Steven Arnott's Blog

August 15, 2020

Case Study #2 - Am I ready to retire?

Our Case Study series reviews the financial lives of everyday Canadians. While helping individuals plan and answer pressing questions, we find transferable lessons to help others navigate similar situations. If you have recommendations for future case studies or would like to be featured, please email me. While details were changed to protect the identity of our participants, the information and recommendations are reflective of the situation.

Personal and financial backgroundSummaryKathryn is a widowed 60 year old who lives in Vancouver, where she rents an apartment and works downtown in the financial services industry. She loves cooking with fresh ingredients and prioritizes spending on groceries to ensure she’s eating healthy and enjoying her time in the kitchen.

Her primary reason for reaching out was to see if she’s on track to retire in five years. She also wants to know what would happen to her retirement spending if she decided to retire earlier.

FinancesAssets: Emergency fund of $8,000, RRSP of $334,000, TFSA of $28,500, defined contribution pension plan of $16,500, non-registered investments of $105,000, and a life insurance cash value of $40,000. Total of $532,000.

Liabilities: N/A.

Income: Kathryn works in the financial services industry and earns a base salary of $86,300 plus a typical annual bonus of $9,300.

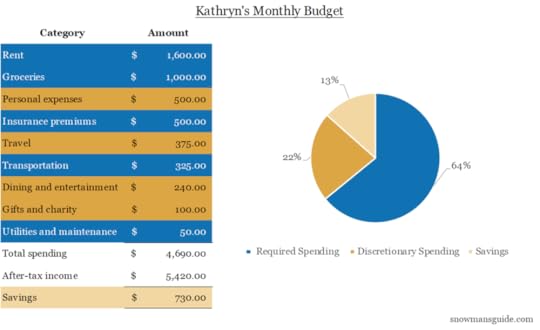

Monthly expenses: Rent of $1,600, groceries of $1,000, personal expenses of $500, insurance premiums of $500, travel of $375, transportation of $325, dining and entertainment of $240, gifts and charity of $100, and utilities and maintenance of $50. Total of $4,690.

Review and recommendationsSpendingWhen creating a budget, a typical target is to assign 50% of your income to required spending (e.g., rent, groceries), 30% to discretionary spending (e.g., travel) and 20% to savings or debt repayment. Because of the high cost of living in Vancouver, much of Kathryn’s base income goes towards required spending. She also enjoys cooking, so some of her groceries could be considered discretionary spending. Kathryn uses her annual bonus to top up her savings above the target of 20%.

Investment planning

Working in the financial services industry, Kathryn was introduced to investing fairly early in her career. While she’s been invested for years, most of her money is in mutual funds that charge roughly a 2% management expense ratio (MER). As a result, Kathryn pays close to $6,000 a year in fees. We discussed several ways to reduce these fees by moving to a low-cost solution (e.g., a robo-advisor).

If Kathryn lowered the MER from 2% to 0.7%, a typical fee for a robo-advisor, she’d save $4,000 each year. She could instead use some of this money to work with an advice-only financial planner as she sees fit.

Kathryn has roughly 60% of her savings in higher-risk investments (e.g., stocks). Based on her financial knowledge, experience in the market and long time-horizon before she needs some of her money, this risk level seems appropriate. Kathryn also mentioned that she currently has multiple non-registered accounts, Tax-Free Savings Accounts (TFSAs) and Registered Retirement Savings Plans (RRSPs). To make it easier on herself and reduce fees, Kathryn could consolidate her accounts with one or two providers.

Retirement planningKathryn’s primary goal is to confirm if she can retire in five years at the age of 65. She’s also curious how much she could spend in retirement if she chose, or was forced, to stop working sooner.

At her current age of 60, Kathryn has a 25% chance of living to at least 97. As a result, she’ll want to plan for her desired spending level until at least this age. If she were to live past 97, she would still have income from government pensions, but she’d need to reduce her discretionary spending. Another solution would be to adjust her spending throughout retirement depending on her investment returns and health.

Kathryn will need to decide when to start receiving payments from the Canada Pension Plan (CPP) and Old Age Security (OAS). Given her sizable investment portfolio and long life expectancy, she’s likely best to wait to receive OAS and CPP payments until she’s 70. Delaying CPP and OAS will reduce the risk that Kathryn outlives her retirement savings since more of her income will be guaranteed for life and increase over time.

Kathryn plans to continue renting in retirement, but she expects to move to a lower cost of living area. Between a slight reduction in rent, no longer requiring most of her insurance and reduced transportation costs, Kathryn expects to spend 15% less in retirement. As a result, Kathryn is targeting an annual after-tax budget of $45,000.

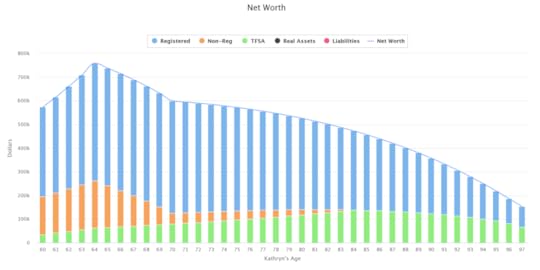

The following chart shows Kathryn’s assets growing to roughly $750,000 before she retires at 65. From 65 to 70, her savings decline at a faster rate because she isn’t yet receiving CPP or OAS. Once these payments begin at age 70, she’ll draw on her savings more slowly.

Source: Snap Projections

Kathryn was also curious about what would happen if she needed to retire earlier than 65. We looked at several scenarios, including:

Retiring today

She’d need to lower her target spending from $45,000 to $36,000 to avoid running out of savings before 97.

Retiring at 62

She could spend $40,000 a year before running out at age 95.

Part-time work earning $50,000 until 65

Kathryn can maintain her current lifestyle in Vancouver until 65 and then spend $40,000 a year in retirement.

Since Kathryn’s still enjoying her work, she plans to target retiring at 64 or 65 but was glad to see she can make it work if things change.

Tax planningKathryn has $56,200 in TFSA contribution room and $12,500 in RRSP room available. We discussed using some of her $104,000 non-registered savings to top up her registered accounts. While she’d realize some capital gains when selling her non-registered investments, she could offset this income with a contribution to her RRSP. That way, her investments would grow tax-free going forward. This small adjustment should save Kathryn roughly $500 a year in taxes.

Risk management (e.g., insurance)Kathryn has a permanent life insurance policy with a $40,000 after-tax cash value. As a widow with growing assets and no dependents, she no longer requires the coverage and is considering taking the cash value to put towards her retirement savings.

To protect against risks to her income, Kathryn will continue to maintain disability and critical illness coverage until she retires.

Estate planningKathryn plans to leave any estate assets to her remaining family members. She doesn’t have a will in place as she previously considered creating a trust. We discussed several options to ensure the right portion of her estate gets to her intended recipients. She could:

Name her family members as beneficiaries of her registered accounts. In this case, she could split the funds by specific percentages and name contingent beneficiaries in case someone passes away early.

Create a will that outlines her wishes.

Set up a trust that distributes set amounts to specific beneficiaries over time.

There are pros (e.g., simplicity, certainty) and cons (e.g., costs) associated with each option, and she could combine multiple together if she wished.

For now, Kathryn is comfortable updating the beneficiaries on her accounts.

SummaryKathryn has had a successful career in the financial services industry in Vancouver and has set aside a great nest-egg to help her in retirement. Between government pensions and her existing savings, she’s well-positioned to enjoy the retirement lifestyle she has in mind.

By taking a few simple steps to reduce her investment costs and taxes, she’ll have another $4,500 a year available for her goals.

Transferable lessonsIn each Case Study, we find transferable lessons to help you, a friend or a family member. Kathryn’s case helps us see:

How much you could save by changing your investments.Kathryn pays roughly $6,000 a year in management fees for her investments. By switching to a lower-cost solution (e.g., a robo-advisor), she could save $4,000 a year in costs.

The benefits of tax-saving accounts like the TFSA and RRSP.Kathryn had $100,000 invested in a non-registered account. In this account, any growth (e.g., interest, dividends, capital gains) is taxed. By contributing most of this money into her TFSA and RRSP, Kathryn will save $500 a year in taxes.

The complexity of trade-off decisions when planning for retirement.The retirement scenarios we looked at with Kathryn show that there are many options available when planning for retirement. There’s always a trade-off between:

working longer

taking on more investment risk

timing of government pensions and more

When you’re approaching retirement, it comes down to how much you’re enjoying your current work relative to the lifestyle you’d live if you weren’t working.

Closing remarksLearning more about your finances has different benefits depending on how far along you are in the process.

In the early stages, personal finance is mostly about increasing your income and building strong habits.

Once you have money to put aside, it’s important to invest it, while minimizing taxes and costs.

After you’ve automated your investment plan, much of personal finance is about aligning your money with your life priorities and protecting yourself from unexpected events.

The end goal of all of this is to use money as a tool to live a fulfilling life.

If you’re early in your learning process, you can check out my book for free, or purchase it from Amazon or Indigo. If you’re further along in the process or would like personal guidance, I’m available for financial planning services through Ripple Financial Planning.

Thank you to Kathryn for sharing her experience. If you have recommendations for future case studies or would like to be featured, please email me. If you enjoyed this case study, please consider subscribing to our community at the bottom of the page to receive future emails. If you know someone else who could benefit from the resources on the site, your referral is much appreciated.

July 14, 2020

Case Study #1 - Am I On Track for Retirement?

This is the first post of a new Case Study series that reviews the financial lives of everyday Canadians. While helping individuals plan and answer pressing questions, we find transferable lessons to help others navigate similar situations. If you have recommendations for future case studies or would like to be featured, please email me. While details were changed to protect the identity of our participants, the information and recommendations are reflective of the situation.

Personal and financial backgroundSummaryLeon, age 50, lives in Richmond, British Columbia, with his daughter, 18, and son, 15. They rent a three-bedroom townhouse in a housing co-op where they don’t need to worry about property management fees or the risk of being evicted.

Roughly a decade ago, Leon and his wife went through a divorce. At the worst of a financially challenging period, out of necessity, Leon began learning about personal finance. He read books, frequented forums and started to track and manage all of his income, spending and investments. Ten years later, Leon wants to know if his hard work has paid off. He wonders if he’s on track to pay for his children’s post-secondary education and to retire comfortably.

FinancesAssets: Emergency fund of $7,500, car savings of $6,500, RRSP of $120,000, TFSA of $87,000, RESP of $86,000, defined contribution pension plan of $63,000, and other investments outside Canada of $30,000. Total of $400,000.

Liabilities: Personal loan of $27,000.

Income: Leon works in the IT sector and earns a base salary of $110,000 plus a typical annual bonus of $10,000.

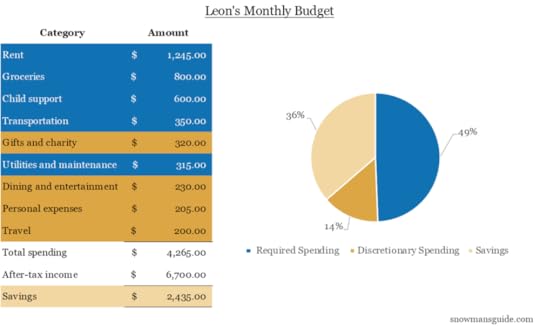

Monthly expenses: Rent of $1,245, groceries of $800, child support of $600, transportation of $350, gifts and charity of $320, utilities and maintenance of $315, dining and entertainment of $230, personal expenses of $205, and travel of $200. Total of $4,265.

Review and recommendationsSpendingLeon tracks his spending in Excel and has done an excellent job prioritizing his expenses. He’s identified the essential categories for him and his children (e.g., groceries, travel) and minimized his costs on their non-essentials (e.g., television, meals out). Leon also wanted to keep his housing costs affordable, as this is a significant component of most budgets. He did research to find somewhere that was family-friendly, affordable and stable, and eventually learned about housing co-ops.

Leon’s base income works out to $6,700 a month after-tax. Over the years, Leon has spent time identifying and developing desirable skills to ensure he remains a competitive candidate for well-paying jobs. Leon’s spending allows him to save 36% of his salary for his primary goals of paying for his children’s post-secondary schooling and retirement. He’s also working on topping up his emergency savings to $15,000 and continuing to contribute to his car fund.

Investment planning

Leon manages all of his investments himself. He’s a DIY-er who’s comfortable determining the right amount of risk to take for his goals. To keep his investing low-cost and straightforward, Leon follows a Canadian Couch Potato model portfolio and also uses some of the new all-in-one exchange-traded funds (ETFs).

With 15 years to retirement, his investments are roughly 70% higher-risk (e.g., stocks). As Leon approaches retirement, he plans to use the bucket approach that he learned about through My Own Advisor. With the bucket approach, you invest portions of your portfolio differently depending on when you plan to spend it. The money you’ll need in the next few years is kept risk-free, and cash you don’t expect to spend for ten years or more can be invested more aggressively.

Retirement planningOne of Leon’s primary concerns is whether he’s on track for retirement and if there’s anything else he should be considering.

Leon’s savings and expected income from government pensions [e.g., Canada Pension Plan (CPP), Old Age Security (OAS)] are more than enough to meet his anticipated spending. He’s targeting an annual budget of $55,000 after-tax, increasing each year for inflation. Since Leon moved to Canada later in his career, he should qualify for 75% of the maximum CPP and OAS payments.

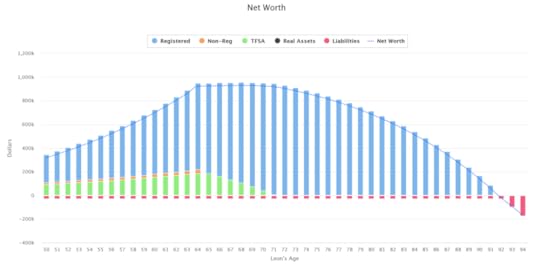

The following chart shows Leon’s annual retirement contributions of roughly $37,000 and existing investments growing to roughly $1.75 million, leading into retirement at 65. Given his current age of 50, Leon has a 25% chance of living to the age of 94 or older.

The above chart assumes Leon’s income remains stable, and his savings rate continues. If this holds he can explore the following options given his sizable expected surplus:

Save less for retirement and move that to discretionary spending.

Take less risk with his investments.

Retire earlier.

Spend more in retirement.

Gift money to his two children while he’s still living.

Plan for a sizable estate.

Since the future doesn’t always go as planned, we also looked at a scenario where:

Leon loses his job and replaces it with a position earning $80,000.

He changes his retirement target spending from $55,000 to $45,000.

His investment returns are 0.5% lower than expected.

In this case, Leon would begin to run out of savings in his 90s. He’d need to adjust his spending based on his investment returns and health throughout his 70s and 80s.

An important consideration is that Leon doesn’t yet know how he’ll spend his retirement. He could continue working part-time, volunteer or take up a new hobby. For many Canadians, entering retirement is challenging if you don’t have a plan. Much of your daily routine is now gone, and you can feel lost without goals or a community.

I recommended that Leon consider two or three areas that he wants to prioritize in retirement (e.g., giving back to his community, travelling, spending time with family, learning new hobbies). Once he knows where he’ll focus, this will also help him work towards a more specific retirement budget. MoneySense has a great article from David Hodges titled “Go beyond the numbers of retirement planning” to help consider non-financial retirement needs.

Tax planningLeon has deposited up to his Tax-Free Savings Account (TFSA) contribution limit and is regularly contributing to his Registered Retirement Savings Plan (RRSP). He’s prioritized the TFSA because of its flexibility.

He receives the Canada child benefit (CCB) for his son and has used the Registered Education Savings Plan (RESP) to help him save for his children’s education. By contributing to the RESP, Leon has received almost $14,000 in government grants that he can use for his children’s post-secondary education.

Risk management (e.g., insurance)Leon has two life insurance policies:

A term life insurance policy for $200,000 that expires in seven years once both children will have graduated.

A life insurance policy through his employer for an additional $300,000 in coverage.

As the years pass, Leon’s need for insurance coverage will reduce since he’ll have earned more money and covered more of his children’s expenses. By lowering his insurance coverage over time, Leon pays less in premium fees while ensuring his family is looked after.

Estate planningLeon has a will and power of attorney (for health and financial matters) in place that he plans to update once both his children are 19, the age of majority in BC.

SummaryLeon is in a great spot! After a challenging financial period, out of necessity, Leon took control of his finances and hasn’t looked back. He’s automated as much of his saving and investing as possible to keep things simple and remove himself from day to day decisions. While Leon acknowledges the important role his high income plays in his financial success, his habits and living below his means are also critical.

Transferable lessonsIn each Case Study, we find transferable lessons to help you, a friend or a family member. Leon’s case helps us see:

The importance of helping others to learn about personal finance.Leon provides a great example of what happens once you start learning more about your money. What began out of necessity has turned into a personal passion, and Leon is keen to share his new knowledge with his son and daughter. He’s asked them to each complete two book reviews of a personal finance or personal development book each year.

You haven’t missed the boat. You can start learning at any time.In just over a decade, Leon built up over $200,000 for his family’s future. While starting early helps, you can be just as successful starting later in life if you build your knowledge base and find the motivation. If you know what you need to do and develop steady habits, you’ll be amazed at how quickly you’ll progress.

Closing remarksLearning more about your money gives you the flexibility to live the life you want. If you’re looking to learn more, three resources on the site include:

Personal Finance Explained in Under 1,000 Words

A three-part series on where to start with your money:

Where to Start with Your Money: Major Life Events

Where to Start with Your Money: Current Financial Situation

Where to Start with Your Money: Goals and Behaviour

The Snowman’s Guide to Personal Finance: A simple approach to managing your money

Thank you to Leon for sharing his experience. If you have recommendations for future case studies or would like to be featured, please email me. If you enjoyed this case study, please consider subscribing to our community at the bottom of the page to receive future emails. If you know someone else who could benefit from the resources on the site, your referral is much appreciated.

June 17, 2020

What a Spousal RRSP is and When to Use It

Saving your money in a Registered Retirement Savings Plan (RRSP) allows you to avoid paying taxes on income today. Instead, you pay taxes later when you withdraw the money. A spousal RRSP is similar. However, instead of you paying taxes later, your spouse pays the taxes.

This is beneficial if your spouse is charged a lower tax rate than you are. For instance, if you earn $85,000 per year and your partner earns $40,000, you’d pay 32% in taxes while your partner would pay 20%. If you withdraw $10,000 from an RRSP, you’d pay $3,200 in taxes. However, if your partner withdraws $10,000, they’d pay $2,000. Therefore, you’d save $1,200 by using a spousal RRSP.

Rules when using a spousal RRSPContribution roomYou can deposit to a spousal RRSP using your available RRSP contribution room. To illustrate, consider a married couple of Jennifer and Jared. Jennifer earns $85,000 per year and Jared earns $40,000. If Mary has $20,000 available in contribution room, she could contribute $10,000 into a spousal RRSP for Jared. This way, Mary would avoid paying taxes on the $10,000 income today, and Jared would instead pay taxes on the withdrawal.

Timing of withdrawalsFor the withdrawal to be taxed in Jared’s name, he needs to wait three years before withdrawing the money. If Jennifer deposits $10,000 into the spousal RRSP in 2020 and Jared withdraws the money in 2020, 2021 or 2022, then Jennifer would need to pay the taxes on the withdrawal. Jared needs to wait until 2023 to withdraw the funds and be taxed at his lower rate.

When to use a spousal RRSPSpousal RRSPs used to be more common because they allowed couples to split their income in retirement. Rather than one person having a large retirement account, couples were able to split the savings between a regular RRSP and a spousal RRSP. However, since 2007, this is no longer necessary. You can now split pension income (e.g., RRSP withdrawals) in retirement with your spouse without needing to use a spousal RRSP.

While this limits the need for a spousal RRSP, there are still cases where the account is beneficial. We’ll review three examples below:

If you experience a year of low income ahead of retirement.

If you want to use the Home Buyers’ Plan (HBP) to help buy your first home.

If you want to retire and split income before the age of 65.

Low income ahead of retirement (Use Case #1)Occasionally, you may find yourself with a lower income for a year. Perhaps you:

Are going back to school.

Have taken maternity or paternity leave.

Are in a career transition.

Have started a new business.

In these cases, it may make sense to withdraw money from a traditional RRSP or from a spousal RRSP. If you have little or no income for the year, a withdrawal from an RRSP will allow you to keep most of the money. To illustrate, let’s consider a case where you plan to go back to school in 4 years and don’t expect to earn income for a full calendar year. You could deposit money to an RRSP, or your spouse could deposit money to a spousal RRSP in the years leading up to your school. Then, when you’re in school you could withdraw money to fund your expenses without paying high taxes.

Remember that for a spousal RRSP you’ll need to wait 3 years after the most recent deposit before withdrawing.

Buying your first home (Use Case #2)If you’re starting to save for your first home, you may consider using your RRSP to help. If there’s one high-earner in your couple, that individual could contribute to their own RRSP as well as a spousal RRSP for the other partner. This way, both partners could withdraw $35,000 through the Home Buyers’ Plan (HBP), providing up to $70,000 for a down payment.

Early retirement (Use Case #3)While the government has made it easier to split your pension income with your spouse in retirement, you’re not able to do this until you turn 65. Therefore, if you want to retire earlier and start receiving money from an RRSP, you may benefit from a spousal RRSP.

Closing remarksWhile spousal RRSPs are less common than they used to be, there are still times when they come in handy. Spousal RRSPs are another example that show how complicated the tax system is in Canada. This complication causes millions of Canadians to miss out on eligible incentives each year. To help, you can learn more ways to minimize your taxes, or work with an accountant or financial planner.

Thanks so much for stopping by the blog. If you’ve enjoyed this article, please consider subscribing to my email list in the footer to receive updates when new content is posted. If you know others who could benefit from the content throughout the site, please share the word, it’s much appreciated.

June 8, 2020

What is a Good Management Expense Ratio (MER)?

In all your daily transactions, you’re used to being quoted a price and paying it. Whether you’re buying coffee, signing up for a streaming service or making a larger purchase like a car, you know how much you’re paying. However, this isn’t usually the case when you invest. Whether you’re investing online or through a local bank branch, you’re paying a fee and you may not be aware just how much it is.

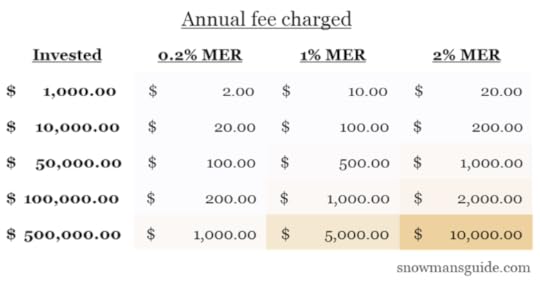

Investment fees are often presented as a low percentage. They usually range between 0.1% and 2.5%. What appears to be a small number can have a significant impact on your financial success. If you’re charged a 2% annual fee on a $50,000 investment, you’re paying $1,000 a year in fees. This fee is called a management expense ratio (MER) and it’s charged on your total investment balance. The following table shows how much you’d pay annually depending on how much you’ve invested and the MER.

Why you’re paying an MER

When you invest in an exchange-traded fund (ETF) or mutual fund, the provider will charge you an MER to select and bundle investments (e.g., stocks) together. The two main factors that determine whether you pay 0.1%, 2.5% or somewhere in between are:

Investment managementThere are two ways a fund can select and bundle investments together for you.

Passively

They follow a set list of investments with minimal research and little buying or selling.

Most passively managed investments charge an MER between 0.1% and 0.5%.

Actively

They research individual investments and regularly buy and sell them.

Most actively managed investments charge an MER above 0.8%.

The MER goes to pay for analysts who research companies and all the overhead associated with running the business.

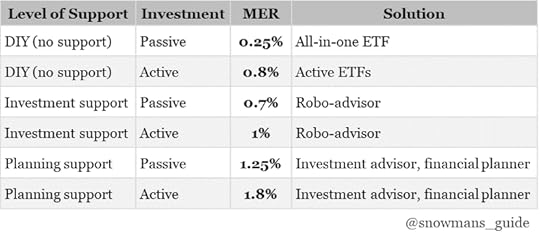

Advice and financial planning servicesIn addition to having investments bundled together for you, you may also be paying for advice and financial planning services. For instance, if you’ve purchased mutual funds through a bank branch, a portion of the MER you’re charged is paying for your advisor.

Most funds that are sold through a financial or investment advisor charge an additional 1% MER.

This fee provides you access to tailored advice and financial planning services. If you don’t need this or aren’t receiving it, then you should find a new investment solution.

What is a good MER?In summary, if you’re paying for an actively managed fund at a bank branch where you receive support from a financial advisor or planner, you can expect to pay an MER of 1.8% or more. If you open a brokerage account and invest directly in a passively managed ETF, you can expect to pay an MER of roughly 0.25%.

There is evidence that most funds that actively manage your money perform worse than passive funds. It’s hard for fund managers to earn a high enough return to offset their additional fees on a regular basis. This is mostly because the stock market is so unpredictable.

The following table presents what a good MER is depending on the type of service you’re looking for. It also provides example solutions for each.

Closing remarks

Like any purchase you make, you’ll have the option to pay more for higher quality and additional features, or less for a simpler version. Paying more doesn’t always mean it’s better for your needs. The first step to find a fair MER is to decide how much support you’ll need. The more support, the more you’ll need to pay. You can use the above table to explore solutions that make sense for you and then research further to find the right provider.

If you’re not sure whether you’re paying too much for your investments, you can work with a fee-for-service financial planner to review your situation and receive guidance. If you’ve enjoyed this article, please consider subscribing to my email list in the footer to receive updates when new content is posted. If you know others who could benefit from the content throughout the site, please share the word, it’s much appreciated.

June 5, 2020

Can I Transfer an RRSP to a TFSA Without Penalty?

The Tax-Free Savings Account (TFSA) is a fantastic way to lower your taxes and save for the future. Unfortunately, it also complicates what was previously a simple decision. Before the TFSA was introduced in 2008 you deposited your savings in a Registered Retirement Savings Plan (RRSP) and went about your day. However, today there are potential benefits of using a TFSA instead of, or in addition to, an RRSP.

Unfortunately, there’s no way to transfer money from an RRSP to a TFSA without penalty. However, depending on your situation the penalties may be minor. If you’ve deposited money into an RRSP and wish to move it to a TFSA, you’ll want to consider two things.

The taxes you’ll need to pay on the RRSP withdrawalWhen you withdraw money from an RRSP you must include that amount in your income for the year and pay taxes on it. For example, if you withdraw $10,000 from an RRSP and earn $50,000 from your job, your total income for the year will be $60,000. As a result, you’ll need to pay ~30% of the $10,000 you withdraw in taxes. This means you’ll only have $7,000 left to deposit into your TFSA.

The fact that you can’t redeposit that money to the RRSP in the futureWith a TFSA, any withdrawal you make can be deposited back into the TFSA in a future year. However, with an RRSP, if you withdraw money you’re not able to redeposit that money in the future.

When it can make sense to transfer from an RRSP to a TFSAYour income is currently lowIf you’re taking time off from work, starting a business, or otherwise earning a low income this year, it may make sense to withdraw from your RRSP and move the money to a TFSA. If you withdraw $10,000 from an RRSP in a year where you’re not earning other income, you’ll pay minimal, if any, taxes. This may allow you to move the full $10,000 withdrawal into your TFSA. You’ll then be able to avoid paying any taxes on this money in the future.

You expect to have higher income in retirementIf you expect to receive a pension from your employer when you retire, it may make sense to withdraw from your RRSP ahead of your retirement. If you combine a government pension, employer pension and withdrawals from an RRSP, your taxable income may be quite high. While this is a great problem to have, you may be able to lower your overall tax bill by transferring to your TFSA over time.

The process to move money from an RRSP to a TFSAIf either situation applies to you and you want to transfer money from your RRSP into a TFSA, there are three steps to take.

Request a withdrawal from your RRSPYou’ll need to have cash in your account to request a withdrawal. As a result, you may need to sell some of your investments ahead of time. You may be able to remain invested as you move money from your RRSP to your TFSA, however the process is more complicated. I recommend you contact your RRSP provider to discuss your options.

Pay the withholding tax on your withdrawalWhen you withdraw money from an RRSP, the company that manages your account will keep a portion of the withdrawal for taxes. They’ll send this money on your behalf to the Canada Revenue Agency (CRA), like how your employer sends taxes from your paycheque.

Depending on the amount you withdraw, the company will withhold between 10% and 30% of the money.

$5,000 or less, they’ll withhold 10%

$5,001 to $15,000, they’ll withhold 20%

more than $15,000, they’ll withhold 30%

The amount withheld may not be the amount you owe when you file your taxes. It’s important to set aside some of the money for taxes in the future if you have a high income.

Withholding rates are slightly higher in Quebec.

Contribute the remaining money into your TFSAOnce you receive the money and have set some aside for future taxes, you can deposit the rest into your TFSA. You’ll want to make sure you have enough contribution room before starting the transfer process.

Closing remarksWhile you can’t avoid penalties when withdrawing money from your RRSP, it may still be worth it. If the taxes you’ll owe are low, and you don’t need to redeposit the money to your RRSP in the future, then the penalties are minor. A simpler approach may be to leave the money in your RRSP and to start using a TFSA going forward. If you’re wondering whether you’d benefit from transferring money between accounts, you can consider connecting with an accountant or financial planner.

As always, thanks for stopping by the blog. If you’ve enjoyed this article, please consider subscribing to my email list in the footer to receive updates when new content is posted. If you know others who could benefit from the content throughout the site, please share the word, it’s much appreciated.

June 4, 2020

Simplify Your Investing with All-In-One ETFs like VBAL, VGRO and VEQT

It’s never been easier to invest your money for the future at a low cost. You can own a portion of thousands of companies and lend to hundreds of countries and businesses with the click of a button.

To help you manage your money in a hands-off and low-cost way, Vanguard, BlackRock and BMO have each recently launched all-in-one exchange-traded funds (ETFs). These funds are also called one-ticket, single-ticket or asset allocation ETFs.

What is an all-in-one ETF?When you invest in a single company (e.g., Apple, Walmart) by purchasing shares, you take on a significant amount of risk if that company faces future challenges. To minimize the risk of investing in one or two companies, a common approach is to buy many different companies—called diversification. ETFs bundle many different investments into a single package that you can easily buy and sell.

ETFs used to focus on investing in a specific geography (e.g., Canada, Europe, developing countries) or a specific investment type (e.g., stocks, bonds). As a result, people used to buy multiple ETFs to make sure they had investments around the globe and the right balance of stocks and bonds.

An all-in-one ETF removes the need to buy and manage multiple ETFs because it does everything for you. It maintains a set level of risk by investing a certain amount in stocks and the rest of your money in bonds. It also makes investments around the globe to minimize the chance you miss out on the next major trend.

Each ETF has a ticker symbol, which is a unique code to help you buy and sell the fund. As an example, one of Vanguard’s all-in-one ETFs is called the Vanguard Growth ETF Portfolio and its ticker symbol is VGRO.

Features of all-in-one ETFsThere are three major features that make all-in-one ETFs so great.

DiversificationAs we mentioned above, individual companies are exposed to many risks (e.g., lawsuits, customer reviews, regulation). If you invest all your money in one or two companies, you could lose a large portion.

Instead of buying one or two companies, all-in-one ETFs purchase thousands of investments. As an example, Vanguard’s VGRO ETF holds over 26,000 investments. This includes investments in large companies like RBC and Microsoft, as well as small companies like Sonim Technologies Inc. It also includes lending money to the Canadian Government, Province of Ontario and John Deere Capital Corp.

Low feesTo buy all the investments and bundle them together for you, the ETF provider (e.g., Vanguard, BlackRock, BMO) charges a fee called a management expense ratio (MER). All-in-one ETFs charge a low fee, ranging between 0.2% and 0.25%.

Canadians pay some of the highest fees in the world. Most mutual funds charge between 1.5% and 2.5% to manage your money. As a result, you may be paying ten times more than you need to. On a $50,000 investment, an annual fee of 0.25% is $125 compared to $1,250 if you’re paying 2.5%.

MonitoringOnce you’ve purchased an all-in-one ETF you can sit back and relax. The ETF provider will monitor the investments and rebalance if needed. Rebalancing is the process of occasionally buying and selling investments to make sure you’re taking on the right amount of risk.

Automating your investments is one of the surest ways to success. Our minds are wired to be terrible at investing. As a result, the less day-to-day involvement you have the better.

Choosing the right all-in-one ETF for your needsThere are two main differences when selecting between all-in-one ETFs.

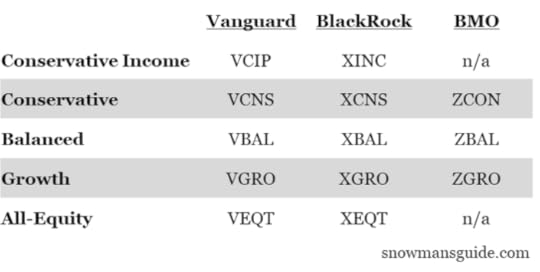

The company that manages your moneyThe three main providers of all-in-one ETFs in Canada are Vanguard, BlackRock and BMO.

Vanguard is owned by the investors of its funds rather than by shareholders.

BlackRock is the largest money manager in the world and operates the iShares brand.

BMO is the Canadian bank with the largest ETF offering.

While there are minor differences in fees and in the amount of money invested in each fund, all three companies offer competitive options.

The amount of risk you want to takeInvesting comes with different levels of risk. Leaving your money in a savings account at the bank has almost no risk whereas buying shares of a small technology company could have significant risk. To help manage this, you can invest both in equity (e.g., stocks) and fixed income (e.g., bonds).

All-in-one ETFs are available in five different risk levels.

Conservative Income (20% equity, 80% fixed income) - lowest risk

Conservative (40% equity, 60% fixed income)

Balanced (60% equity, 40% fixed income)

Growth (80% equity, 20% fixed income)

All-Equity (100% equity) - highest risk

The following table provides the unique code for each all-in-one ETF available from Vanguard, BlackRock and BMO.

How to buy an all-in-one ETF

Once you’ve decided the amount of risk you’re comfortable with for your investment goal and which company you’d like to use, you’re ready to invest.

You’ll need to open a brokerage account with any of the major banks or a digital service provider. Here’s a list of options with rankings to help you get started. You’ll need to decide whether to open a Tax-Free Savings Account (TFSA), a Registered Retirement Savings Plan (RRSP) or a non-registered account. If you don’t already have a TFSA and an RRSP, you’ll likely want to use one of these. We’ve covered the differences between the two account types previously.

Once you’ve opened your account and deposited your money, you can purchase the all-in-one ETF you’ve chosen above. Most brokerage companies have how-to guides or videos to teach how to invest on their platform. If you need further help, you can always speak with a contact representative by email, chat or phone.

Closing remarksI use all-in-one ETFs for their simplicity, low cost and hands-off approach. I’m able to rest easy because I know less of my money is going to fees and therefore more is working towards my goals. I also know that professionals are regularly monitoring the investments to make sure I’m taking on the right amount of risk. And finally, I’m able to focus on other aspects of my life and not worry about the stock market or managing my investments.

Thanks for checking out the site. If you’ve enjoyed this article, please consider subscribing to my email list in the footer to receive updates when new content is posted. If you know others who could benefit from the content throughout the site, please share the word, it’s much appreciated.

June 3, 2020

How Many RRSP Accounts Can I Have?

The great news is that you can have as many Registered Retirement Savings Plan (RRSP) accounts as you’d like. However, there’s a limit to the total amount of money you can deposit across all of your accounts.

You can only deposit to an RRSP if you have contribution room available. Each year that you earn income and file your taxes you receive RRSP contribution room equal to 18% of your income. For instance, if your income is $50,000, you gain $9,000 in RRSP contribution room that you can deposit to any of your RRSP accounts.

Contribution room that you earn each year adds up and can be carried forward. You can find out how much contribution room you have available by signing into your My Account with the Canada Revenue Agency (CRA) or by looking at your latest tax confirmation slip from CRA, called a Notice of Assessment (NOA).

Pros and cons of additional RRSP accountsNow that we’ve confirmed you can have as many RRSP accounts as you’d like, let’s look at pros and cons for having more than one.

Pros of having multiple RRSP accountsMore investment options

There are lots of investments to choose from once you open an RRSP. In some cases you may need to open a new account to increase your options. A short list of investment options includes:

Exchange-traded funds (ETFs) and mutual funds.

Guaranteed investment certificates (GICs), high-interest savings accounts and bonds.

No need to transfer accounts

If you want to have just one RRSP, then you’ll need to either stay with a single company your whole life, or you’ll need to transfer your old account each time you open a new one. For some, transferring an account can be time consuming and confusing.

Cons of having multiple RRSP accountsMore difficult to manage

Managing accounts across multiple investment options and companies can make tracking your money difficult, especially at tax time. You’ll have more monthly statements and tax forms to track down to make sure you know how your investments are performing and what you need for taxes.

You may pay higher fees

If you leave old accounts open, you may be paying more in fees than you need to. If you used to have a relationship with a financial advisor or planner, you may still be paying their fees on your old accounts. In addition, new investment options are introduced each year at lower fees, so transferring old accounts can help you keep more of your money.

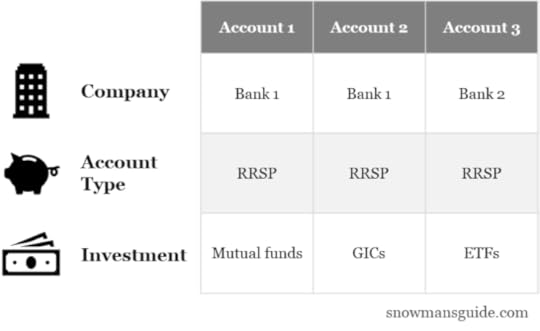

Examples of when multiple RRSPs happenYou can have multiple RRSPs at the same company, perhaps to invest in different offerings. For example, in the following table the individual has two RRSPs at Bank 1, one to invest in mutual funds and the other to invest in GICs.

You can also have an RRSP at multiple companies, perhaps because you’ve moved your business, or you’ve found an exclusive offering. For example, in the following table the individual has an RRSP at Bank 2 in addition to their accounts at Bank 1.

Closing remarks

An important question to consider when opening a new RRSP account is whether you could benefit from a Tax-Free Savings Account (TFSA). Depending on your situation, a TFSA may help you lower your taxes even further and save more for retirement. We completed an in-depth comparison between the TFSA and RRSP for your retirement savings previously. In the end, the most important step for your financial success is to set money away for the future. Whether that’s easiest with one RRSP, five RRSPs or two RRSPs and one TFSA, find what works for you.

May 29, 2020

What Happens if You Make a Mistake on Your Taxes in Canada?

Making a mistake on your taxes is more common than you might expect. In Canada, you can easily make a change to your tax return to correct the error, going back as far as ten years if required. After you submit your taxes to the Canada Revenue Agency (CRA), you’ll need to wait for them to send you a Notice of Assessment (NOA). Once you receive your NOA, online or by mail, you can follow the steps below to change your return.

Common mistakes when filing taxes in CanadaBefore we dive into the steps to change your return, it’s worth discussing some of the common mistakes people make. This way, while you’re adjusting for the error you’ve identified, you may be able to uncover other issues proactively. Common mistakes include:

Receiving a tax form after you’ve already filed your taxesPerhaps you forgot about a savings account that had earned interest throughout the year, resulting in an unexpected T5 tax slip. Or, maybe you forgot you made a deposit to your Registered Retirement Savings Plan (RRSP) and later found your tax receipt in a pile of old mail.

Forgetting to claim a taxable benefitYou may have made donations throughout the year that you didn’t realize could lower the taxes you owe. Or, you might have paid tuition for a qualifying post-secondary program and forgot to claim it on your taxes. There’s a long list of ways to lower your taxes through tax rebates and deductions.

You claimed a benefit that you’re not eligible forPerhaps you thought an expense qualified for a tax benefit, but after further research or discussions learned you weren’t eligible. Rather than wait for CRA to find the error, you can make the adjustment yourself.

Entering an incorrect value in a fieldYour income tax form from your employer (i.e., T4) can have upwards of 20 fields to copy. Some of these fields have only minor differences from one another, so it’s not surprising they can be copied over incorrectly.

Use your Canada Revenue Agency ‘My Account’ to change your returnNow that you know what you’d like to change, the process is straightforward. The first step is to create or login to your CRA My Account. This is a secure digital portal where you can view your tax information and change previous returns. When you first sign in, you’ll see a button to ‘Change my return’ under the ‘Tax returns’ section.

You can only change one year’s return at a time. If you made a mistake in the most recent year, select that year from the drop down and click ‘Next’. However, if you realize you made a mistake several years ago, you’ll need to start with that year and may need to adjust following years afterwards. For example, if you forgot to claim a tax benefit in 2016, you’ll need to first make the claim in 2016 and then may need to adjust 2017 through 2019 afterwards. Each time you submit a change to a tax return, you’ll need to wait for CRA to send you a Notice of Reassessment before you can proceed with a new change.

If you’re not comfortable making the changes yourself, you can work with a friend or family member you trust, or seek assistance from a professional (e.g., accountant). It’s worth considering the benefit you’ll receive (e.g., lowering your taxes, avoiding a penalty from CRA) against the cost and time to make the change.

Closing remarksI made an error on my 2014 and 2015 tax returns that I realized and corrected in 2016. I hadn’t realized that expenses I was paying to complete licensing exams for my job qualified for the tuition tax credit. In 2016 I changed my 2014 tax return, waited for my Notice of Reassessment and then changed my 2015 tax return. The process took roughly 3 hours over several weeks and earned me ~$600 in tax rebates, well worth the effort. Learn more about why we pay taxes in Canada and how you can avoid paying more than your fair share.

May 28, 2020

How to Buy Stocks for Beginners

Between February and March 2020, the stock market declined in value at the fastest rate in history, with most major markets declining over 30%. Meanwhile, another record was being set through Google’s search engine. People around the world were looking to take advantage of the decline in stock prices and searching “how to buy stocks.” The following graph shows the stock price of a group of global stocks in blue and the relative search rate for “how to buy stocks” in gold.

Sources: Yahoo Finance adjusted closing price for VTI , a major exchange-traded fund (ETF) . Google Trends .

With a great deal of media coverage on the pandemic and its impact on the stock market, many people were drawn to what has been called a generational opportunity to buy stocks. Before you dive in and buy stocks yourself, I’d like to discuss a checklist of steps to consider and provide a system to help you be successful.

What to consider before buying stocksInvesting in the stock market can help you grow your savings for the future. I’ve spoken previously about how the stock market works and the power of compound growth for your financial future. At the same time, I’ve discussed the risks of investing and why the market declined in value in March. If you want to invest in the stock market, please consider the following opportunities and risks before moving ahead:

Pay off medium to high-interest debtIf you owe money on a credit card or a personal loan that charges 10% interest or more, you may be better off paying down your loan rather than investing.

Create an emergency savings account with 3 to 6 months of mandatory expensesWe’re seeing record unemployment in Canada after shutting down much of the economy to slow the spread of the virus. If you lose your job or have an unexpected expense, you don’t want to have to sell your stocks at a potentially lower value.

Don’t invest money you’ll need in the next few yearsWhile the stock market has historically been a great way to build wealth, it takes time to do so. There’s no guarantee the stock market will be higher in a year or two than it is today. Therefore, it’s dangerous to invest money that you can’t afford to lose, or that you’ll need in the next few years.

Avoid buying individual stocksOur brain is wired to be terrible at buying individual stocks. We’re driven by emotion and make decisions using shortcuts. As a result, a more dependable approach is to invest in a broad range of companies rather than trying to pick and choose the winners.

If you’re in a stable financial situation and are looking to invest your money in the stock market, we’ll discuss your options and systems you can put in place to be as successful as possible.

Opening an account to buy stocksInvesting in the stock market has never been easier. You can open a brokerage account with any of the major banks or a digital service provider. Here’s a list of options with rankings to help you get started. You’ll need to decide whether to open a Tax-Free Savings Account (TFSA), a Registered Retirement Savings Plan (RRSP) or a non-registered account. If you don’t already have a TFSA and an RRSP, you’ll likely want to use one of these. We’ve covered the differences between the two account types previously.

Once you’ve opened your account, you have the option to invest in individual stocks or a bundle of stocks through an exchange-traded fund (ETF) or mutual fund. Purchasing an ETF that bundles a bunch of stocks together for you is the easiest way to take advantage of the stock market’s future growth without much overhead. The Canadian Couch Potato has been providing ways to invest in a low-cost, hands-off way for years.

Creating a system to buy stocksIf you want to invest in individual companies with a portion of your money, there are important steps to consider.

Managing your emotions is criticalFear and greed can overtake your rational thoughts in a second. You may have invested based on sound research and then if the stock drops in value you could panic and sell, locking in a loss. In addition, if your investment increases in value, greed may overtake you and you may invest more of your money than you should, assuming it will continue to go up.

Create a system to help you avoid emotions and rash decisionsBefore you buy a stock, you should know the following:

Why you’re buying it (e.g., why do you believe it will increase in value in the future).

When you’ll sell it (e.g., once the company successfully launches a new product, once the stock increases in value by 30%, if the stock drops in value by 20%, if the future outlook for the company declines significantly).

Avoid the belief that anything “has to happen,” there are no guarantees.

Once you’ve developed a system and decided what companies you want to invest in, it’s a matter of:

Logging into your brokerage account you opened earlier and depositing your money.

Finding the stock symbol for the company (e.g., Apple’s stock symbol is AAPL, Walmart’s stock symbol is WMT).

Investing your desired dollar amount into shares of the company (e.g., if you want to invest $1,000 in a company and its shares cost $20, you will buy 50 shares).

Following your system without deviation. If you said you’d sell at a set price or after a specific event, it’s important to stick to your plan. The more you allow your emotions and shortcut decisions to drive your investments, the more you’re at risk.

With most brokerage companies you’ll need to pay a fee of ~$10, called a commission, each time you buy or sell a stock. Most brokerage companies have how-to guides or videos to teach how to invest in stocks on their platform. If you need further help, you can always speak with a contact representative by email, chat or phone.

Closing remarksAfter years of academic and practical experience investing in the stock market, I can assure you that emotions are challenging to overcome. There are tens of thousands of individuals around the world who dedicate their lives to investing in the stock market. They have advanced computing capabilities and access to proprietary data. Even these individuals have difficulty earning better returns then the overall stock market. If you want to grow your money for the future, I’d encourage you to consider a simple, low-cost investment in an ETF that bundles thousands of companies together. Once that’s done, forget you bought it and avoid looking at your investments. Building wealth takes time and patience.

Thank you for checking out my site. If you’ve enjoyed this article, please consider subscribing to my email list in the footer to receive updates when new content is posted. If you know others who could benefit from the content throughout the site, please share the word, it’s much appreciated.

April 30, 2020

Thoughts on the Stock Market Rebound

Just over a month ago we discussed the sell-off in the stock market caused by the current pandemic. At the time, there was a great deal of uncertainty clouding what the future would look like. When the article was published, we had 4% of the confirmed cases we have today in Canada. Markets across the globe were down ~30% and an index that measures investor fear was at its highest level on record. Since then, stock markets around the world have risen at some of the fastest rates since the Great Depression. Most major markets have recovered ~50% of their March losses.

This market rebound has taken place as we’ve seen several negative, record-breaking economic stats and with a significant uncertainty still present. As a result, the market rebound has many people wondering if we’ll eventually see a drop in stock prices. While I don’t know if the market will go up or down from here, I wanted to share a few important points for consideration.

Factors that could justify current stock pricesThere are three factors I’d like to discuss that could help justify the rebound.

Investor’s expectation for future returns may have declined over the last two months.

We’ve seen an unprecedented response (i.e., speed and magnitude) from many governments and central banks.

There is a battle between two risks competing for investor attention.

Return expectationsSince January, the return being offered to owners of 10-year government bonds declined from ~1.6% to 0.56% in Canada. This means investors are willing to accept a lower future return today than they were two months ago. If this is the case for bond investors, it may be the case for those buying stocks as well. Therefore, even though earnings are expected to decline over the next few years, the current value of those earnings may still be close to what they were in January.

If stocks return to their all-time highs, it’s not the same as saying the stocks are as valuable as they were in January. It’s saying they’re as valuable, relative to all other investment options, as they were in January. When you consider other options, paying current prices could make sense. However, you’ll likely need to lower your expectations for future returns.

Unprecedented responseGovernments around the globe have responded to the crisis with support for those impacted. Programs include payments to individuals who lost their job, small business rent relief, partially forgivable loans and more. In addition, central banks have lowered interest rates and provided significant lending to governments and businesses alike.

These activities have helped to limit the worst-case scenario. As we discussed during the sell-off article, investors consider the full range of potential future outcomes, and often overweight the worst-case scenario. As these scenarios come off the table, the value of stocks can jump significantly. This is the same reason that stock markets can rise even though data seems worse than expected. Each new piece of information removes a bit more of the uncertainty and fear.

Competing risksThere are two risks that investors are struggling with right now.

The risk of investing before a further market decline.

The risk of waiting and watching the market rise.

With an increasing number of recoveries to reference (e.g., 1932, 1987, 2003, 2009) investors may be more confident than ever that stocks will eventually recover. If enough investors are confident the economy will recover in the next few years, they may be willing to look past current uncertainty. I wrote about this idea recently when discussing the idea of an overvalued stock market more broadly. The main takeaway is that even if the market is overvalued, which is difficult to determine, that doesn’t guarantee it will drop in price.

Closing remarksIt’s likely we’ll see further volatility in the stock market over the coming year. As we’ve discussed previously, these short-term fluctuations are irrelevant if you have the right time horizon and risk tolerance. Setting up an emergency savings account if you can will help provide peace of mind through the coming months. In addition, if you need your investments soon, the market is providing an opportunity to adjust.

Investing in a low-cost, diversified investment and ignoring the headlines has historically provided the surest way to a strong financial future. If you’re not certain what to do in these times, please feel free to reach out with any questions.