncover an earnest and insistent need then their attention will quickly wear off, and their urgency will evaporate. In startup M&A getting attention and creating urgency aren’t the same, and you’ll want to make sure you mind the gap.

Risk Inversion

Pretty much every business opportunity exists within the constraints of the Urgency = Direction % x (Reward / n x Risk) calculation. However, some startups have a superpower that can transcend this calculation and fundamentally change the entire urgency game in their favor. They can change the calculation in such a massive way that the PSP’s urgency score explodes through a process I call: Risk Inversion.

December 19, 2024

Hot Take #6: Norwest VP on Startup M&A + your action plan for 2025

2025 is looking like it’s going to be a big year for startup M&A

Regardless of how you may feel about the totality of the recent election, the near-term implication as it relates to startup M&A is likely positive. If the tailwinds of reduced regulation, lower inflation, favorable interest rates, and aggressive strategic plans materialize you will have the ingredients in place for the key factor in startup M&A: optimism.

Acquiring startups requires faith. Faith that a big, risky, bold, acquisition is going to pay off. It’s hard to have faith when you’re pessimistic. I’ve been doing this a long time, and I can tell you, the best years have been when acquirers are optimistic, with faith that the future is better than the past. In contrast, the worst years have been when acquirers have pulled in their claws, fearing what may be around the corner. As we turn this corner into 2025 things feel promising.

And there’s a secondary booster to this optimism: urgency. The AI revolution is upon us. For many Potential Strategic Partners (“PSPs”) 2024 was a planning year. They were figuring out what AI meant to their company and where they should place their bets. 2025 is looking like an action year. As PSPs see their competitors making AI moves, the pressure for them to act will be tremendous. The AI winners and losers are starting to get sorted, and executive teams aren’t going to want to be stacked with the losers.

Optimism + Urgency = Boomtime

If you’re reading MBP.co then you’re already way ahead of the startup M&A game. But how do you get even more aheader? That’s what we’re going to discuss here, starting with four great posts from Norwest, and ending with your 2025 action plan. I want you to have your priorities set and the ideal steps lined up. 2025 is the year of the PBI (Partner Big Idea). Boomtimes come and go, let’s get the most out of this one while it lasts!

Norwest Venture Partners on startup M&A

Now that the three part series on building the Partner Big Idea is behind us (part 1, part 2, part 3) we can get back to the fun stuff! As I do for Hot Takes I went on the search engines and poked around for posts that appear when you look for startup M&A advice. Norwest has a post that does very well: M&A Strategy Advice for Startup Founders & CEOs (not a huge surprise given the SEO juice that title surely has!). It’s a lengthy piece with lots in it to discuss. At the bottom of the piece are links to three more posts (here, here, and here)! Go big or go home is my motto - so we’re going to expand the aperture of this Hot Take and look at all four posts through the lens of the Magic Box Paradigm.

First a little housekeeping. While the three pieces I discovered at the bottom of the first piece have authors associated with them, this first piece doesn’t (if you’re out there let me know!), so I’m going to refer to the mystery author as “Poster.” Also, these are four dense articles so rather than plod through each of them point-by-point I’m going to pluck out the parts with the greatest alignment, and misalignment, with the MBP - all with an eye towards getting you ready to roll in 2025.

PE vs strategic M&A

The MBP focuses on developing “strategic” M&A opportunities (opportunities with larger operating companies). This isn’t to say that startups shouldn’t consider private equity as a potential path. In her piece Don’t Let Turbulent Markets Stop You from Planning a Smart Exit Strategy Norwest’s Sonya Brown makes a good point that in the current market “there is still a lot of private equity money. As a result some of our exits probably will tap that source of funding, at least in the near term.” I agree, and in recent years I’ve seen an uptick in PE firms acquiring certain types of startups. However, because the thesis for a PE-type acquisitions typically centers on the performance of the startup in-and-of-itself these are often less Magic Box scenarios, and look more like the DCF type M&A deals you learn about in business school. In short, PE acquirers are likely going to take a utilitarian approach to valuation. What we’re looking for are big ideas that lead to big valuations, and those are almost always found in the strategic (operating company) acquirer market.

The centrality of the PBI

The Partner Big Idea is the magic in the box, and the MBP is the method for building them. It’s notable how frequently articles on startup M&A nibble around the edges of the PBI without ever calling it out directly. In the main Norwest piece M&A Strategy Advice for Startup Founders & CEOs the PBI is hinted at, but only gets a passing mention when Poster sites a Bain study that names “clear deal thesis” as the #1 “critical factor to M&A deal success.”

A “clear deal thesis” isn’t just one of several factors, it is the factor. It’s the main event, it’s the show, it’s center court. Building a clear deal thesis isn’t something that just happens, nor is it incidental to factors like valuation or the likelihood of close - it’s what powers everything, it’s the energy source of the entire effort. We’re not going to dive into building the PBI/clear deal thesis as we just covered that in the three part PBI series - but to orient ourselves correctly, all other factors are in service of the PBI, it’s the one ring that rules them all. The elements we’re going to discuss from these posts are the enabling factors to getting you to a PBI, not things that are its substitute, or in some way it’s equal. What we’re looking for are the ingredients and catalysts for building PBIs - and there’s a great deal to uncover in these posts.

Relationships

Relationships are the foundation upon which big ideas are built. In her post titled How to Get Your Company Acquired, Not Sold (a title I love BTW, for more on why I love this title read this MBP post on the pitfalls of the sales process mindset) Priti Youssef Choksi describes how a “over the years, two well known entrepreneurs (acquirer and acquired) had developed a strong rapport and eventually were so aligned on a future together that the actual deal process was very short.” That alignment on the future together is code for the PBI. These two founders had a clear deal thesis, one they had developed over many years, to the point that when it made sense to actually put it to work, getting the deal done was easy.

In the main Norwest piece M&A Strategy Advice for Startup Founders & CEOs Poster speaks at length about Relationships, it’s arguably the central point of the piece. PBIs take time to develop. Sometimes their gestation period is years. It’s important to start developing relationships early, and to get that thinking started.

Trust

Startup M&A is exceedingly risky for PSPs. They’re paying a premium price in the hope of achieving a transformational outcome, at some point in the future. That’s one heck of a leap of faith! The only way they are going to make that leap is if they trust the people they are going to make it with: you and your team. Poster makes some excellent points about building trust through the process itself. For example Poster has a section on not “hiding bad news during the M&A process” - nothing kills trust like a lack of transparency. Going even further Poster talks about founders not “letting ego get in the way.” As it says in the MBP: confidence is inspiring; humility is endearing; arrogance is a deal killer. Trust is subtle, it takes time to develop, and it can be destroyed in the blink of an eye. You need to build an enormous amount of trust if you’re going to pull together an epic startup M&A deal.

The trust point is extended in Gary Walter’s post How to Sell Your Company: 5 Lessons Learned from Doing it Twice. Walter’s point #5: “Be open, honest, and a bit vulnerable” is right on. PSPs are rarely acquiring your startup for what it is today, they are acquiring a work in progress, that is in turn going to fold into their work in progress. It’s all becoming. They want to know they can work with you. They will be looking to understand if you’re collaborative, if there’s a strong culture fit, if yours is the right team to help them tackle unknown future challenges. Walter speaks about his changing posture from his first startup M&A transaction to his second, how by opening up the second time around (and abandoning the projection of perfection) he was able to establish a framework for confident collaboration. It’s more important to create an environment of productive problem solving than it is to show you’ve already solved all the problems.

Engage

There can often be a hesitance from startup leaders to engage with PSPs. The concern is that PSP engagement may send a signal the startup is for sale. The good news is that you can engage without sending that “for sale” signal, you just have to engage in the right way. As I discussed in the MBP post extending on Chapter 3 of the book, the grand unifying word of startup M&A is: impact. You are an innovative team looking to have the biggest impact possible on the world. It may be that that impact is maximized by going it alone, or maybe it’s through a commercial partnership, and it could even be that it’s best achieved by fully joining forces through an acquisition. You’re open to every conversation that relates to your potential impact, and you can start each of those conversations with the prior sentence.

Choksi rightly advises startups to “take the corporate development meeting.” Corp dev’s mandate isn’t just processing near term M&A transactions, they are also responsible for mapping the market and understanding how longer-range priorities could be enhanced by relationships with certain startups. But Choksi takes it one, good, step further. She advises you to leverage these corp dev outreaches “to get connected to product teams and company leadership and have them get to know you.” Bingo! Certainly take the corp dev meeting, but don’t go into the meeting flat footed, do your research and identify the key people at the PSP in product and leadership and leverage the conversation with corp dev into introductions to them.

Choksi even uses the magic word, impact, when says startups should seriously consider joining forces: “if it’s clear that the acquiring company’s resources will help you realize your vision and have a more significant impact.”

Startup M&A is a buy-side driven business

In startup M&A it’s not about when you want to sell, it’s about when buyers want to buy. Startup M&A is about powering a partner’s big idea. It’s about how you fit into, and accelerate, the PSP’s product roadmap. Those spots on the roadmap appear very rarely, and usually for only a moment in time. When the deal door is open, you need to at least take a good look inside.

Poster makes this essential point in the main piece: “don’t ignore offers to sell the company.” However, to align with the MBP, I’m going to adjust this sentence to read “don’t ignore opportunities for your startup to be acquired” - which I actually think is closer to the point Poster is trying to make. Many inbound PSP inquiries will be high level in nature and you’ll quickly realize if it’s more of a “get to know you” type outreach. However, you’ll also quickly realize if it’s more than a casual outreach, and there’s a substantial PBI in the works; if there is, I’d take it seriously. Legitimate PBIs are few and far between. As Brown says, don’t ignore “the importance of timing.”

Scarcity

As we know from the MBP, startup M&A valuation = opportunity / scarcity. With the scarcity denominator often having the biggest impact on the equation. Right in line with this thinking is #3 on Walter’s list of 5 lessons: “Know your differentiation.” Walter astutely says “buyers are looking for assets that are better than the competition or better than themselves. Too often we entrepreneurs are not able to quickly and succinctly articulate how and why we are different from our competition.” In MBP speak this is your ability to articulate your scarcity narrative. I dove deep into articulating scarcity in this MBP.co post on scarcity so I won’t expand on the mechanics here, but the headline point, as confirmed by Walter, is that being able to articulate what makes you different and special is of critical importance.

Being an attractive acquisition target

In the main piece Poster has a lengthy section on the makings of an attractive M&A target. This is where we start to see a deviation from the MBP and it’s good for us to dig in a bit here. Poster is trying to unpack how it is that some startup acquisitions achieve outperforming valuations, in certain cases reaching “revenue multiples as high as 20 times to above 100 times revenue.” Poster attributes these outsized valuations to the “strategic premium the buyer places on the team, the product and technology, and the dynamics in the market.” That’s kinda right, but not exactly in the way Poster goes on to frame it as: “Premium M&A valuations will go to companies with high growth, amazing technology, strong pipeline, highly recurring revenue with annual or multi-year contracts, signals of sales efficiency, gross margins, and low churn.” Poster extends this to the Rule of 40, highlighting that as the valuation-driving equation. Don’t get me wrong, these are all fantastic, and if a startup has all of these attributes then they are surely a very strong company. In fact, in a case where all of these were present, I’d echo Choksi and consider that this may be a time “when not to sell” under almost any circumstances!

The items that Poster lists will most certainly make you more attractive to growth capital investors, but I’d argue that these aren’t the core driver of massively outperforming startup M&A valuations. What drives an outperforming startup M&A valuation is the Partner Big Idea. An idea so big that it consumes the attention of the acquirer, and to which your startup is so critical that they have no other option but to pay a premium to acquire it. The structure of your revenue, the nature of your contracts, even your margin profile and churn, may, or may not, be of critical importance to the PSP. They aren’t paying 100x revenue because they care about your revenue, they are paying a giant price that backs into 100x revenue because they care a lot about something other than your revenue. Big ideas come in all shapes and sizes and what they may be looking to accomplish is almost certainly quite different from the path you’re on today. Said simply, if your conversation with the PSP is centered on how great you are independently, you’re probably on the wrong track. To dig deep into building the Partner Big Ideas that lead to outperforming valuations read the three part series here: part 1, part 2, part 3.

Valuation and negotiation

Then we get to the ultimate point of the whole conversation, determining valuation, and Poster and the MBP again have a bit of divergence. If you’re following the MBP, and you’ve correctly gone through the process of building the PBI, then you’ve established tremendous value in the eyes of the partner. They have so much urgency about the larger strategy that they don’t want to waste time with lowball offers, and there’s a strong enough relationship that there’s significant social pressure for them not to want to burn this important relationship by offending you. You want the PBI to power a strong first offer. You want your valuation to be your portion of their strategy, and not a function of revenue or EBITDA multiples applied to your startup as an independent company.

The MBP and Poster rejoin the same path with the advice to “seldom say your number first.” As I say in the MBP book, when a value is relatively determinable, like when you’re selling a house, then it can make sense to plant a high anchor price to start negotiations. However, since the PBI process is a buildup to an ultimate moment of maximum value, maximum urgency, and maximum pressure - and since you don’t have complete visibility as to how big this opportunity might be perceived to be by the PSP, you are wise to let them speak first so as not to leave anything on the table. And as I say in the book, sometimes you just don’t get there in the first round of discussions, but that typically means the PBI needs more development (as opposed to the buyer having enormous valuation flexibility that they just don’t happen to be sharing in their opening offer).

Four great startup M&A posts from Norwest! Now how do we turn this all into strategy?

2025 is looking like it’s going to be a big year

Here’s the five step plan for getting things rolling in Q1:

December 12, 2024

MBP Discussion on Lenny's Podcast

I stumbled on an exceedingly interesting discussion of the MBP this week!

If you’re on substack generally, and if you’re on this substack in particular, then you’ve heard of Lenny’s Newsletter - one of the biggest substacks of them all. So it goes with out saying that it was great to see the MBP discussed on this platform.

Jonathan Lowenhar founder of Enjoy the Work gives his take on how his team adapts and applies the Magic Box Paradigm in their work with startups. It’s an interesting variation on the themes we discuss on MBP.co. I particularly enjoyed the success stories Lowenhar shares.

A few things I found particularly interesting from the conversation:

Inversion: Lowenhar opens by describing the Magic Box Paradigm as an “inversion” of the orthodoxy and “utterly counter to most of the advice founders have heard.” Yep!

Fantasy: Lowenhar frames the “big idea” as a “fantasy” - what I like about this framing is that it speaks to the criticality of imagination. In the MBP book and on this substack I tend to be very technical in how to spark and construct the partner big idea (“PBI”). What can be lost in approach is the equally important need for passion and creativity in the big idea process: fantasy.

Competition: The MBP speaks a great deal about the role competitive dynamics have in these conversations, and in the forming of big ideas. Lowenhar astutely warns founders to handle competition and competitive dynamics with care (both in terms of sparking urgency, and I would add also in terms of valuation/negotiation). For more on this read the MBP.co post on startup M&A bidding wars.

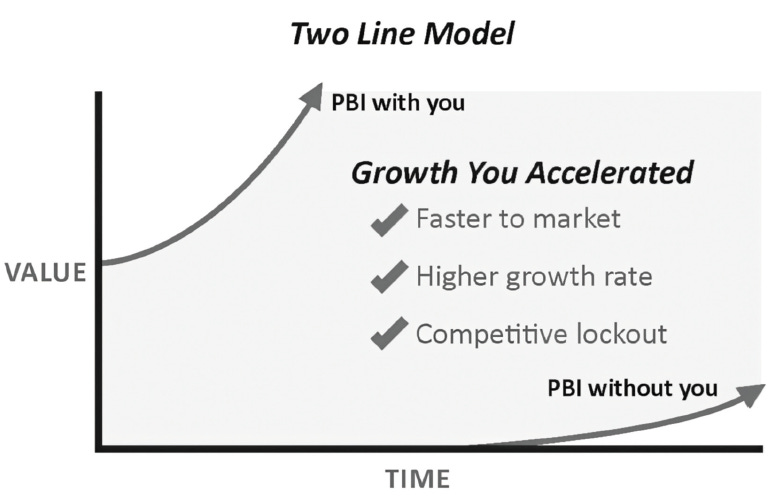

TLM: Lowenhar has a great discussion on shifting the conversation with a potential strategic partner from you as a standalone company, to what you can accomplish together. Essentially the power of the Two Line Model - even if they call you crazy - you still need to put it out there! Shift the framework of the conversation for your math to their math. As I say in the MBP book, your valuation is the present value of your contribution to their future strategy.

Here is a link to the section of the interview where they discuss the MBP (and the rest of the podcast is great also). Minute 25:25 in the full podcast if you jump to the start of the podcast.

If you’re still here, a couple other recent mentions of the MBP that also popped up on my radar:

Mention in Forbes about how the founders of Jemi leveraged the MBP.

#6 on the the list of 8 books every SaaS founder should read.

Lastly, an MBP.co programming note - going to publish a big Hot Take next week where we look at four pieces on startup M&A from a well known venture firm, break them down, and then leverage them to create a 2025 action plan! Stay tuned!

October 9, 2024

Building a Partner Big Idea - Part 3 - Setting up the Right Offer

The MBP centers on the Partner Big Idea (“PBI”). This three part series is a deep dive into their development.

Part 1 is (here): Opportunity + Methodology + Execution

Part 2 (here): Economics + Two Line Model (“TLM”)

Part 3 (here we go): Market Leadership Positioning (“MLP”) + value framework + setting up the right offer

As I said in Parts 1 and 2 this is a fictional scenario. Any overlap with happenings in the real world is coincidental. Also, I’m distilling the development of a startup M&A thesis down to its essence, so I make all kinds of simplifying assumptions and skip over any number of details. What I want to transmit to you is the “feel” of how these things go, so that you have a head start in handling the situations that present themselves to you.

As I’ve said in the prior posts, this is all a “way of thinking.” It’s intended to give you an approach that you will almost certainly adjust in practice. In your case things may be shorter, longer, fatter, or skinnier. It will flex based on what seems achievable and best fits your context. Don’t worry if it doesn’t make sense to do all the parts I describe - I’m trying to give you an example framework, one that you can then improvise with, and hopefully improve upon!

The PBI

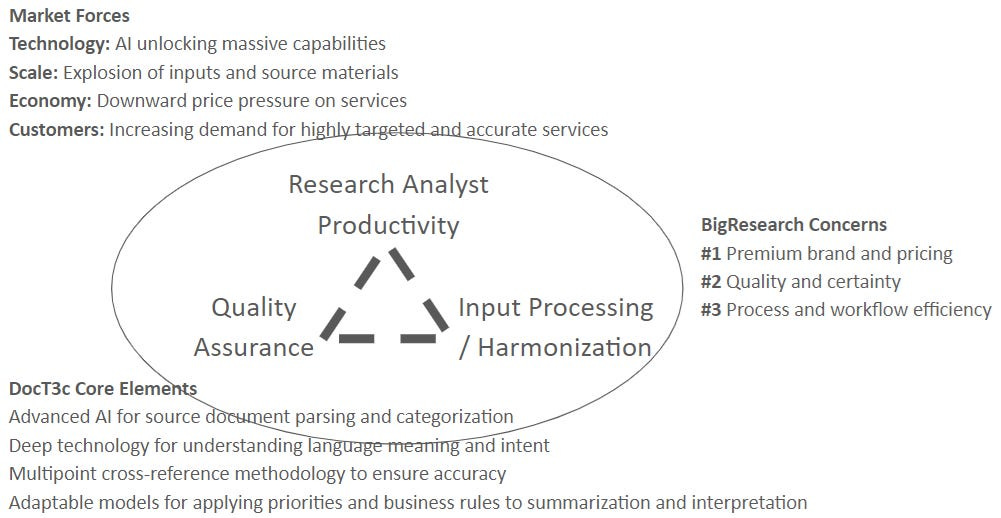

A lot has gone into building this PBI, so it’s important to read the first two parts of this series before diving into this part three! But to get us pointed in the right direction, let’s do a brief recap. BigResearch is a large diversified research company that studies complicated things for giant clients. DocT3c is a startup working on advanced AI for language processing.

Together they’ve developed the framework for a powerful PBI: Aligning key market forces; accounting for BigResearch’s major concerns; and determining how best to leverage DocT3c’s technology and expertise.

DocT3c is catalytic to BigResearch’s unlocking of the power of AI. They’ve mapped out a long-range and far-reaching strategy. In short, they’ve created a lot of purple boxes - with DocT3c’s red box right at the center of them.

DocT3c’s CEO has artfully crafted the Two Line Model (“TLM”) and articulated the enormous impact this PBI will have on BigResearch’s business.

Now it’s time for DocT3c’s CEO to pull this all together and ensure BigResearch fully appreciates how acquiring DocT3c will move them into a dominant market position, thereby significantly increasing shareholder value. By extension he also wants BigResearch to make their maximum offer to acquire DocT3c, an offer that acknowledges the critical role DocT3c will play in their future. In this Part 3 of the PBI series we are going to lay out the moves DocT3c’s CEO needs to make to ensure BigResearch develops that strong offer.

Tight linkage

Through the TLM process DocT3c’s CEO carefully linked DocT3c’s capabilities to the critical variables that power BigResearch’s significantly improved performance in combination. Propelled by the giant head start BigReseach will realize through the acquisition of DocT3c they will expand their TAM, increase the number of projects on which they can bid, improve their win rate, increase revenue per customer and improve the efficiency of project delivery.

Together the teams have developed a robust execution strategy and it’s through that strategy that it has become clear to BigResearch that to make this all work they needed to acquire DocT3c. A partnership or a licensing arrangement just isn’t going to cut it, they needed to own the platform and capture the full attention of the entire team.

Startup M&A is a revelation

Let’s stop and make a highlight on this point. Many startup founders wonder how they can move a conversation with a potential strategic partner (“PSP”) out of the “friendzone” (partnership, or license agreement, or…) and into M&A. The reality is you probably can’t (at least not while maintaining a position of strength). The need for the PSP to acquire your startup is instead “revealed” to the PSP through the development of the PBI. By carefully constructing the Opportunity, Methodology, Execution, and Economics layers of the PBI the strategy will build up the gravitational pull required to consume your startup. It will become clear to the PSP that acquisition is the only way forward. You are working to create a revelation, not pressing to force a decision.

The PBI gains momentum

Startup founders often fret about their inability to get senior executives at target PSPs involved in M&A conversations. They have access to enthusiastic mid-level players, but just can’t seem to break through to the executives with the organizational juice to sponsor an acquisition. The Magic Box Paradigm PBI process offers the solution. A well constructed PBI build’s organizational involvement, and in doing so compels an increasing amount of senior executive input. It builds intellectual mass as the layers of the PBI are formed. By requiring input from across the organization it elevates itself onto the visible horizon of PSP senior executives.

Remember business is a battle of ideas, and there’s lots of good ideas out there. This means the PBI needs to outcompete them all. It has to be the best. So, in a world of competing priorities, it’s not enough to just be visible, you have to be urgent. A well constructed PBI will almost certainly have greater depth and breadth than other potential strategies. And because it includes making an acquisition (vs. the other PSP ideas that probably start from scratch, and will take a while to mature) the return on investment from the PBI will be realized sooner!

You want this sponsorship, urgency, and scale to translate into a strong valuation.

Setting up an outperforming offer

A PSP’s offer to acquire your company should come at the end of the value creation process, not at the start. You want the first offer to be close to the max they would be willing to pay and you want it to incorporate every aspect of the PBI. This PBI is going to move the PSP into the premier market position, it’s going to lift their enterprise value. Making this move is urgent because your startup is a perfect and unique fit. Everything from your technology to your corporate culture align with the PSP. The future is at stake and you are the key that unlocks it.

To the victor go the spoils

DocT3c’s CEO realizes that now is the moment to pull it all together. The PBI is almost fully formed. But what does the PBI really mean to BigResearch?

It means that BigResearch is going to establish the leadership position in the market. They are going to be Coke, not Pepsi, and most certainly not Fanta. DocT3c’s CEO develops the Market Leadership Positioning (“MLP”) that’s going to explain the power of the PBI and how it will catapult BigResearch to #1.

#1 sets the market narrative

DocT3c’s CEO begins to develop the MLP document. He takes the lead in its preparation, but he also wants it to be a collaborative creation so he seeks input from BigResearch’s team wherever he can.

The first thing he frames is the market power accreted to the #1 player. #1 controls the narrative. They have the strongest brand, fastest growth, and biggest technological advantage. #1 controls pricing, attracts talent, and wins the jump balls.

DocT3c’s CEO reaches out to various BigResearch execs to discuss how they view market leadership. He wants to make sure he’s using their vernacular in the articulation of this opportunity. He wants the MLP to speak their language. He also appreciates that this document should lean more qualitative than quantitative - it’s the story of BigResearch’s future.

MLP framework

DocT3c’s CEO opens the MLP with the key drivers shaping the market in which BigResearch operates. He then outlines the growth profile of the market, and includes the additional market categories that the PBI would enable BigResearch to reach. He then goes create a high level, ten year, projection of what portion of this expanded market the #1 player could reasonably expect to capture. He supports this projection by illustrating the case studies from related markets where a dominant market leader was able to establish a #1 position by leveraging next generation technology.

He layers on to this analysis a commentary on how moving fast will enable BigResearch to outmaneuver competitors in winning the top customers. He closes the MLP with a summary of the secondary and tertiary benefits of market leadership. In particular, the market leader’s ability to set industry protocols, establish best practices, define vernacular, and a few other factors that collectively represent the “securing of the high ground” in the category.

The missing link

You want the value the PSP places on your startup to be a function of their improving position (not of your standalone metrics as a small company). Yet, it’s hard to make the leap from the developing PBI all the way to a discussion of PSP value creation. The MLP is the missing link between the creation of the PBI and setup for an outperforming offer. It raises the altitude of the conversation up from the practical business implications to the larger strategic ones. However, there’s one more piece to move on the board to perfectly position yourself. You have to translate the PBI into their improving capital markets position. You need to show the change in the PSP’s future value so as to maximize their current view of yours. Said differently, you want your valuation to be the NPV of your contribution to their strategy, not the DCF of you as a standalone company. As with the linkage of your startup to the critical improvements in the TLM, you want to now link the PBI to their rapidly improving capital markets posture.

BigResearch value drivers

DocT3c’s CEO reviews the companies that market analysts tend to compare to BigResearch. He sees a few consistent patterns in the value drivers that influence how these companies are perceived by the market. He reduces his list of value drivers down to the six that seem to really power capital markets perception in this category: rate of growth, scale of revenue and profit, innovation and technology leadership, strength of brand, market share, and competitive moat.

The basket of comparable companies to BigResearch look like the following:

On its current course BigResearch can make a good argument that they are at least comparable to the average of this basket, putting their enterprise value multiple in the 1.2x revenue range. From the TLM it’s projected that on a standalone basis BigResearch will cross $800M in revenue three years out and with a 1.2x revenue multiple they’ll inch over the $1B enterprise value mark.

Movin’ on up

Now DocT3c’s CEO gets to work on articulating how, through the PBI, BigResearch can massively improve on this performance.

July 29, 2024

Building a Partner Big Idea - Part 2 - The Two Line Model

The MBP centers on the Partner Big Idea (“PBI”). This three part series is a deep dive into their development.

Part 1 (read Part 1 before reading this Part 2): Opportunity + Methodology + Execution

Part 2 (this part): Economics + Two-Line Model (“TLM”)

Part 3: Market Leadership Positioning (“MLP”) + value framework + setting up the right offer

As I said in Part 1 this is a fictional scenario. Any overlap with happenings in the real world is coincidental. Also, I’m going to try to distill the development of a fictional startup M&A thesis down to its essence, so I’ll be making all kinds of simplifying assumptions and skipping over any number of details. What I want to transmit to you is the “feel” of how these things go, so that you have a head start in handling the situations that present themselves to you.

The PBI

As a quick recap of Part 1 we have BigResearch, a large diversified research company that studies complicated things for giant clients. DocT3c, a startup working on advanced AI for language processing.

Together they’ve developed the framework for a powerful PBI: Aligning key market forces; accounting for BigResearch’s major concerns; and defining how best to leverage DocT3c’s technology and expertise.

DocT3c is catalytic to BigResearch’s unlocking of the power of AI. They’ve mapped out a long-range and far-reaching strategy. In short, they’ve created a lot of purple boxes - with DocT3c’s red box right at the center.

Diving in on the Economic layer of the PBI

Beyond the Opportunity layer of the PBI, DocT3c’s CEO has artfully facilitated the initial framing of the Method and Execution layers. What’s left is the final layer of the PBI: Economics.

It’s becoming clear that there are two major areas where these advanced AI capabilities will manifest for BigResearch: 1) increasing the efficiency of project delivery, and 1) acquiring new projects. Both of these areas leverage similar aspects of the underlying product strategy, but they will manifest in slightly different ways. In fact, even though the initial thinking was that improving project delivery efficiency was the highest priority, it’s turning out that the biggest early gains are likely to be made in enhancing BigResearch’s ability to win new projects. As the conversion progresses, and the big idea layers continue to develop, DocT3c’s CEO realizes that it’s time to articulate the underlying economic model for how this PBI will impact BigResearch’s business. It’s time for the TLM.

But before we follow DocT3c CEO's efforts, let’s do a deep dive on what a TLM is and how to approach one.

The Two Line Model (“TLM”)

The TLM is the parallel economic model designed to illuminate the impact the PBI will have on the potential strategic partner’s (“PSP’s”) business. One line of the model shows how the strategy will unfold without the startup. The other line shows how it will unfold when boosted by the startup.

The startup is more adept at leveraging these new technologies. They are also further along in understanding their application. As such the growth curve of the PBI with the startup starts sooner and goes up faster. Without the startup the PSP will have to start later and execute less effectively. Technical expertise, market experience, time-to-market are all critical. So starting later, with clunkier tech, and a weaker team, translates into a tremendous loss of value for the PSP.

Beyond the internal benefits of starting sooner, there are also external benefits. By getting to market first the PSP can claim the market leading position, edging out competitors.

Collect data when it’s easy

You’ll need the inputs in order to build the TLM. Ideally you’d get these inputs directly from the PSP. However, as PBI’s start to form, and excitement starts to build, the potential of a partnership or acquisition negotiation appears on the horizon. The PSP will often become hesitant to share too much info lest that info be used against them in said future negotiation.

Anticipate that you may someday need to build a TLM long before the day comes that you need to do and collect data long before a potential negation is on anyone’s mind.

Naturally the critical data elements may not be exactly clear from the start, and they will be contextual to each PSP/PBI context, but you can almost always make general guesses around the big economic levers of a PSP’s business. A few safe bets for data collections are areas like:

Number and types of customers

Forms of monetization and pricing

Retention and churn dynamics

Sales cycles and conversion rates

Unit economics and core cost drivers

Implementation, and integration requirements

Delivery and support resources

You don’t need to get all of this in one go. As you work your way through early conversations you can almost assuredly smurf up an enormous amount of information by casually asking pointed questions. Arming yourself with this information will not only enhance your understanding of the PSP’s business and priorities, but it will also set you up to build a kickass TLM.

TLM KISS

As the old saying goes “keep it simple, stupid.” My version of this as it relates to startup M&A is that if it doesn’t make sense on a napkin, you probably don’t have a deal. Distill your TLM down to as few moving parts as possible. You don’t want a lot of clutter in the model. Clutter will confuse the conversation and significantly degrade the impact.

Ideal elements are ones that are: 1) core economic drivers of the PSP’s business (or potential business); 2) significantly impacted by the PBI; and 3) linkable to impacts your startup will make. These are the jackpot variables and each input may not hit all three but wherever you can, you’d like them to!

Strive to keep the TLM simple. When you do run into something you feel it’s important to expand upon, do it in a supporting sub-model or analysis document. The TLM is the top level thinking, but it doesn’t have to be the only piece of work. If you need to expand on an input or variable then do so by referencing another piece of work. This will keep the TLM from becoming overcrowded, while also displaying the depth of your thinking.

The TLM should focus on the core elements of the PBI and not extend too far into adjacent arenas. You also don’t want to look too far into future potential opportunities. You can discuss adjacencies and long-range potentials as qualitative elements in supporting materials. As I said above, the TLM is the napkin-math for the core aspects of the PBI.

KISS.

The start of a conversation

There are times when the relationship between the startup and PSP is so collaborative that developing the TLM is a joint exercise. But, more often than not, you’re probably going to be building the first version of the TLM without direct help from the PSP.

You want to build the TLM in such a way that it starts a conversation about the enormous economic impact of this PBI. To accomplish this in the least threatening way possible, you want to design the TLM in such a way that it can be handed to the PSP’s team, and they can play with the inputs. Framing it as a very rough draft, a thinking tool that needs their feedback. They may call you crazy, but the impact of the PBI, and the TLM, will start to seep into their thinking.

It’s also potentially the case that you aren’t able to develop a full blown TLM, the numbers may just be too vague for you to create a quantitative business case. In this circumstance you still want to create some form of framing of the economic implications of the PBI. Even if the framing is broad, there needs to be an articulation of the impact the PBI will have on the PSP, and of your importance to it. Make your case qualitatively if you can’t make it quantitatively, but still make sure to make your case.

Fortunately for DocT3c the inputs are clear, and the CEO has collected what he needs to build the first draft of a compelling model.

The TLM for BigResearch

DocT3c’s CEO has been gathering data points throughout the PBI development process. He’s made a point of trying to discover insights into BigResearch’s view of the market, their sales funnel, and project execution.

With new project acquisition emerging as the top priority (and improving project execution efficiency following closely behind) DocT3c’s CEO begins to frame the TLM for BigResearch.

He has learned that projects are the core of BigResearch’s economic model. They see the typical project as being roughly a year long, with three or so consultants per project, billing around $85K per month (at an average of $200 per hour) - so in the range of about $1M per project per year.

DocT3c’s CEO also learned that BigResearch has around 600 projects running at any given time, which puts them at roughly $600M in annual revenue. BigResearch’s CEO has set the company’s BHAG target to be reaching $1B in revenue in the next five years.

BigResearch sees their current target market as representing 20K strategic research project starts per month. Further, BigResearch believes that by leveraging technology they can expand the types of projects they could serve, in time significantly increase the number of project starts on which they could bid.

Further, through this technology BigResearch can not only increase the number of projects they can serve, and on which they can bid, but they can also improve their win rate, and increase their revenue per project.

As it relates to improving the efficiency of project delivery. BigResearch sees this new technology as: 1) enabling their consultants to do more in less time; 2) enabling less expensive junior consultants to do the work of those at a senior level; and 3) increasing both the speed and quality of delivery.

Where to focus?

DocT3c’s CEO knows that for the TLM to be effective it has to be simple. He decides to focus on a few key growth variables: market size, sales funnel, and revenue expansion. He’s going to include some level of cost improvement on the project delivery side, but for now he’s going to handle this in a more aggregate way and not dive too deep into it.

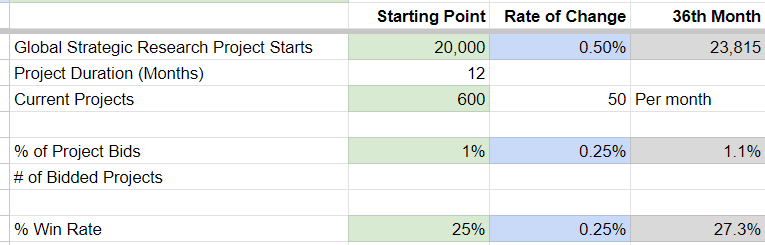

Here are the big numbers he puts down as his starting point on the growth side:

Global Strategic Research Project Starts (Per Month): 20,0000

Percent of Projects BigResearch Bids: 1%

Percent Win Rate on Project Bids: 25%

Project Revenue (Per Month) $85,000

Current BigResearch Projects: 600

Project Length (In Months): 12

DocT3c’s CEO is going to use these numbers as the starting point for both the “Standalone” model and the “Combined” model. There’s no real reason to change these starting points for either model, as the starting point is-what-it-is in both cases.

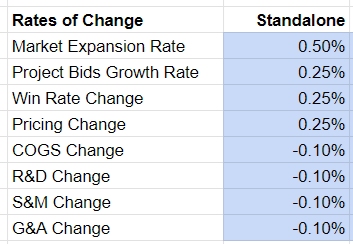

What is going to differ between the two models is how quickly change happens. How fast can BigResearch expand the target market, bid on more projects, increase their win rate, and expand project revenue? The growth is going to be in the compounding impact of faster, technology-powered, improvement, not in a single step-function leap forward.

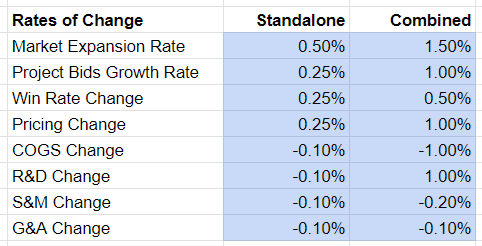

DocT3c’s CEO develops some estimates that he feels are pretty defensible for how BigResearch will evolve in their current standalone mode. For each of the key variables, the monthly rate of change looks like this:

However, by moving quickly, acquiring DocT3c, and executing on the PBI, the rates of change for several key variables change at much faster monthly rate - more like this:

DocT3c’s CEO knows that he needs to tie each of these improvements back to tangible impacts his startup can make. So he creates a supporting document that outlines the impact the PBI (powered by DocT3c’s technology and expertise) will have on each variable. For example in the case of Project Bids Growth Rate he links the AI automation of bid research and preparation to an increase in productivity (and quality). He quantifies the time difference between the legacy, manual, way of developing bids and the new automated approach. It’s a strong link and the process improvements are hard to argue.

Putting this to work

DocT3c’s CEO builds out a simple model. The model looks out three years (by month) and has the Starting Point of key variables (column B), the Rate of Change (column C), and then how things look for that variable in the 36th Month of the model (column D).

(Spreadsheet note: if you download this spreadsheet you can edit various cells. On the Monthly tabs the cells that are shaded green are editable. The cells that are shaded blue are editable also, but edit them on the Summary tab (column L and M). I have these blue cells organized on the Summary tab so that you can quickly compare changes in the key variables at the aggregate level.)

You can see the full TLM model here:

July 4, 2024

Happy 4th - Free MBP Giveaway

For the holiday weekend we’ve unlocked the Kindle App version of the Magic Box Paradigm book for free download.

Spread the word.

Grab a copy here.

Happy 4th!

May 29, 2024

Building a Partner Big Idea - Part 1

If you haven’t already - get the second edition of the MBP here.

The MBP centers on the Partner Big Idea (“PBI”) so it’s time to do a deep dive into how to approach building one. This is a big topic, so I’m breaking it into a three part series. Here’s how it’s going to flow:

Part 1 (this part): Opportunity + Methodology + Execution

Part 2: Economics + Two Line Model (“TLM”)

Part 3: Market Leadership Positioning (“MLP”) + value framework + setting up the right offer

I’m going to try to distill the development of a fictional startup M&A thesis down to its essence, so I’ll be making all kinds of simplifying assumptions and skipping over any number of details. What I want to transmit to you is the “feel” of how these things go, so that you have a head start in handling the situations that present themselves to you.

The scenario we’re going to develop is completely fictional. It’s all made up and any overlap with happenings in the real world is coincidental.

Purple boxes, mapping big ideas

The purple boxes framework has become quite popular!

The funny thing is that it’s not even in the MBP book itself - but is instead a construct that’s come to be on MBP.co (although I’m plotting a third edition of the book that brings it into the MBP proper).

As a reminder on the purple boxes framework:

The PBI landscape is framed by the major forces creating significant opportunities in the market. Inside of this frame is your startup (the red box) and the potential strategic partner (“PSP” - the blue boxes).

It’s very easy to focus these conversations on the red and blue boxes, they have shape, they are bright, they jump out at you.

However the gold is in all the white boxes. There’s only 7 shaded boxes, but there are 93 white ones!

The big idea is the area of the new strategy. It’s a blend of blue and red: purple. It’s a bold new initiative, with your startup at the center of it.

It’s not about you today, it’s about what you unlock tomorrow

First off, remember the “P” in PBI is “partner.” This isn’t your big idea, this is their big idea (that you’re helping to shape and enhance). The entirety of your efforts today might be perfectly aligned with the PBI, or it might be that only elements of your startup fit into the PBI (in reality it’s more often the latter). What matters is that there’s a large purple area, and that your startup (in whatever form it takes) is critical to unlocking it. Ultimately you want your value tied to the future value of the purple boxes, not the NPV of the red one.

Let’s build a PBI

BigResearch, a giant, diversified, research firm is starting to see how AI will transform its industry. They are evaluating a number of potential internal development initiatives, as well as exploring potential acquisitions. These are going to be big bets, so they are proceeding carefully. Through a mutual connection they are introduced to DocT3c.

DocT3c is developing advanced AI in the natural language processing (“NLP”) arena. They have a strong team that’s a blend of industry pros and leading academics. They’ve raised $25M and are excited about the opportunities in their field. They started DocT3c to press forward into innovative areas of interest, but they aren’t opposed to joining forces with another market player if that will enable them to maximize their impact and enable them to work on increasingly cool stuff.

DocT3c’s current offering is advanced document summarization and interpretation provided directly to end users. They chose to go after the real estate market as they felt it was ripe for this kind of automation and the cost to acquire customers was relatively low (when compared to other sectors they were considering).

This is what DocT3c’s website looks like:

BigResearch tackles complex research projects for large enterprise customers. This is what their website looks like:

BigResearch’s top markets are:

Legal

Healthcare

Government

Finance

Education

Real estate isn’t even in the top 10.

BigResearch’s has some significant concerns as it relates to AI initiatives (and the use of technology more generally in their services). They have to make sure nothing they do upsets their on-going business. They are OK moving carefully, even if it means moving a bit more slowly. Their primary concerns are:

Maintaining their premium brand and pricing

Ensuring quality and certainty

Maintaining process efficiency (there’s no room for retooling or down time)

Starting the conversation the right way

After a very pleasant introductory phone call with the head of strategy at BigResearch, DocT3c’s CEO realizes a few things about BigResearch: first: they have zero interest in the real estate market; second: they are nowhere close to being ready to deploy an advanced summarization and insight generation solution directly to their clients; and third: the stuff that BigResearch actually wants to do is super easy and would be absolute layup for the DocT3c team - in fact the guts of DocT3c’s platform already does important parts of what BigResearch is looking to do.

There’s a giant opportunity here. An opportunity to revolutionize an industry filled with dinosaurs. But how to approach this conversion? The CEO realizes that if he goes into their next meeting with a discussion of real estate, direct to consumer, subscription revenue, conversion rates, and all the things his investors love, he’s going to take things in the completely wrong direction.

He doesn’t know much about M&A, but he knows there has to be a way to solve this problem. Fortunately another founder friend of his recommends he read this under-the-radar book, Magic Box Paradigm. She says it’ll get him oriented the right way to create a powerful PBI, whatever that is.

M&A hadn’t been top of mind, but it also hadn’t been completely out of mind. This is a massive opportunity and way to put DocT3c’s team on a much larger stage. If it isn’t M&A, there’s also a chance that this could turn into a giant commercial contract, or even an investment. The juice is worth the squeeze to see if there’s something actionable with BigResearch.

Market forces and PSP priorities

Job one is understanding the major market forces shaping BigResearch’s strategic thinking, and then inside of those market forces to get a better understanding of what they see as their current priorities. He sets up a call with the BigResearch execs. He knows they’ll expect to learn about him on the call, and won’t just open right up about themselves out of the gate. So he prepares a short presentation on the areas of focus for the DocT3c team, these are:

Advanced AI for high volume source document parsing and categorization

Deep technology for understanding language meaning and intent

Multipoint cross-reference to ensure accuracy

Models for applying priorities and business rules to document summarization and interpretation

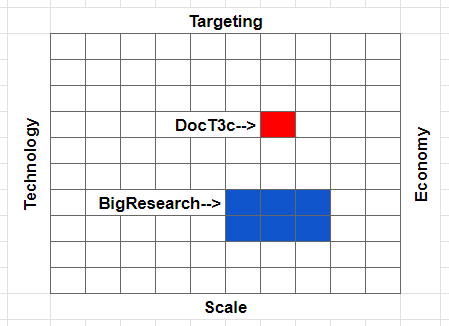

As hoped, the BigResearch exec’s get excited by what they are hearing. And start to share their view of the world and what they see as their top priorities. The major market forces they see shaping the next generation of services are:

Technology: AI is unlocking almost magical new capabilities

Scale: there’s an explosion of new inputs and sources

Economy: many of their clients are victims of disruption themselves - bringing downward price pressure

Targeting: demand is changing and moving from large and broad projects to smaller highly targeted ones

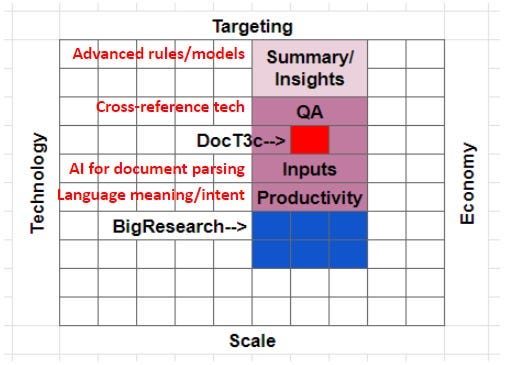

The PBI landscape looks like this:

In response to these market forces BigResearch articulates a set of key priorities:

Input processing and harmonization (in particular deduplication of sources)

Tools for increasing research analyst productivity

Quality assurance (in particular fact checking)

Next generation summarization and advanced insight creation

#4 is what DocT3c does today, but it’s clear that BigResearch isn’t ready to roll this kind of offering out to its clients. And in all honesty, DocT3c’s offering is still pretty early. The CEO knows they had to make numerous tweaks for it to work in the real estate market specifically, tweaks that in some ways made it actually less well suited to other markets more generally. The good news is that priories #1 and #3 are core elements of DocT3c’s platform, and priority #2 is so broad that there are any number of ways DocT3c could help BigResearch there.

Opportunity then Methodology then Execution then Economics

The foundation of the PBI is a shared view of the Opportunity. BigResearch wants to establish itself as the first tech-enabled, enterprise-focused, research firm. They want to infuse their services with AI to enhance productivity, quality, and scale. In doing so they believe they can expand the market while establishing themselves as the preeminent player in the arena. By extension they want to enhance their position in the capital markets by articulating a narrative featuring technical innovation and a high-value, long-range, offering strategy.

As the conversation between BigResearch and DocT3c develops BigReasearch’s priorities come into clearer focus - with the creation of tools to increase research productivity becoming the overarching objective, supported by input processing and harmonization, and ultimately quality assurance. Next generation summarization and advanced insight is very exciting to BigResearch, but they see that as a future capability, something to put on the long-range product roadmap.

The Opportunity is to establish BigResearch as the first tech-enabled, enterprise-focused, research firm. The elements of the strategy looks like:

This Opportunity thesis aligns with the market forces BigResearch has articulated. It also accounts for their primary concerns. It also aligns BigResearch’s current business model and with DocT3c’s core technology

It’s starting to look like the makings of a solid PBI.

Let’s translate this to our purple boxes framework and then dive into Methodology and Execution. Overlaying this all on to the purple boxes framework we we get something like (not a precise rendering - but a tool for thinking purposes):