Will Herman's Blog

December 19, 2020

The Startup Playbook 3rd Edition is Available Now!

The Startup Playbook is the Amazon best-selling startup book that’s been so popular we’ve just released its 3rd edition. Find out why thousands of successful entrepreneurs have used The Startup Playbook as their go-to resource to help build their new startups.

We call this The Entrepreneurial, 3rd Edition because we’ve circled back to the foundation of the 1st edition. Thousands of people used the 1st edition to help them start to build their new companies. The book was popular enough to attract the attention of a major publisher, who we worked with on the 2nd edition. It too was a big success with thousands more books delivered to new entrepreneurs. Unfortunately, we found we had different goals. The publisher wanted to maximize revenue and we wanted to maximize availability. So, we’ve parted ways and released a new version with the goal of reaching more people.

What does that mean? Basically, we’ve republished the book with some new, added content and are making the ebook available now for just $0.99. Yeah, way less than a cup of coffee. It’s also a great, last minute Holiday gift for that entrepreneur in your life. Delivered instantly to their mailbox.

We still offer a free chapter to check the book out (available here). And the audiobook for the 2nd edition – which, all modesty aside, is really very entertaining – is available here.

We’d really appreciate your help in getting the word out. Here’s a quick tweet you can use. And thanks in advance!

The Startup Playbook, 3rd edition is available now! The Amazon Best-Selling Startup book that has been used by thousands of new entrepreneurs to build their startups is available now for only $0.99. Check it out here. #startupplaybook

The post The Startup Playbook 3rd Edition is Available Now! appeared first on The Startup Playbook.

November 29, 2020

Guest Post: How to Ensure Employee Wellness in Your Startup

Image Credit: Unsplash

Image Credit: UnsplashThe annual cost of employee sickness and injury in the U.S. has reached as high as $225.8 billion — that’s $1,685 per employee. And with depression causing employees to lose an average of 27 workdays per year, it’s clear how crucial it is to promote overall wellness in the workplace.

Indeed, employee wellness is essential to business and organizational success. It impacts a company’s culture, resources, productivity, and ultimately, its bottom line. So, how employees are feeling physically and mentally is more than an HR issue. It is, in fact, a fundamental foundation for business growth, stability, strength, and sustainability.

If you still don’t have an employee wellness program, you should consider introducing one. Even the Harvard Medical School attests to how effective employee wellness programs are. And it’s certainly possible to have one without going over budget. With so much at stake in terms of increased productivity and reduced absenteeism, you can’t afford not to.

Listen to your Employees

Although it’s common to quickly think of on-site gyms or fancy catering services when considering employee wellness programs, Pain Free Working highlights the first important step you need to take: listen to your employees. Different surveys have found that it’s not the fancy perks that keep employees happy. Of course, these can certainly attract new hires, but what keeps employees happy in the long run tend to be a little less complicated: better lighting and air quality, the freedom to personalize their workspaces, and attention to mental wellbeing. Starting with listening helps you understand their current mindset, obstacles, beliefs, and provides an excellent foundation and direction for everyone’s wellness.

Define your Metrics of Success

Monitoring numbers of sick leaves in proportion to productivity rates may be the standard way to measure success, but that’s usually not enough. Include monitoring participation rates in the various activities of the program you’re planning. Add conducting anonymous surveys that will measure employee satisfaction. You may also want to make your program meaningful by, say, donating to a charity for every specific number of steps the company takes as a whole.

Communicate Your Plan

It’s important to think about how you’ll motivate and communicate your wellness plan to your employees. Providing discounts to nearby gyms for fitness memberships is a good start. But your program will be more effective and have a stronger impact if you combine education, accountability, and community, with physical activity.

Consider bringing in health and fitness experts who can give workshops on nutrition, exercising, sleep, and other wellness topics. You can also hire a consultant and have a private social media group for accountability and community.

Make the Program Accessible

The level of difficulty in participating should be straightforward and easy. Make sure the program is accessible for everyone. Creating different levels for both beginners and savvy fitness enthusiasts is a good way to make more employees involved and engaged.

Cultivate a Culture of Wellness

A wellness program isn’t just an email cascade informing employees that smoking is harmful, and that they should exercise. It should be a culture. Rajat Bhargava previously highlighted the different roles of a founder. And in the role of the cultural leader, the founder sets the cultural tone for the organization. The employees of a company will do as the founder does, so it’s important to set a unified tone from the top down.

Make a commitment to integrate the wellness factor into every act and decision the company makes — from the backing of the leaders, down to the smallest ways of making the working environment healthier. Start by looking at your vending machine and cafeteria options, or swapping the office snack bowl with healthier alternatives such as nuts and fruits. WebMD has more tips for health improvement in the workplace that you can start with.

Introducing a wellness program for your organization doesn’t have to be complicated. Just start small and keep improving as you go along. Health is indeed wealth, for both employee and company.

The post Guest Post: How to Ensure Employee Wellness in Your Startup appeared first on The Startup Playbook.

September 14, 2020

The Startup Playbook Audio Edition is Available!

One of the biggest requests readers and potential readers of The Startup Playbook asked for in the second edition was an audio version of the book. It’s now available! You can check out The Startup Playbook audio edition on Amazon and Audible now.

Everyone can now learn how to start a company in a handful of easy listening hours. Pair it up with an ebook version to highlight the important points to come back to again and again.

With the average commute these days lasting about 40 seconds – from the coffee pot to the stand-up desk in the living room – it might take a long time to listen to on your daily commute. But, it’s perfect for that long drive to visit your parents. Just sayin’.

The post The Startup Playbook Audio Edition is Available! appeared first on The Startup Playbook.

August 19, 2020

Guest Post: 9 Lucky Tips Every Successful Entrepreneur Needs to Know

Success in business is not a universal metric. It can be achieved in dollars, but it can also be developed in things like jobs created, rising in position, and other things. The point is that success is whatever you want it to be in the business world.

But there are some things that successful entrepreneurs need to know to help make them successful. Some will work better than others, but these are things that proven successes have implemented into their lives in a positive way. Here are 9 lucky tips that every successful entrepreneur needs to know to boost their career.

Self-Care

While being driven to succeed in business is important, so is ensuring that you have the energy to do so. Caring for oneself is just as essential as any other tip. Whether that means eating better – things like chia seeds or herbal teas – or picking up an inflatable hot tub with hydro real jets, is up to you. Take some stress off by hanging out with a pet.

Whatever method that you choose, it is about ensuring that your body has the energy and care that it needs to handle a high-paced business atmosphere. Besides, any of those make for a relaxing end to even the most hectic of days.

Have a Business Plan

No matter what the business endeavor, planning ahead is a key to success. While it is impossible to predict everything that will happen, a business plan can help to mitigate some of the surprises that a venture will bring.

Moreover, preparing can help to make you mentally better-equipped to handle things when they do go wrong. It might not feel great to have those situations presented, but they can become far more manageable when there are some traps that spring up. Remove the surprise and you will be more prepared to handle the good and the bad.

Prepare for Money Challenges

Very few business ventures get off the ground without financial difficulty. This can be finding money to get the project started, capital to finance a new building, or any number of issues that may spring up. The point is that they will happen.

Knowing this, it is extremely important to be wary of debts. Debt can and will kill many small businesses that don’t straddle the line effectively. Watch what you owe because it could be too much to recover from, even if your business plan is sound and you think you have everything covered.

Ask for Help

While it may seem like the most successful people in life did it all on their own, that isn’t the case. As a matter of fact, some of the most successful people in life got there because they had a great support system. This could be a handful of people or an entire company. The point is that help was there.

Failure to delegate and share the load leads to the end of far too many ventures. Don’t be afraid to ask for help when the load is too heavy or where you may not have the expertise.

Remember: It’s Your Wallet

When starting a business venture, it might seem smart to get an expensive office, equipment, or a ton of marketing. But remember that your company’s livelihood is entirely dependent (at least early on) on your wallet.

So, while it is important to make sure that money is spent on the necessary equipment, it is also important to be smart and frugal. Overspending is one of the quickest ways to kill a business venture before it can ever really get off the ground. Spend wisely, especially in the early stages.

SEO is Your Friend

While marketing is essential no matter what the business, it can be done in a variety of ways. Simply put your business needs exposure to your desired audience and that can’t be done without some form of marketing.

Focusing on SEO can be a great way to successfully market without having to break your budget to do so. It will keep you in the mix on major search engines and it can cost little to nothing depending on what you choose to use. Free marketing is great no matter what size the company may be.

Work on Time Management

Far too many entrepreneurs think that working 24/7 is the way to a successful venture. But the fact of the matter is that it doesn’t matter how long you spend doing something, only that it gets done. So, having proper time management abilities can make life easier, especially with startups.

Instead of feeling like you have to miss time with friends and loved ones, try to manage your time more effectively. Work on the important things and ensuring that they are done in a timely manner is of the utmost importance. This is where delegating can particularly helpful, too.

Build a Team

Delegating means having a team that you can lean on. Trusting others, especially when it comes to a venture that you have put time and money into, can be difficult. But it is the only way that a business can truly succeed.

Building a team that you can rely and depend on can give you the peace of mind that you need to focus on your strengths. It also means that you will spend less time on areas of the venture where you will have the least amount of impact.

Always be Learning

The one trait that defines a successful entrepreneur is that they are striving for more. They understand that their knowledge base is never complete and that it takes a constant education to stay on top of trends in that field.

Businesses that are able to adapt to new trends, continue to grow and learn are the ones that often times stay ahead of the curve. The best entrepreneurs never stop learning and are constantly looking for ways to improve not only the business, but themselves. This will transfer to others in the organization and create a truly successful venture.

Article By: Peter Rossi, a professional hot tub designer and founder of ByRossi.

The post Guest Post: 9 Lucky Tips Every Successful Entrepreneur Needs to Know appeared first on The Startup Playbook.

August 13, 2020

The Small Country Startup Challenge

The overall European startup ecosystem is strong and healthy. It has grown significantly in capital over the last decade and acts more like its American cousin than it did in the past. Aside, of course, from the capital gains tax laws in many countries, but more on that at another time.

In fact, one part of the European startup ecosystem that looks increasingly more like the American one is how regional it is. Like its US counterpart, the vast majority of investment capital is focused on a few locations. In Europe, they are primarily, London, Paris and Berlin. Unfortunately, investors and investments in smaller European countries are few and far between. Great teams and solid ideas in smaller countries often go ignored or don’t get the level of investment they need.

This is a shame because many people from smaller countries are hugely entrepreneurial and work harder to find ingenious solutions to underfunding that are often ignored by entrepreneurs in the epicenters of European startup capital. Still, in a world where speed is critically important to success, being good at managing costs is usually not enough to beat better-funded competition. Having fuel to burn – money, that is – makes competing that much easier and makes the odds of success much better.

Know All Your Options

So, what’s a startup team outside of one of the big European investment areas to do? Well, seeking capital from the big investors outside of their country shouldn’t be ignored. Big ideas in solid markets and successful teams can still get still get funding through the regional route. But alternate funding methods are available. Here are a few:

Check out AngelList for European focused investorsTap into a network of investors using LinkedInAttend one of the many European AcceleratorsAttend one of the increasingly available worldwide virtual acceleratorsSubmit your deck to a European-focused worldwide investor syndicatePack your bags and move to one of the regional epicenters in Europe or the US

Without a doubt, it’s more difficult to get funding for a startup in a smaller European country. To get the money you need – and you probably need the money to make it big – you’ll need to apply all of your entrepreneurial skills to fundraising, not just building your product. Use some of these resources to get the ball rolling. Even if you’re not successfully closing money through one of these channels, you’ll build a network while working through channels. In the end, this network will be the key to finding capital.

Accelerators are your best leverage

Building a broad network on your own can be done, but it’s much easier to leverage resources already in place. Accelerators offer incredible opportunities for you to engage with people who you would otherwise not have access to. And, because each of the already established people you meet through an accelerator has an existing network, you can gain access to many others who might resonate with your idea, offer to help or even invest.

And now there are more opportunities with accelerators than ever. The COVID-19 pandemic has changed the structure of most accelerators and moved them virtual. Now, you have access to once regional accelerators from anywhere there’s an Internet connection. Apply to a Y-Combinator accelerator in Silicon Valley, a Techstars accelerator in Boulder, Colorado, or any other accelerator anywhere in the world. You now have access to almost all of them.

If you’re dealing with the small country startup challenge, don’t be shy. Apply to many. You’ll learn a lot and, more importantly, expand your network exponentially.

Ready to build your first company? Learn how to do it with my book, The Startup Playbook co-authored with Rajat Bhargava. Super easy to read and chock full of startup wisdom. Written by founders for founders. Check it out.

The post The Small Country Startup Challenge appeared first on The Startup Playbook.

August 10, 2020

What is this Product-Market Fit Thing Everyone Talks About?

If you’ve looked for capital for your startup, you’ve almost assuredly been asked about product-market fit. It’s a gateway for most investors in determining if your venture is worth their investment. Why is it so important? While hardly a guarantee, it’s a fundamental point in the process of converting your idea into a successful product and testing whether it has a chance to grow into a business.

So, what exactly is it? Product-market fit is the extent to which a good market (many potential customers) is addressed with a product that meets that market’s needs, wants, or desires. It’s proof that both the problem and the solution have value to people.

And by value, it’s the actual monetary value that’s important. Will customers pay for your solution to their problem? That is the ultimate test for product-market fit. Will enough potential customers buy the solution you’re offering?

One of the most high-profile lessons in product-market fit, or lack thereof, is Pets.com. Pets.com was created to sell pet food and accessories via the web, cutting out the middleman and aggressively cutting prices. Sounds like a winning strategy, right? Well, not so much at the time. As it turns out, while Pets.com assumed people wanted such a service, the market just wasn’t ready for it. They had the product, but not a market interested in paying for it. No product-market fit. The company burned through over $300M in about two years and went public before it crashed. It just doesn’t matter how innovative your solution is; if there’s no market, you won’t succeed.

How to Test Product-Market Fit

The best way to test your product-market fit is to talk to actual, potential customers – real people who are part of your target audience. Testing your concept like this takes guts, but it’s the only way to learn whether you’re on the right path with the right idea. Use your connections to gain access to people and offer to discount the product, give them early access to it, or provide a similar benefit in exchange for their time. When you’re not delivering a heavy sales pitch, people are often very open to sharing their time and frank opinions.

You’ll want to discuss as much about the product as possible, even parts that you haven’t thought a lot about yourself. You don’t know what you don’t know, after all, so getting the most feedback you can from others is critical to testing your offering. Remember that testing whether they’ll pay money, in the amount you want, for the solution you’re offering them, is a critical question.

Show Me the Money

The answer to the “How much would you pay for our solution?” question will tell you a lot about your product-market fit assumptions. The price the customers give you will almost never stand up once you’re ready to sell the product, but you should be able to test whether you’re in the right ballpark. For example, you might say to a target customer, “If the price was $150, would you buy this product, which I’ll deliver by May 6?” For some customers, you should even go further and ask who else in their company (if a B2B product) will have to agree to the purchase.

This is a tactic that many successful startups have used, especially when it’s early in the process of vetting if their idea is going to pass the critical product-market fit milestone. By asking an excited customer about their willingness to purchase on the spot, you’ll learn if there’s legitimate interest in your idea and a desire to pay for it. A customer’s readiness to move forward with purchasing your product sends a strong signal that you may have hit upon an idea you can build a business around. Even if they’re reluctant, their reasons for not moving forward may be even more valuable than their early purchase. It’s a great way to learn.

Sometimes, a potential customer who has otherwise been excited about your solution may balk when the discussion of money comes up. Often, there’s a gap between a person saying they like an idea, and their willingness to pay for it by a set date. If this happens, test other price points and delivery dates to see how their reaction changes. Remember to remain completely open to the concept that you may have an interesting idea, but not one that is worthy of the price you need to charge to be successful.

Many people will tell you that product-market fit is binary. You either have 100 percent fit or you don’t. It actually doesn’t work that way. Especially as you’re making your first pass through refining your business model, it’s likely you’ll find some fit, but it won’t be complete. You may find that the group of potential customers that you add value to is small, or the problem you’re addressing isn’t big enough. This is completely normal, and a good reason that you should test for product-market fit as early in your business model development as you can. Testing early gives you plenty of time to fix any issues.

Conform to Your Target Market Rather than Trying to Change It

Markets are hard to change for any company and, as a startup, almost impossible. Obviously, products are easy to change before you actually build them. Rethink your value proposition to see if your target customer will be more likely to buy a different product. Then, go out and test it again with real people. It’s part of the iterative process you should be using to build your business in the first place, after all.

You should also consider the market you’re targeting. Although attempting to change a market in a missionary fashion is close to impossible for an early startup, your idea might have more success in a different market completely.

Remember to be as critical as possible early on. It’s much easier to change things early than doing it later. Keep in mind that product-market fit will also be one of the first things that investors look for. The more prepared you are to answer their questions and provide proof of solid product-market fit, the better off you’ll be during the fundraising process.

As I said, you don’t need to prove that there will be 100 percent adoption to move forward. There are still many steps in the process of vetting your business model. You might find that you can further refine your vision as you go through them to increase your product-market fit. You don’t even need to find 100 percent adoption to ultimately exit the whole vetting process, either. As you grow and have additional resources (including funding), you’ll be able to shape your product and message to address larger groups of customers. Still, you should establish a large enough group of potential customers early on through iterating on your vision and value proposition to be able to convince yourself and others that there is a real market for what you’re creating.

The earlier you establish product-market fit, the easier everything else will go for you and your founding team. Yes, you’ll do a lot of work upfront to make sure you’ve got it, but you’ll save yourself even more time and energy later because you established it early. You’ll iterate less and the changes you need to make will happen when you have the time to do them. If you need to revise your idea or even pivot, you’ll be doing it with less overhead and when you’ll need to implement fewer changes. Ultimately, once you’ve established product-market fit, you’ll be able to raise money faster and at a higher valuation. Wouldn’t that be nice?

Ready to build your first company? Learn how to do it with my book, The Startup Playbook co-authored with Rajat Bhargava. Super easy to read and chock full of startup wisdom. Written by founders for founders. Check it out.

The post What is this Product-Market Fit Thing Everyone Talks About? appeared first on The Startup Playbook.

August 1, 2020

Don’t Hire Your Friends – The Secrets to Building a Great Founding Team

The quality of the founding team is probably more correlated with the success of a startup than the idea the company is founded on. Yet, few entrepreneurs are as diligent in building their founding team as they are in even finding office space. Often, founding teams are assembled from a convenient and available group of friends or coworkers. That is, of course, when there is a team at all. Entrepreneurs frequently set out on their own, taking on the incredibly difficult task of building a startup without any else’s help or support.

Let’s face it, 9 out of 10 startups fail. Don’t you want to do everything possible to increase your odds of success? It makes sense to start off with a solid founding team, right?

With a great founding team, you increase your odds of getting funding, getting into an accelerator, recruiting people to help you out, solving problems more quickly and efficiently and balancing the load. So, why is the creation of a great founding team so often overlooked?

Everyone is in a hurry to get startedThe makeup of the founding team just doesn’t seem that importantIt’s difficult

Typically, what happens in a startup is that someone has the flash of an idea and decides to start a company. Instead of taking the time to look at skill sets and personality matches, they choose people to join them who are most convenient - usually friends or co-workers. I often see new founders act impulsively as they rope in someone with specific skills to address an immediate need as the company is just starting out, or someone who other people suggest they need without really thinking about the future of the company or its long-term requirements.

As you can imagine, these situations rarely turn out well. Occasionally, you might get lucky, but most often, they lead to the most difficult problems you can have in a startup. Issues with the founding team are divisive, unproductive, and are an external red flag for everyone involved in or with the company - especially investors.

Fortunately, most of these problems are avoidable if you understand the importance of the team aspect of the founders and you take the time to think through and be diligent about the process. Let’s start by looking at the most important criteria in choosing a co-founder - personal alignment.

Personal Alignment

Choosing the right co-founders to build your startup is as much about finding the right personality match as it is about talents and skill sets. The relationship between co-founders is one of the special relationships you’ll have in your life. It can (and likely will) also be one of the most difficult. It’s a high stress relationship. The intense pressure of starting a new venture and then building momentum takes a toll on these relationships. Unfortunately, many, if not most, don’t survive.

At the core of the co-founder relationship, there must be mutual trust and respect among all parties. What level of trust are we talking about here? Virtually the highest level of trust. One in which you can share your dreams and aspirations without fear. Yeah, you-have-my-back-in-a-foxhole kind of trust.

When you trust one another, then you can safely disagree and have open conversations. You’ll need this as you debate the best course of action, timing, and a million other details that go into creating and launching a product and the actual company.

Truthfully, few relationships can withstand this level of intensity and commitment. As you look at possible co-founders, ask yourself if you’ll be able to disagree with them without taking things personally. Ask yourself if you can put aside yesterday’s argument to move it forward today. Ask yourself if you can put aside your anger or frustration with a co-founder to appear united in front of the startup team, your early core team, including founders, employees, and your extended advisors and board members.

Only after you conclude that you can establish and thrive in such a difficult relationship, you’ll want to carefully assess your ability and those of your co-founders to play the key roles that founders need to play

Filling Key Roles

Ideally, your co-founding team should fill in your weaknesses or the areas you’re not interested in performing so that, together, you create a solid foundation to grow the company. For example, perhaps you don’t love to be in front of people evangelizing the vision of the business. It doesn’t have to be you. It can be another member of the founding team. Or, say, for example, you aren’t a great manager of people, but you’re an outstanding individual contributor. The structure of the founding team should account for that. All the roles of the founding team need to be filled, but it’s not required that each of the founders can do all of them.

As part of this, you need to be brutally honest about your strengths and weaknesses. You can’t fill in your holes and augment your skillset if you don’t admit where you have weaknesses. We all have them. Your goal should be to find co-founders who are good at the things you are not - technically, procedurally or emotionally.

As you can tell, finding a co-founder for your startup is one of the most important decisions you’ll make when it comes to your startup. This is one of the few decisions that can truly make or break your new company; that’s how important it is. Finding the right co-founders can accelerate your startup enormously. You’ll figure out vexing problems quicker, you’ll get more work done, and you’ll feed off the energy and alignment that you each have.

My advice to you when trying to build your founding team is to slow down and choose wisely. You can avoid having to navigate through an unfortunate situation where you chose the wrong co-founder quickly just by stepping back, casting a large net, and taking your time to thoughtfully consider (i) what you and the company need in a co-founder, (ii) whether you want and can closely work with that person on a daily basis, and even (iii)where that person is located geographically (even if working virtually most of the time, location still has an impact).

Finding the People

So, how do you find the perfect people to fill out your team? When looking for co-founders, start with current or previous co-workers and colleagues. Talk to mentors. Ask your friends. Consider the industry your company will be engaged in and attend meetup groups (events where people with common interests get together and share ideas) in your area, or check out conventions and conferences - even virtual ones. Join industry associations, use professional social media networks such as LinkedIn or AngelList, and seek out accelerators (although these groups have a different mission, you can still find alignment with people of similar minds). In our experience, the best co-founders have been colleagues of colleagues. Someone in your network likely knows the right person.

In the end, it comes down to activating your network and telling people who you know and trust that you’re looking to build your founding team. Share your idea and tell people about the strengths you’re looking for in a co-founder and the needs of the company. If you’ve made an honest assessment of your weaknesses, and you know what gaps need to be filled for the company to succeed, then this list should come easily to you. When you’re armed with a detailed description of your ideal co-founders, then this significantly drives your ability to activate your network for help. You’ll get better leads on potential co-founders when you can say to people, “I have this idea for a company. Of the four things I need to optimize for success, I possess two of the capabilities. Now, I’m looking for one or two others who can bring in these other capabilities to round out my team.”

If you plan to bring on a co-founder you don’t know, then consider working with them briefly first before you decide to go into business together. You’ll want to do this carefully due to intellectual property and legal issues - you don’t want to create a competitor right out of the gate- but it can be a great way to test the waters before jumping into a co-founder relationship without enough data. If you decide to test the relationship before committing, then put together the appropriate paperwork to protect yourself and your potential co-founder. At a minimum, set up a contractor relationship where it’s clear that the work being done is owned by the company, and in exchange, there will be some compensation. That compensation can be in cash or even stock in the company. If you decide to pursue this path, you should quickly talk to a lawyer to create a legal agreement describing your relationship.

The founding team of the company is the most important, most leveraged team in your startup, especially at the beginning. It’s not only critical to how you build the company, but has the biggest impact on shifting the odds of success in the startup’s favor. It’s also one of the primary metrics that are used to judge the company externally. Strong teams demonstrate a lot about the potential strength of a business. Weak teams do too. It’s always worth it to take a step back and build the best team you possibly can. It’s the best way to start building a successful company.

More on this topic, and many other perspectives on building successful startups can be found in my book, The Startup Playbook. Super easy to read and chock full of startup wisdom. Written by founders for founders. Check it out.

The post Don’t Hire Your Friends – The Secrets to Building a Great Founding Team appeared first on The Startup Playbook.

July 21, 2020

How to Build a Fund-Me-Now Startup Pitch Deck

Your Investment Deck – from The Startup Playbook https://startup-playbook.com

Your Investment Deck – from The Startup Playbook https://startup-playbook.comSo, you’ve kicked off your new startup, built your team and have a solid plan for the coming 6–12 months. Sometimes, entrepreneurs don’t think about the plan much. That plan — part of your overall business model — should include delivery milestones and achievements; a list of the resources you have at your disposal to make those things happen; and the metrics for the path your business is on. It is, in fact, everything that needs to go into your startup pitch deck to attract investors after all.

What you’ll need now is the pitch deck or investor deck, as it is often called. You’ll either send it to your potential investors or you’ll present it to them when you meet. Generally, the investor deck is the first formal external step in the investment process.

The Deck

The deck is roughly ten to twenty slides, created with presentation software like PowerPoint or Keynote, although it’s generally delivered in PDF form. Doing it as a PDF make it more universal, small, and it will discourage anyone from futzing with it. The deck helps to tell the story of your business and why it’s interesting. The goal with the deck is to convince investors that your company is the one to invest their money in. But, you should note that the presentation is very rarely enough — it’s often just the first step in a deliberate process.

With fierce competition from numerous startups for money, you want your deck to stand out from the pack. Many founders don’t realize they rarely present their decks to investors. Most often, you send it to them via email first, and then they’ll decide if they want to meet with you. Or, they’ll look at it prior to a prescheduled meeting. You often won’t be able to walk them through it the first time they view it or give them additional information, so your startup pitch deck has to be visually appealing, easily understandable and stand on its own.

Some of the deck’s highlights include what you’re planning to do, how much money you’re seeking to raise, why you’re raising that amount of money, how you will use the money, what it will produce, and the type of return that investors will receive. These are the types of key variables that investors look for when deciding on what startups to invest their money in.

There are some tried-and-true approaches to the creation of an investor presentation. Your deck should tell a story. It should be logical and flow well. It should be compelling and captivating to the reader. The reader should walk away having learned something new and unique.

But, the deck doesn’t need to be long. In fact, long decks either won’t be looked at or might just get a cursory glance. You should be able to get across your key messages in about 12 slides with a few more held in backup to send or present later. And these won’t be text-heavy, jam-packed slides, either. You should use graphics rich with charts and data with text that supports that information. Again, you likely won’t be with them when they’re looking at it.

It’s a Story. An Emotional Story.

The best decks open up with an emotional story or question about the market you’re selling into or the state of your customer. The story should make the viewer feel the pain that exists for the customer. This gives them a sympathetic view for the opportunity you’re addressing and the solution to the problem you’re proposing. The following few slides introduce them to your solution and then tells them why you have a unique approach to the problem or to the market. Then, of course, another slide tells them why you have the right team to take advantage of the situation.

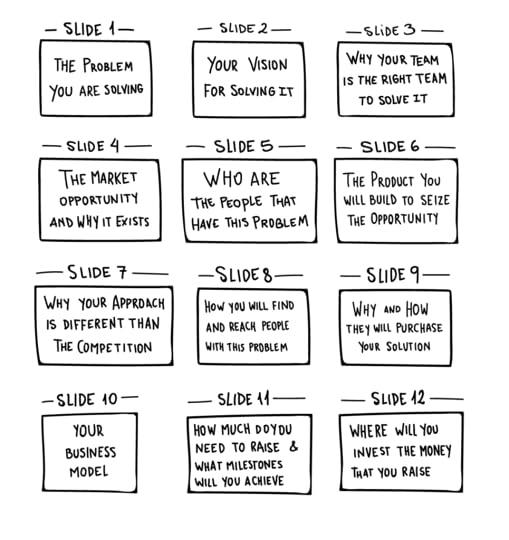

Here’s a more specific outline.

The problem you’re solving. That is, the existing customer pain. It’s a challenge to get people to invest in problems that aren’t clear to the customer. Make the pain your customer has really obvious. If you can, make it emotional to have them feel the pain themselves. 1–2 slides.The product/service you’ll build to seize the opportunity — it’s highly unlikely that you’ll have a unique solution if there’s a large market opportunity. 3–4 slides.Why your approach to the problem is different from existing solutions and the status quo — you have to assume that doing nothing is a reasonable option for your customer. 1–2 slides.Proof of product-market fit. You may not have it yet. If not, speak to the status of your efforts to establish it. It’s much better if you have proven it already. 1–2 slides.How you’ll reach the people who have the problem you’ve outlined. This is your marketing plan. 1–2 slides.How your customer will purchase your solution, Your sales plan. 1 slide.The team you’ve put together that makes your company better than any other in the market. 1 slide.How much money you need to raise and what milestones you’ll achieve with it. Show the viewer that you’ve done your homework on your real capital needs. Ask for the money, don’t be soft about it. “We’re looking for $n and we’d appreciate if you’d consider investing in us.” 1 slide.

Use Pictures to Tell the Story

The design of your deck and the imagery that you use can convey significant information about your company. Again, charts, graphics, and images can often show something about your startup rather than just using words to tell your story. Many founders often neglect to put a lot of thought into the titles of their slides, but those too can be used to your advantage. You can broadcast the framework of your story with just the headlines. And, finally, you should include a validating quote or logo from a customer or industry luminary on just about every slide. The goal with this is to give potential investors subtle positive messages from authorities that build credibility.

Remember that the startup pitch deck is likely your first introduction to an investor. Don’t take its development lightly. First, make sure you’re ready to ask for an investment. Have you vetted your idea? Have you built a solid business model? Try to delay seeking capital until you’ve carefully refined and documented your business and its plans. Then, run the deck you create based on those plans by as many people in and around your company as you can. You may only get one shot. Make sure you take your best one.

Ready to build your first company? Learn how to do it with my book, The Startup Playbook co-authored with Rajat Bhargava. Super easy to read and chock full of startup wisdom. Written by founders for founders. Check it out.

The post How to Build a Fund-Me-Now Startup Pitch Deck appeared first on The Startup Playbook.

July 16, 2020

Guest Post: The Origins of Startup Accelerators

The Startup Accelerator was born when Paul Graham wanted to disrupt the Venture Capital(VC) business by encouraging investors to make smaller investments early on in a start-up’s evolution, and funding younger founders and hackers rather than ‘older suits’. Within 10 years, there were 579 startup accelerators globally, that had invested over $206 billion in 11,305 startups with thousands of exits. Airbnb, DropBox, Reddit, Stripe, Pillpack and SendGrid are just some of the graduates of Startup Accelerator Programs. ‘Y Combinator’, the accelerator Paul Graham founded, has launched over 2000 startups globally with a combined valuation of $155 billion.

“Jessica, I’ve got this idea to start our own VC firm, but with a big twist!”. The twist — tying startup investments in with an education and mentoring program — belonged to Paul Graham. When he shared it one day in the spring of 2005 to his soon-to-be wife Jessica Livingston, she declared, “I’ll help you start it up”, and within three months, the idea became the world’s first ever ‘startup accelerator’. Paul based his twist on a model of investment a friend of his had made in own startup Viaweb which he had sold a few years earlier for $49 million.

Or so the story is told in a new book “Startup Accelerators” by Associate Professor Dr Naomi Birdthistle, Dr Richard Busulwa and Steve Dunn. Paul Graham put $100k of his own money into Y Combinator, convinced Jessica to help him run the program, and they recruited a third and fourth co-founder, Robert Tappen Morris and Trevor Blackwell, their friends and computer programmers from Paul’s startup Viaweb. Robert and Trevor put in $50K to set up an investment fund that initially invested $10K into 8 startups for a small percentage of equity, whilst also taking the startups through a 3-month summer job-style internship.

The original idea was expanded into a host of ways to accommodate more mentors into the program, from all walks of entrepreneurial life, advising the startups on how to ‘get investment ready’. The mentors also shared knowledge to startup founders on how to avoid all the challenges, dilemmas, and pitfalls they’ll likely face getting their startups off the ground. Today the Y Combinator accelerator has launched over 2000 startups globally with a combined valuation of $155 billion, and there are now around 10,000 startup accelerators held in almost every country around the world fueling local startup ecosystems and jobs growth.

Co-Authors of Startup Accelerators, Steve Dunn and Richard Busulwa, are aware of the paradox that after taking their startup through 3 accelerator programs in USA, Europe and Asia Pacific, they still have not raised an investment round. “After we wrote the book, we realized we were nowhere near ready to take our startup to the next level in the first US-based accelerator we did, and only now after graduating from three accelerator programs are we starting to find product-market fit”.

The Y Combinator co-founder backgrounds, bear some resemblance to the backgrounds of the co-founders of Apple. Mr Tappen Morris — like Steve ‘Woz’ Wozniak at Apple — were expelled from their universities for computer hacking. In Mr Tappen Morris’ case, he became famous for releasing the first serious internet virus in 1988, called the ‘Morris Worm’ and being the first person to be indicted for internet hacking under the US Computer Fraud and Abuse Act (sentenced to 3 years’ probation, community service and fines). According to both Woz and Tappen Morris, they hacked computer systems not to cause damage, but to highlight security flaws.

Despite Y Combinator’s co-founders ‘hacking’ beginnings — Paul Graham is often referred to as the ‘Hacker Philosopher’, he runs a blog called the ‘Hacker news’, and has written a book titled ‘Hackers and Painters — the Y Combinator story has been anything but rough. Their first program in 2005 began with a bang gaining successes from 4 out of the first 8 participating startups including Reddit being acquired by Conde Nast in 2006 for $20 million, and Loopt acquired by Green Dot for $43.4 million. Then a few years later the household name companies came through Y Combinator including Airbnb, Dropbox, and Instacart. The accelerator’s only hiccup came in 2018 when a software glitch notified all 15,000 applicants that applied to the program that they were accepted, only to learn a few hours later they had been rejected.

Y Combinator provides a remarkable story, not only because it has launched so many successful startups through its programs, but also because it spawned so many accelerator programs across the planet with their own successful startup alumni. Given Y Combinator’s initial success it was not surprising that competition soon followed. In 2006 David Cohen, Brad Feld, David Brown and Jared Polis started the Techstars accelerators, and now they boast helping launch 1600 companies with a combined market capitalization of $18.2 billion. In 2011, Techstars launched the Global Accelerator Network (GAN) in conjunction with President Obama’s Startup America Partnership, which linked 22 similar programs internationally.

Co-Authors of the book ‘Startup Accelerators’, Mr Dunn and Mr Busulwa took their startup LEAPIN Digital Keys through the first GAN accelerator in Australia in 2012. They had both just finished studying their Masters in Business, when Accelerators were starting to take off around the world. During the Australian GAN accelerator, Mr Dunn and Mr Busulwa met Techstars Co-Founder Brad Feld, and from that moment on they caught startup fever and become somewhat addicted to accelerator programs. “When I met Brad the ‘Godfather of global startup accelerators’ and interviewed him about what it takes to be a successful startup, I knew right then, that I had to get over to the US and do a startup accelerator there”, said Mr Dunn. The following year LEAPIN Digital Keys was accepted into an accelerator called 10Xelerator run out of the Ohio State University.

Mr Dunn and Mr Busulwa are passionate advocates for Startup Accelerators. They see Y Combinator and Techstars accelerators as pioneers in building the recent Silicon Valley startup boom. “Just look at some of the mentors in Y Combinator and Techstars who have taken their own startups and/or thousands of other startups to big successes, and you can begin to see how thriving startup ecosystems are built”, said Mr Dunn. “The mentors in these programs are simply mind-blowing — from partners in the biggest VC firms on the planet, such as Marc Andreessen, to the biggest entrepreneurial influencers and investors, such as Fred Wilson, to the former CEO of Twitter Dick Costolo, to Presidents of the biggest Media Corporations such as Michael Zeisser VP of Liberty Media which owns Formula One and SiriusXM”.

Mr Busulwa says that although mentors are a big part of startup accelerators, “our research revealed eight key benefits for startup founders including; accelerated startup evolution; accelerated learning/skills development; funding/investment readiness/fundraising support; network building; getting free/discounted professional business services; getting strategy right; ongoing advice/hands on support; and honing entrepreneur’s professionalism and confidence.

The book “Startup Accelerators” not only introduces the reader to birth of this new startup phenomenon that has swept across the business world, but it also explains what different accelerator programs offer, how to get accepted, what to do during the program, how to raise money during accelerators, what to do after the program ends, and much more. Packed with real-world case studies and advice from leading experts on startup accelerator programs, this one-stop book also provides step-by-step guidance on the entire accelerator process.

The author, Steve Dunn has attended 3 accelerators on 3 different continents. He’s an avid traveler and the co-author of the book, “Startup Accelerators.”

The post Guest Post: The Origins of Startup Accelerators appeared first on The Startup Playbook.

July 7, 2020

Introducing The Startup Playbook, 2nd Edition!

tl;dr: The Startup Playbook, 2nd Edition Launches today! Use discount code SPLB2 to get 30% off directly from Wiley or buy from Amazon, Barnes & Noble, Indie Bound or BAM.

“This book is extraordinarily fresh and exciting. In an accessible, straight talk fashion, this book is a manual, and an inspiration. The Startup Playbook is smart and avoids the ‘I am so smart’ over-writing endemic to the genre. Read this as it is presented. You’ll be doing yourself a tremendous favor.”

Amazon Reviewer

Two years ago, we set out to write the go-to book for new entrepreneurs. After starting 11 companies between us – some successes and some miserable, crash-and-burn failures – as well as investing in and advising hundreds more, it was clear that startups weren’t getting the information they needed to shift the odds of success in their favor.

The first edition of The Startup Playbook clearly filled that need. It sold out of its first printing and became an Amazon bestselling startup and overall business book. 13,000 books and 100 reviews averaging 4.8 stars later, Techstars and Wiley joined forces to publish the second edition of the book. It’s being released today!

The things that made the book different in its first printing remain in the second . . .

We aren’t academicians speaking about theories or passing on the stories of others. This book is a founder-to-founder dialogue sharing the most important things we’ve learned in the trenches.It’s thorough – it’s not a pamphlet. We expect readers to come back to it year after year throughout their startup journey. Everything we’ve learned in 45 combined years in the startup world is contained in these pages.While we’ve had a fair number of successes, we’ve both crashed and burned several times. We share many of those mistakes we made. They are valuable to understand so that you don’t repeat them yourself.We don’t tow the party line – many of our beliefs run contrary to the collective wisdom in the startup community. We think that many are self-serving and exist to help investors, advisor, mentors, etc instead of the startups themselves.

We still offer our personal, how-to guide for building a startup from the ground up. You’ll find a collection of the major lessons and shortcuts we’ve learned that will shift the odds in your favor. We share our tips, secrets, and advice in a frank, founder-to-founder discussion with you.

But, in this second edition, we’ve revised, expanded, and improved on the stories and updated the examples to be more topical. We’ve also included a new foreword by Venture Capitalist, Brad Feld, author of Venture Deals.

The book includes expanded sections focused on:

How and why you build a founding teamHow to deliver a productHow much capital you’re going to needStartup cultureDealing with funding issuesVetting your ideaAnd so much more . . .

One of the biggest pieces of feedback we got from the first edition was that it was easy to read and to apply. We’ve even improved on that in the second edition, making it a great read straight through or a resource that entrepreneurs can come back to when they have a question.

We’re thrilled to release the new edition of The Startup Playbook and to be working with Techstars and Wiley. We hope you’ll love the book and it will help you start your first venture!

The post Introducing The Startup Playbook, 2nd Edition! appeared first on The Startup Playbook.