Bec Wilson's Blog

August 23, 2025

Big age pension changes are coming on 20 September – here’s what they mean for you

Feature: Big age pension changes are coming on 20 September – here’s what they mean for you

From Bec’s Desk: So much purposeful work

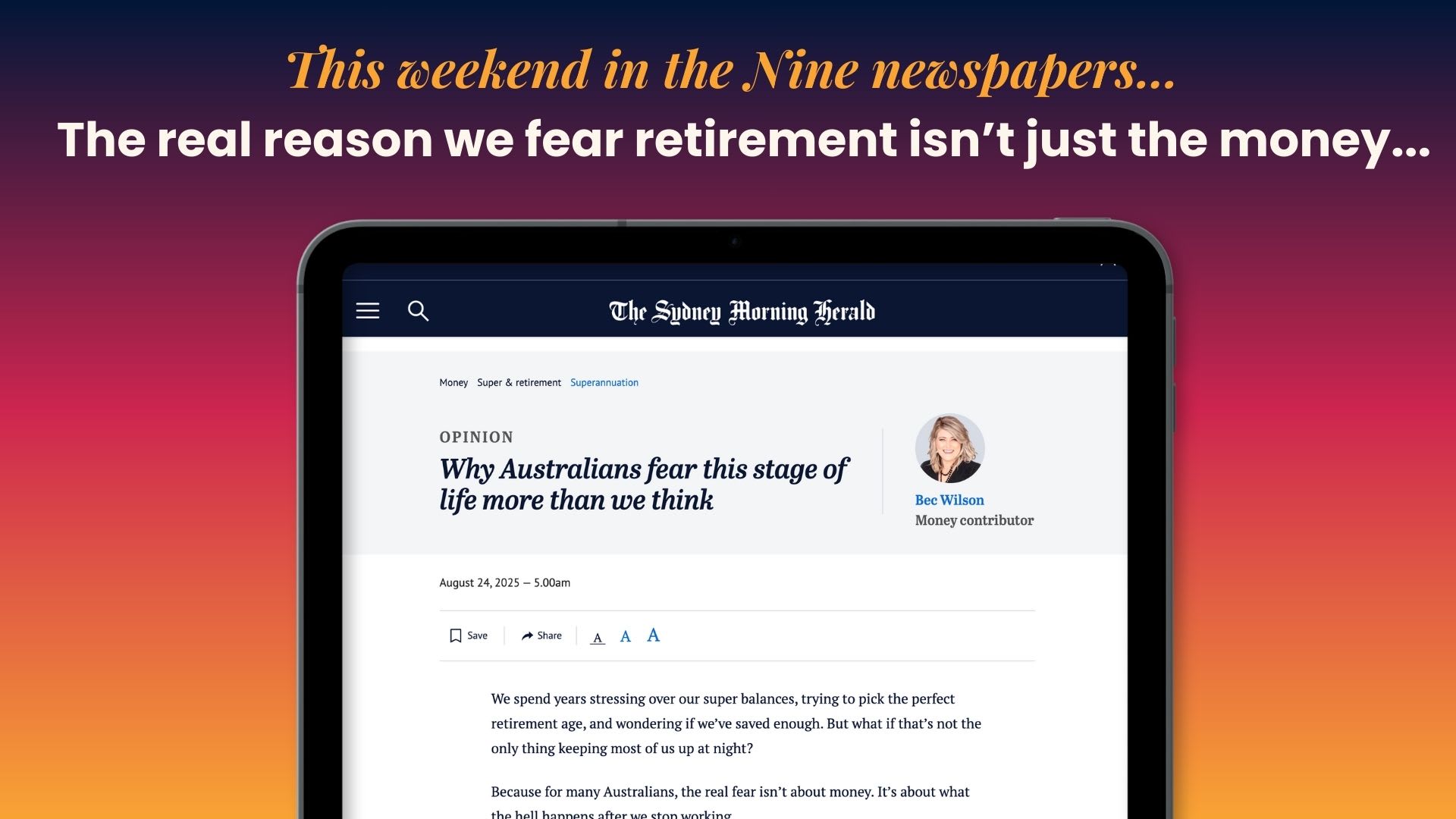

SMH/TheAge: Why Australians fear this stage of life more than we think

Prime Time: What being the executor of a will ACTUALLY looks like

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Ad - Before we start — a big thanks to our newsletter sponsor this week, Viking

Start early, stay longer. Journey further

Start early, stay longer. Journey furtherTime is running out to save up to AU$4,800 per couple when you add an extension to your 2026-2028 river, ocean or expedition voyages*.

Our pre- and post-extensions are designed for the curious traveller, those who seek to fully understand a place. Whether you extend your stay in your embarkation or disembarkation city, or journey to a new destination, each extension enriches your journey.

With over 300 Viking-curated cruise extensions available, there has never been more choice when it comes to extending your journey and exploring more of the world in comfort and style. Offer ends 1 September 2025.

*T&C’s apply

Big age pension changes are coming on 20 September – here’s what they mean for you

Big age pension changes are coming on 20 September – here’s what they mean for youIf you’re retired (or thinking about it) and get any form of age pension, 20 September 2025 is a date you’ll want to circle. The Age Pension is about to change in two ways – and depending on your situation, you’ll either come out a little further ahead or find the system clawing some of it back.

This is the biggest pension boost in yearsFrom September, the maximum Age Pension will rise thanks to indexation – the automatic adjustment that happens twice a year to keep payments in step with living costs.

Singles will get an extra $29.70 per fortnight, taking the full rate to $1,178.70.

Couples will get an extra $22.40 each per fortnight, taking the combined payment to $1,777.00.

It’s the biggest bump in two years. For many retirees, that’s a welcome lift when the cost of groceries, power bills, and petrol just keeps edging higher.

The flip side – deeming rates are back on the move for the first time in three yearsHere’s where it gets interesting. For three years, deeming rates – the rates Centrelink uses to “deem” how much income your savings and investments are earning – have been frozen holding eligibility for the pension using the income test artificially low. That freeze shielded part-pensioners from cuts while interest rates soared and gave a lot of people access to the Commonwealth Seniors Health Card too. But those days are now firmly OVER!

From the 20 September 2025, the freeze ends. Deeming rates will rise by 0.50% across both the lower and higher bands and this will particularly affect those assessed by the income test.

Full pensioners with few assets? You’ll likely keep the full boost to age pension rates.

Part-pensioners with super or investments? You could see some, or all, of that increase to pension rates clawed back. Why? Because Centrelink will assume your money is earning more in their calculations – whether it is or not.

People who can’t get the pension but are getting the income tested Commonwealth Seniors Health Card - now might find that in jeopardy.

About half a million Australians are using the income test for their Pension eligibility - and at least a third of them are said to be affected by this change.

Why this matters for your retirement planningFor retirees already in the system, this is a timely reminder that the age pension rules aren’t fixed. A government tweak here or there can change how much lands in your bank account each fortnight, and over time the government will continue to tweak the rules to suit their revenue models.

For pre-retirees, it’s a wake-up call: relying solely on the Age Pension is tough. The pension system is designed as a safety net, not a luxury. And while deeming rates are finally on the move after three years, they’re still well below what your super fund is likely earning and can earn on balanced or growth settings. In practice, that means the system will usually assume you’re earning less than you really are — but it also shows how easily a policy change can affect your retirement income.

This is why building extra buffers – through super, savings, or investments – matters so much. The more you control, the less you’re at the mercy of policy shifts.

The bottom lineFrom 20 September, there’s more money for everyone on the pension. But if you’ve got assets that are generating an income, Centrelink’s update to the deeming rate might take away with one hand what indexation gives with the other.

So stay alert!

It’s been a long, tiring, but wonderful week on the road — and worth every moment. Things kicked off with Bill McDonald on 4BC Radio Monday morning, then a full hour of radio on ABC Late Nights that evening. (I couldn’t believe how many people tune in to that show — the messages afterwards were amazing!)

The week wrapped up on Saturday at GMHBA Stadium in Geelong, keynoting a Lifestyle Communities event about the six pillars of an Epic Retirement. The energy in the room was incredible — such a powerful reminder of why these conversations matter.

And in the middle of all that, we officially launched something I’m so proud of: The Epic Retirement Tick, powered by Chant West. We’ve set out 18 criteria to measure how well super funds are serving their members as they approach and enter retirement. To earn the Tick, a fund has to score above the median on at least 12 of those 18. On 2 October, we’ll announce — through the media — which funds hit the mark. You can learn more or register to get the free report here.

Why? Because retirement products and services have been neglected for too long. Even the regulator says progress on retirement by funds is ‘patchy’. The Epic Retirement Tick is about shining a spotlight on the funds that are stepping up — and giving you the power to ask your own fund: are you prioritising retirement, or not? Together, we can raise the bar.

In between, I squeezed in an appearance on Today Extra to share the Tick story, signed copies of Prime Time at bookstores in Sydney and Melbourne, recorded new podcast conversations, and ran a two-hour education session for the Psychotherapy and Counselling Federation of Australia on how Prime Time and the science of modern ageing are reshaping the way we think about life after 50.

It’s been huge. But every talk, every signing, every conversation reminded me why this work matters — and why I’m so energised to keep pushing for better retirement literacy, and to make our Prime Time more visible in all of our lives then help people have an epic retirement.

Next week, our next six-week How to Have an Epic Retirement course kicks off — and I can’t wait to welcome the new group of around 300 people - our biggest ever. There’s still time to join us, and you can get 15% off with the coupon code EPICSPRING15. Register here.

Now, after a massive week, I’m off to do something completely different — heading to a disco with my daughters for a Saturday night girls’ night. And to Lions Hawks on Sunday too. After all, my prime time isn’t just about work, it’s about play too. I hope you’re catching some sunshine (and footy) this weekend — it’s been pretty wet and miserable everywhere except Melbourne this week!

And if you’re up early with a cuppa Sunday morning, I’ll be on 7 Sunrise at 8.15am Sunday 24th — tune in if you’d like to catch the conversation live.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Extract of of my weekly column in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 24th August 2025.

Why Australians fear this stage of life more than we thinkWe spend years stressing over our super balances, trying to pick the perfect retirement age, and wondering if we’ve saved enough. But what if that’s not the only thing keeping most of us up at night?

Because for many Australians, the real fear isn’t about money. It’s about what the hell happens after we stop working.

It’s the fear of losing purpose. Losing that feeling of being useful or connected. We’re scared of drifting through 25 or 30 years without the rhythm and identity that work gives us. Once upon a time, retirement was the prize at the end of the grind - freedom from the job that wore down your body and stole your weekends. But work has changed. These days, it can be a source of social connection, meaning, and – dare I say it – even enjoyment.

So when we step away from it, the real question becomes: what now?

New data from UniSuper’s Retire with Purpose report, released this week, shows this fear is real. Yes, 68 per cent of Australians still worry about outliving their money. But 61 per cent also worry about losing the social ties they’ve built at work. That’s not a financial fear. That’s a human one. And frankly, we don’t talk about it enough.

Instead, people avoid retirement planning altogether, not because they’re broke, but because they’re terrified that even thinking about retirement makes them irrelevant. They say things like “I’m not ready” or “I don’t want to retire and fade away”. And honestly? I get it.

Read on — this article continues in The Age, The Sydney Morning Herald, Brisbane Times and WA Today. It is free to read.

What being the executor of a will ACTUALLY looks like

What being the executor of a will ACTUALLY looks likeIn this thoughtful and candid episode, I’m joined once again by the always generous and wise Mike Chesworth. After decades in financial services, Mike recently stepped into a new role — not in the boardroom, but in the deeply personal process of executing his late father’s estate.

From paperwork and probate to family dynamics and difficult conversations, Mike shares what he learned, what surprised him, and what he’d urge others to prepare for now — before the time comes.

Whether you’ve been named as an executor, are planning your own estate, or simply want to better support ageing parents — this one’s full of practical guidance and real insight.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

August 16, 2025

Introducing the Epic Retirement Tick

Feature: Introducing the Epic Retirement Tick

From Bec’s Desk: Will I see you in Geelong?

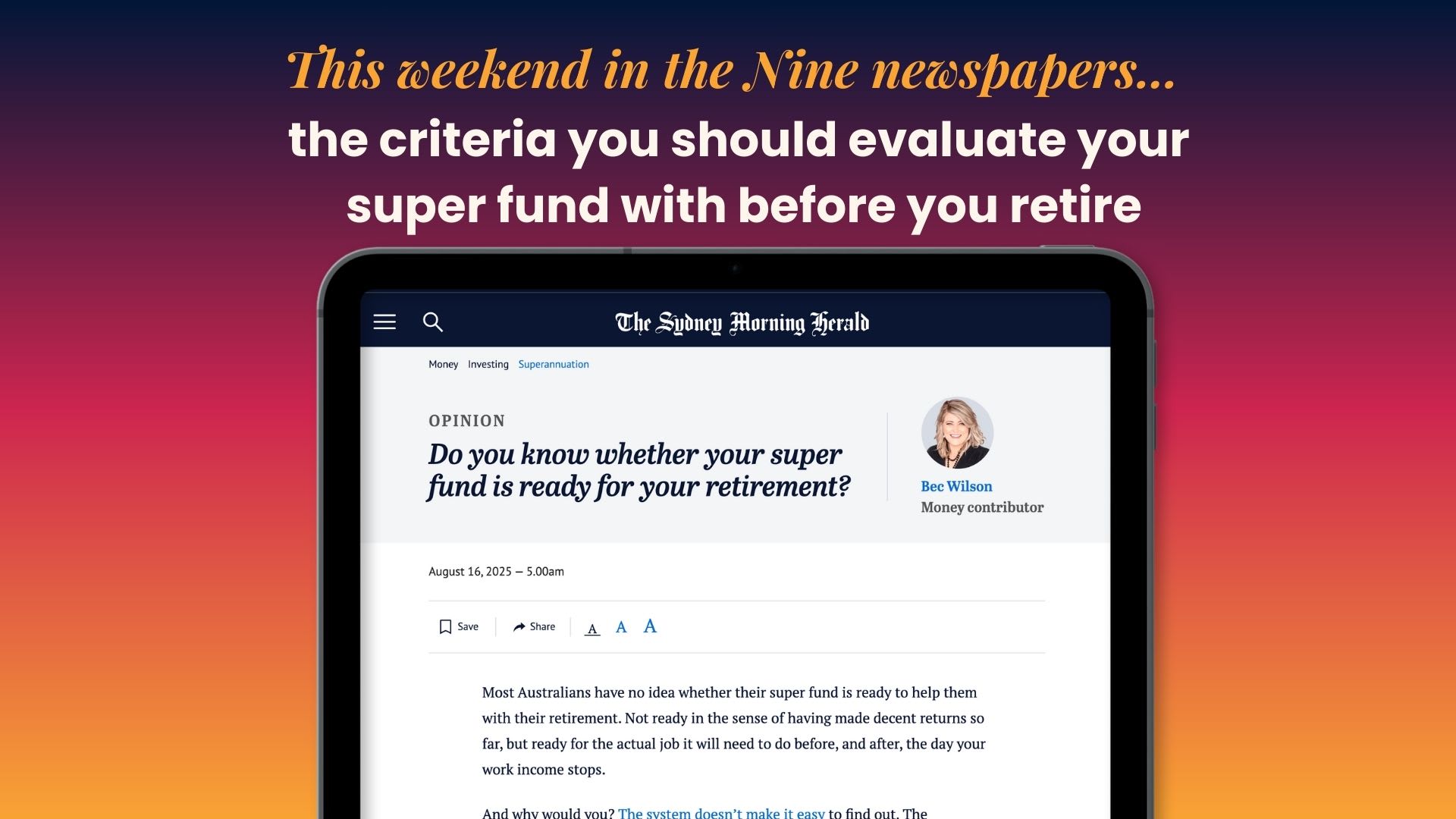

SMH/TheAge: Do you know whether your super fund is ready for your retirement?

Prime Time: How not to become a grumpy old bugger

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Ad - Before we start — a big thanks to our newsletter sponsor this week, UniSuper

No full stop: How Aussies are finding purpose and connection in retirement

No full stop: How Aussies are finding purpose and connection in retirementWhile retirement is often thought as the time for overseas adventures or endless rounds of golf, UniSuper’s new Retire with Purpose study shows that Australians are rethinking what it means to be retired.

The data reveals 61% of working Australians are worried about losing friendships forged in the workplace once they retire, and that 4 in 5 plan to keep working in retirement, be that through a new job, volunteering or flexible, hybrid work.

The study concludes that seeking professional financial advice is the key to retiring with confidence. So, book in that session with your financial adviser today!

Introducing the Epic Retirement TickFor months I’ve been working quietly with the team at Chant West, one of Australia’s leading super fund ratings providers, on something I believe could change the way retirement is prioritised by funds. And now I finally get to share it with you.

It’s called the Epic Retirement Tick.

Here’s why it matters.

Most Australians spend 30 or 40 years building their super. And while funds have become pretty good — and pretty similar — at the accumulation phase, almost no one knows if their fund is actually ready to support them in retirement. Not just with returns, but with the things that really matter when the pay stops: learning how money works in retirement, setting up a pension account, deciding how much to draw down, weighing up whether you need an income-for-life product, and navigating all the little transitions along the way.

Even the basics count. Opening an account quickly, paying your pension on time, making sure it’s secure with multi-factor authentication — these are the things that should be standard, but too often aren’t.

The truth is, the system doesn’t make it easy for everyday people to know which funds are doing well at retirement, and which are not making it their highest priority. And I don’t want to share opinions here — I want to work in facts (you know that’s always my way). The fact is, the regulator has been pointing out for years that funds are too slow at the move to suitable products and services for the retirement phase. Just last week, APRA said again that some funds are doing better than others, but overall progress is patchy.

And here’s my view: many funds aren’t in a hurry to improve, because they don’t think consumers will notice. But they might hurry things up if you start looking and asking questions with clarity about what to look for.

I don’t want to wait anymore while pre-retirees and retirees miss out. I want to celebrate the funds working hardest for their retirees, and provide helpful criteria so the not-so-good can either get better, or you can understand their points of weakness.

So, I’ve partnered with Chant West to create a clear, independent set of 18 criteria that define what “retirement ready” really means. These criteria cover everything — investments, products, drawdown guidance, advice, calculators, education, engagement, and service. Chant West will do the assessment, and I’ll help you understand how to use it. If a fund meets at least 12 of the 18 criteria, they’ll be eligible for the Epic Retirement Tick. And I suspect only a handful of funds will meet the 12 criteria on the first go — but we’re going to encourage, support and show them the way to get there too (not name and shame those who don’t). And then we’ll empower you with choice and insight! And the only way we get there is by talking about the criteria consistently, and expecting action.

The Tick will only drive real change if people like you care about it. If you read the criteria, sign up for the report, and start asking your fund when/if they plan to step up. If you’re willing to look closely at whether your fund is truly prioritising people heading into retirement now and into the future.

That’s what will mobilise action. I’m sure of it. All of a sudden, funds will start pushing those projects forward — because they’ll know you’re watching, you understand your needs, and you know what good looks like now.

The first report will be released on 2 October 2025, but the criteria are public from this weekend — and you can see them on my website now. You can also sign up to get the report when it drops (free).

Let’s raise the bar on superannuation fund services together. This is the power of people — and together I suspect we can make change happen.

Check out my website and sign up for the free Epic Retirement Tick report that will drop in 6 short weeks. I’m excited - we’re working hard on this!

As you can see, this week I’m sharing a really important project. Yesterday my article launching the Epic Tick (below) went a little bit viral in Nine Newspapers all over the country in digital and today' it’s in print in all the papers. A great start. 6 weeks until the report drops. Watch this space.

It’s been a big week in other ways too. We’ve sent out around 300 welcome packs for the upcoming How to Have an Epic Retirement Flagship Course, kicking off on 28 August. There’s still time to join us — use coupon code EPICSPRING15 for 15% off. This will be our biggest course yet, which means more questions, more chatter, and more stories shared along the way.

The week ahead is just as full — I’ll be on the road in Sydney and Melbourne visiting bookstores, signing books, stopping in for another spot on Today Extra, filming with 60 Minutes (I know, right!) and recording some exciting new podcasts. I’m also the speaker for the professional development event for the Psychotherapy and Counsellors Federation of Australia (PACFA). They’re learning about the new life stage of Prime Time so they can better help pre-retirees through their real life changes.

Epic Retirement Event in Geelong… next weekend.

If you’re in Geelong next weekend, get out your diaries - I’d love to see you in person! I’ll be the guest speaker at a special event hosted by Lifestyle Communities, talking all things How to Have an Epic Retirement. I’ll walk you through the 6 pillars of an Epic Retirement (with a few juicy Prime Time lessons thrown in) at GMHBA Stadium next Saturday at 10am. If you’d like to come along, RSVP here. They’ve said “you’re very welcome to come” - but places are limited so please register.

PS - how good is the podcast below on ‘How not to become a Gumpy Old Bugger’ - Geoff is so funny - you have to listen!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Do you know whether your super fund is ready for your retirement?

Do you know whether your super fund is ready for your retirement?

Extract of the national article kicking off The Epic Retirement Tick published in print and digital in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 17th August 2025.

Most Australians have no idea whether their super fund is ready to help them with their retirement. Not ready in the sense of having made decent returns so far, but ready for the actual job it will need to do before, and after, the day your work income stops.

And why would you? The system doesn’t make it easy to find out. The government’s performance test will tell you if your default MySuper fund passed or failed on investment returns and fees, but it is a narrow, product-focused measure (that most people don’t understand anyway) and it ignores a fund’s broader services and capability. It is like judging a car by petrol consumption and top speed, with no idea whether the brakes work, the seatbelt will hold, or even where it plans to drive.

Last week, the Treasury Department finally released a consultation paper on a new retirement reporting framework for the super industry. It promises greater transparency on the products and services funds offer in retirement and how well they deliver — but the data won’t be public until 2028 (and we’ll likely still have to dig to find the detail). By then, the biggest wave of baby boomers will have already crossed into retirement.

At the same time, Australian Prudential Regulation Authority deputy chair Margaret Cole told the Conexus retirement industry conference that while super funds are making progress under the retirement income covenant – a three-year push to improve services for retirees – it’s patchy, and not a single one rated their own performance as “excellent” in the latest survey for APRA and the Australian Securities and Investments Commission.

Some funds are acting on the call for change, others remain stuck in accumulation-phase thinking. The gap between where the industry is today and where it needs to be is still wide, and if we wait until 2028 to shine a light on it, millions of Australians could find out too late that their fund wasn’t ready when they needed it most.

That means there is still no clear measure of whether you can get the right advice when you need it, whether your investment options are designed for the pension phase, whether the planning tools are easy for you to use, or whether even the basics – such as your pension payments – will be done well and on time.

This gap matters. You can spend 40 years building your super balance, but if your fund is not ready for the retirement phase, you could end up facing complex decisions about income streams, drawdowns and the age pension with little tailored help and a lot of frustration.

That is why I have decided to do something about it, and it needs your help to work. I have been working with Chant West, one of the leading super fund research and ratings businesses, to create a set of criteria you can use to judge whether your fund is good enough for you as you approach retirement.

Read on — this article continues in The Age, The Sydney Morning Herald, Brisbane Times and WA Today. It is free to read.

How not to become a grumpy old bugger

How not to become a grumpy old buggerIn this episode of Prime Time, I’m joined by Geoff Hutchison, retired ABC broadcaster, former 7.30 reporter, and author of How Not to Become a Grumpy Old Bugger - a very funny newly released and seriously valuable self help book for older men. We dive into why some men get grumpier as they get older, how that grumpiness affects their relationships, and what they can do to turn it around.

We dive into why some blokes slide into grumpiness as they age, how it chips away at relationships, and how to turn it around. We talk health, self-awareness, friendships, listening better, letting go of regret, embracing change, and even giving the future a go (yes, that includes new tech). It’s funny, it’s warm, and it’s full of practical takeaways — whether you’re worried about your partner, your dad, or yourself.

And it’s a perfect show for anyone who’s a grumpy old bugger in the making, married to one, or keen to avoid becoming one altogether.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

August 9, 2025

The fear of never having enough to retire

Feature: The fear of never having enough to retire

Newspapers: “A call to action for mid-lifers: Rethink retirement”

Podcast: Getting AHEAD of Perimenopause

From Bec’s Desk: We did it! #1 Aussie self help book!

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

😎 Prime Time is the #1 bestselling Australian self help title this week across all bookstores. And #4 on the non fiction bestseller list overall 😎More on this below. in ‘From Bec’s Desk’!

The fear of never having enough to retire

The fear of never having enough to retireDoesn’t matter if you’ve got $100,000 or $3 million in super, almost everyone I talk to thinks they’ll never get to ‘enough’. They feel like there’s always a bit more saving to do. Always a bigger number in mind. But at some point, we need to recognise when that fear tips into the irrational.

It’s hardwired. Humans have been worrying about running out since we were stashing food for winter in caves. Back then it was dried meat and grains. Now it’s retirement savings. Same brain, different fears.

Psychologists call the first concern loss aversion and point out that we feel the pain of losing something about twice as strongly as the pleasure of gaining it. So when you imagine running out of money, your brain reacts like it’s already happening, and it pushes you to keep chasing “just a bit more” for safety.

Think about it like this - when you gain $50,000 in your super account it feels good. But, when you imagine losing $50,000 from it, it feels much worse. So much worse that your brain over-weights the risk and pushes you to keep stockpiling “just in case.”

It’s one of the big reasons why even very financially secure people still fear running out of money — it’s not purely rational; it’s hardwired into our caveman brains.

Then there’s another psychological issue called future uncertainty bias. Your brain hates not knowing what’s ahead, so it overestimates the risks and stimulates your fears. Even if the numbers show you’re fine, the what-ifs - market crashes, health issues, longer life than expected - make you feel like you need an even bigger safety net.

Add in today’s noise like market headlines, rising living costs, not knowing how long you’ll live or what family curveballs might come, and no wonder your head says keep going, you’re not there yet.

And, not surprisingly, even when you hit the number you thought was enough, your brain will quietly slide the goalposts forward into the future. That’s why the feeling never really disappears.

So how do you stop it running the show?

1. Get clear on your numbers

Write your staged Prime Time (or Epic Retirement) budget. Know what you spend now, what you might spend later, and where the money’s coming from. And remember. you’ve got more levers than you think: super, investments, downsizing, part-time work, delaying the big spends until later and if all else fails - the age pension will be there in Australia to catch you.

2. Give yourself breathing room

Build in a buffer. It doesn’t have to be huge, just enough that you can handle a surprise without it throwing your plan.

3. Focus on the life, not the number

The real win isn’t hitting some magic balance. It’s knowing what you want life to look like and having more than one way to fund it. Remember the point I make in the front of both my books - we’re chasing a number that will give us ‘choice’. Not the perfect or the biggest number we can have. You’ve no doubt heard the old adage — no point being the richest chump in the graveyard.

That fear? It might always be there in the background and you might have to learn to live with it. But with a plan, you can turn it into background noise - instead of the thing keeping you up at night.

Do you feel the fear?

OUR NEXT COURSE KICKS OFF IN LESS THAN 3 WEEKS

OUR NEXT COURSE KICKS OFF IN LESS THAN 3 WEEKSThe next edition of the How to Have an Epic Retirement Flagship Course kicks off on the 28th August. And while earlybird 25% off is now closed, we can offer a 15% discount for our Epic Retirement newsletter subscribers using the coupon code: EPICSPRING15 (or click here to purchase with the coupon code now.)

This is going to be our LARGEST COHORT EVER! That makes it even more fun to be honest! More community conversation and people to ask questions!

My 6-week How to Have an Epic Retirement Flagship Course has helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

A week for the memories.

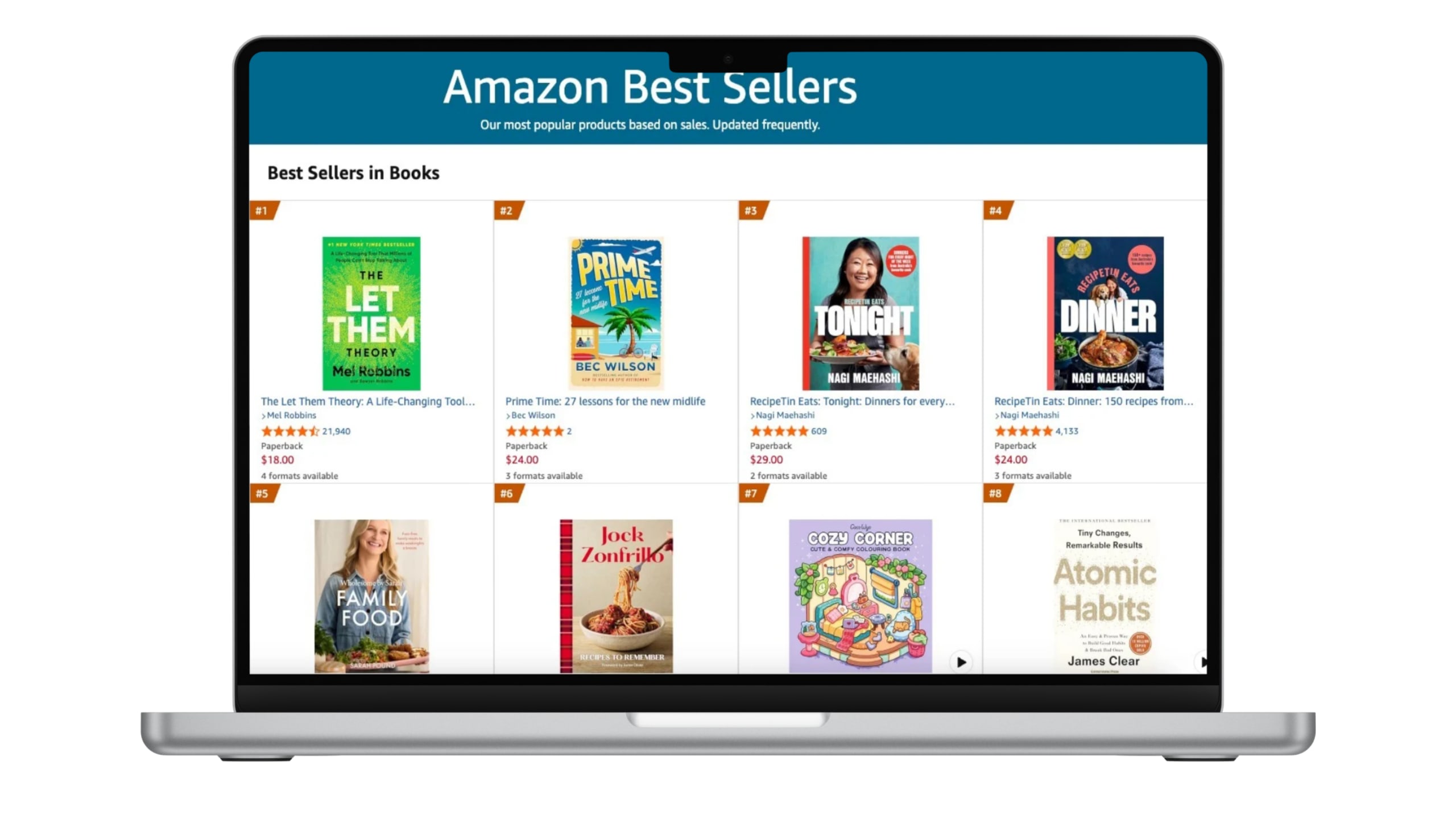

A week for the memories. If you missed the Prime Time newsletter on Thursday of this week, then I have some big news! We did it! Prime Time: 27 Lessons for the New Midlife was the #1 bestselling Aussie self help book in its first week, across all booksellers.

We’re also #4 in on the overall list of non-fiction bestsellers in the country(alongside Australia’s favourite recipe books by Nagi and Let Them by Mel Robbins - what a thrill). And we’re proudly in the top 20 bestselling books overall in the entire country this week. This is all according to this week’s official BOOKSCAN data that was out Thursday - the real insight into what people are actually buying in bookstores around the country.

Thanks to everyone for getting in and buying a copy, and spreading the word. I can’t quite believe I get to say that out loud. It’s wild - and it means so much to me.

To say thanks — and to egg you on to share your pics (because we love seeing them!) — we’ve made some fun mugs for a little competition. Entering is super easy, and you could win one.

COMPETITION - WIN A LIMITED EDITION PRIME TIME COFFEE MUG

We’re giving away ten limited edition quirky Prime Time coffee mugs - they’re funny (a little bit rude) and fabulous—we’re just putting the finishing touches on the designs now).

To enter, all you need to do is:

📸 Post a fun photo with your Prime Time book on social media - get creative!

📖 Or share your favourite quote or moment from the book

📍 Post it on your wall and/or in the Facebook group

🏷️ Use the hashtag #PRIMETIME and tag me: @becwilsonepic on Facebook or @epicretirement on Instagram

That’s it! You’ll be in the running to win, and we’ll select the winners at the end of the first month after launch.

I’ve spent the week running from wonderful radio show to wonderful radio show. (Thank you to all our radio listeners and hosts - I love talkback). The week started with Bill McDonald’s Morning Show on 4BC. Then a chat with Nic Healey on Victoria Statewide Drive. Next it was Sydney for Brekkie with Craig Reucassel; Canberra Drive with Georgia Stynes; and on Saturday was on Tom Mackenzie-Forbes ABC Brekkie in the Gold Coast; and then 6PR in Perth’s Saturday night program with Fred Mafrica. That’s a lot of talking about the Prime Time of our life. Each time there was heaps of callers - and lots of texts!

And if you haven’t grabbed your copy of the book yet, you can get it here:

👉 https://amzn.to/3UE62bk

Or see all the stockists here.

Hey and check out these terrific reviews starting to pour in (and please consider leaving one on Amazon if you bought your book there; or on Goodreads if you bought it elsewhere.)

Again - thank you! thank you! thank you! I love my job - which is really just making things for you to learn from. And it’s even more fun when you use what I make prolifically and tell your friends about them!

Now - while I have your attention - make sure you listen to this week’s podcast with Shelley Horton. It’s a ripper. She’s got so much talent that lady - she’s great to chat with. And don’t forget that you can still register for the course that kicks off on the 28th August. There’s a coupon code above for our readers.

Now go, enjoy your Sunday.

Bec x

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

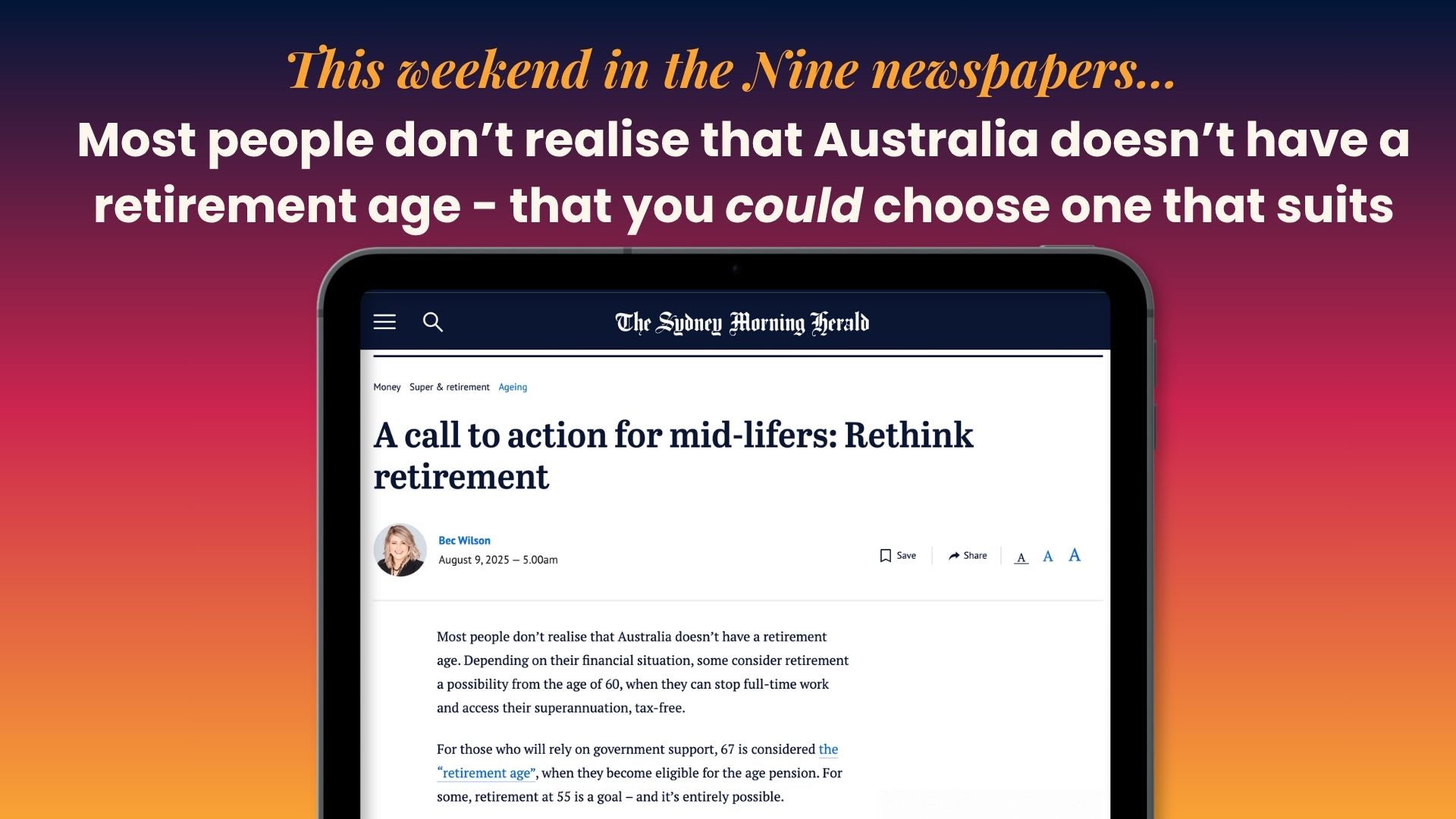

A call to action for midlifers: rethink retirement

A call to action for midlifers: rethink retirementExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 9th August 2025.

Most people don’t realise that Australia doesn’t have a retirement age. Depending on their financial situation, some consider retirement a possibility from the age of 60, when they can stop full-time work and access their superannuation, tax-free.

For those who will rely on government support, 67 is considered the “retirement age”, when they become eligible for the age pension. For some, retirement at 55 is a goal – and it’s entirely possible.

We assume we know what retirement means, thanks to more than 100 years of the concept being deeply entrenched in society. We’ve grown up with the idea it happens at a fixed age – when we can get a pension.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

Getting AHEAD of Perimenopause

Getting AHEAD of PerimenopausePerimenopause can creep in quietly, with brain fog, anxiety, insomnia or sudden mood swings, or it can hit like a freight train. If you’re in your 40s or 50s and starting to feel “off,” there’s a good chance your hormones are behind it, and it’s not just about hot flushes or missed periods.

This week on Prime Time, I’m joined by journalist, TV presenter and all-round powerhouse Shelly Horton, a familiar face on Aussie screens and now the author of I'm Your Peri Godmother: A happily-ever-after guide to kicking perimenopause in the ovaries, the first Aussie guide to perimenopause that’s raw, evidence-based and unashamedly funny.

Shelly shares how she went from media high-flyer to hormonal hot mess in the ICU, and how she clawed her way back with good doctors, better information, and plenty of honesty. We unpack what perimenopause actually is, how to manage and prevent the tougher symptoms, and why this conversation matters just as much for the men who live, work and love alongside women going through it.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

August 2, 2025

Ageism and the midlife workplace shut out

Feature: Ageism and the midlife workplace shut out

Newspapers: “We are running the race to retirement riches backward”

Podcast: Why I wrote Prime Time—and what I hope it sparks

From Bec’s Desk: #2 on the Bestseller List - and holding ground

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Prime Time is currently #2 on the Amazon Bestseller ListOrdered your copy yet? Learn more about the book on my new website www.becwilson.net.

Ageism and the midlife workplace shut out

Ageism and the midlife workplace shut outThere’s a new report from the Australian Human Rights Commission that stopped me in my tracks: a quarter of HR professionals now classify people aged 51 to 55 as ‘old’.

Old. At 51.

I nearly choked on my coffee.

That number has jumped from 10 per cent just last year. And if it’s accurate, it means a huge number of people are being quietly sidelined while they’re still in the prime of their lives - not because they’ve lost capacity or motivation, but because of an outdated story about age. As I put it in my book, they’re being measured against templates that no longer fit. And because even we, the people in this generation don’t understand the templates are broken, it’s unsurprising that younger generations and employers don’t grasp it.

For many people this age-first judgement of them is insulting. It’s wasteful. For individuals, for the economy, and for a society that claims to value experience and want high quality leadership.

The report says, even with more than half of employers reporting hard-to-fill vacancies, only 56 per cent say they’re open to hiring workers aged 50 to 64 to any real extent. That drops to 28 per cent for people over 65. And 18 per cent admit they won’t consider older candidates at all.

So we’re hearing it directly from employers: they’re less likely to hire someone over 50, not because of ability or attitude, but because of age. Then, when they do hire someone older, they report no meaningful difference in energy, creativity, adaptability or output. 🤯

These findings match what many people are experiencing once they hit their 50s - lots and lots of people are facing ageist HR departments and employers. So, if we want to keep working, and get real satisfaction from that work, we need to talk about what’s actually going on. Because this might not be a problem we can solve head-on. It might be something we need to plan around, navigate, or even step around altogether. Why bash your head against the wall creating change when you can simply change industries to one that appreciates and needs age and experience?

It’s a tough reality, and yes, it can feel personal. But naming it and pointing out the industries and companies where ageism is rife - that helps. It stops us wasting energy thinking we’ve done something wrong.

This part of midlife doesn’t get enough airtime. You’re not done. You’re not coasting. You’re not invisible. But the world might be starting to look through you anyway. And that disconnect - the gap between who you know yourself to be and what others assume based on your age - can fuel doubt, frustration, and that quiet question: what if they’re right?

We may not be able to change the system. But we can change how we respond to it.

If you’re facing this midlife workplace shut-out, don’t just wait and hope it passes. It is unlikely to in our lifetime. Instead think of these steps:

Start by getting really honest about your position, your next step on the path and your options. That means checking your skills against what’s actually being hired for - not what you used to be hired for. It means talking to people outside your usual bubble. You’ll get better, faster intel from a friend-of-a-friend in a different industry than you will from hours trawling job boards that filter you out before you’ve even hit apply.

If you're still in work but watching the writing appear on the wall, now is the time to future-proof yourself. Think about what industries actually value age and experience - health, education, training, compliance, aged care, professional services, consulting, not-for-profits, and regional leadership roles. They're not always glamorous, but they often need someone who knows how to lead, stay calm under pressure, or manage people with empathy.

And if you're already on the outer, stop pouring energy into a job market that's ignoring you. Start having conversations about what you could buy, build, or join. There are hundreds of solid, low-drama businesses changing hands every month - cafés, bookkeeping services, cleaning companies, tutoring agencies, franchises. Most of them don’t make headlines or have IPOs, but they make money and offer independence, flexibility, and meaning. That’s worth more than a perfect résumé and another round of ghosted applications.

This isn’t about chasing reinvention for the sake of it. It’s about being honest with yourself about the system you’re in, and choosing the option that gets you back in the game. Not stuck outside it, wondering what happened.

We may not be able to change the system. But we can change how we respond to it. Have you had an experience with ageism in your workplace? Or have you struggled with being shut out?

LAST DAYS OF THE EARLYBIRD 25% OFF DEAL

LAST DAYS OF THE EARLYBIRD 25% OFF DEALThe next edition of the How to Have an Epic Retirement Flagship Course kicks off on the 28th August. And we are closing the 25% off earlybird deal this week and packing our welcome packs for sending off. And I have exciting news.

This is going to be our LARGEST COHORT EVER! That makes it even more fun to be honest! More community conversation and people to ask questions!

My 6-week How to Have an Epic Retirement Flagship Course has helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

Well, at the time of writing on Saturday, Prime Time: 27 Lessons for the New Midlife is still at #2 on the overall Amazon Australia Bestseller List. That’s five days in the top ten, at least three of which were in the top two! Happy. With. That!

Thanks to everyone who has got in and bought a copy. We're kicking off a fun little competition to celebrate the launch of Prime Time the book - and launching our first ever MERCH! You’ve really inspired us with all the photos of your books going up in the group and we want to reward you with prizes. More on that below.

This week was packed with wonderful moments. The moment we got into the top ten, then watching it climb all the way to number two - I think the community was as excited as I was, messaging me, sending me photos of the rankings, cheering our new book baby on (it’s ours not mine!). Watching the excitement of our community as their books started to arrive in their mailboxes was wild - they started posting photos everywhere which really made my week.

Then, the opportunity to talk about it. Live talkback radio shows in three states on high profile programs - one with Steve Austin in ABC Brisbane Mornings. One on ABC NSW Statewide Drive with Jess and one on ABC Sydney’s breakfast on Saturday with Dom Knight.

An extract of the book published in The Age and The Sydney Morning Herald (read it here - unpaywalled). How to Revel in your new empty nest

And a Live Launch of the book on Youtube with my publisher Sophie Hamley which we packaged up into this week’s podcast so you can learn some of the things that drive the book. (below)

The book How to Have an Epic Retirement also got a bump this week and had to be rushed to reprint! Yay!

And, Nina started on our team in the Epic Retirement Institute this week too. Gosh was that great timing. We have a course about to kick off in August, and it’s about to be all-hands-on-course-delivery! It will be our biggest course cohort ever I’m excited to say!

I’m sure there’s more. But this week was a blur. (A good one).

Now, about the competition!

COMPETITION - WIN A LIMITED EDITION PRIME TIME COFFEE MUGWe’re giving away ten limited edition quirky Prime Time coffee mugs - they’re funny (a little bit rude) and fabulous—we’re just putting the finishing touches on the designs now).

To enter, all you need to do is:

📸 Post a fun photo with your Prime Time book - get creative!

📖 Or share your favourite quote or moment from the book

📍 Post it on your wall and/or in this group

🏷️ Use the hashtag #PRIMETIME and tag me:

– @becwilsonepic on Facebook or @epicretirement on Instagram

That’s it! You’ll be in the running to win, and we’ll select the winners at the end of the first month after launch.

And if you haven’t grabbed your copy of the book yet, you can get it here:

👉 https://amzn.to/3UE62bk

Or see all the stockists here.

Can’t wait to see what you come up with. We hope you’ll make it bold, cheeky, or meaningful. This is your Prime Time after all.

Now go, enjoy your Sunday. And thank you - your support is unbelievable. I’m glad you can put my work to good use!

Bec x

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

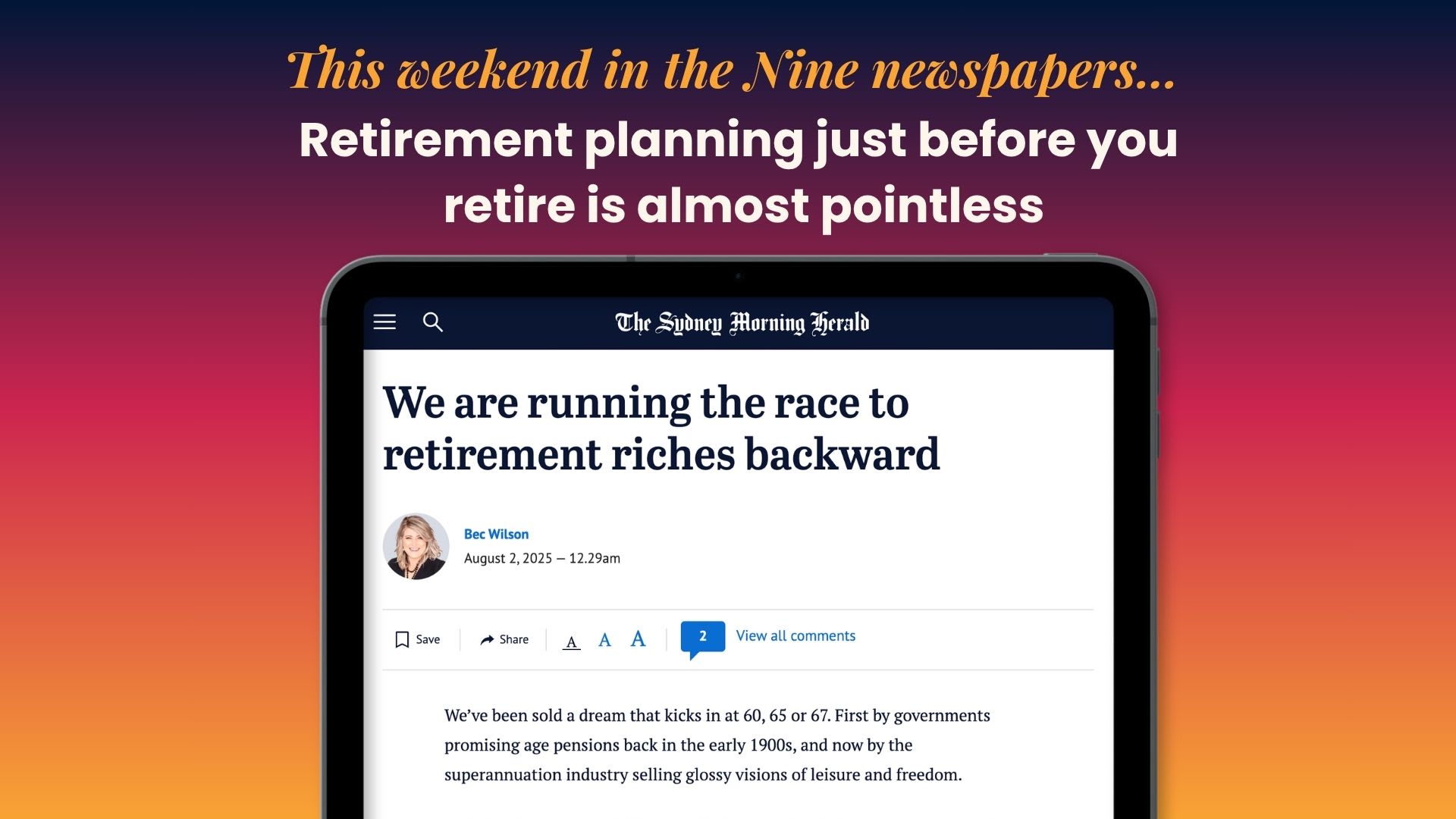

We are running the race to retirement riches backward

We are running the race to retirement riches backwardExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 3rd August 2025.

We’ve been sold a dream that kicks in at 60, 65 or 67. First by governments promising age pensions back in the early 1900s, and now by the superannuation industry selling glossy visions of leisure and freedom.

And the planning for it? That usually happens just before people stop working – often too late to reshape anything meaningful.

But for a growing number of Australians, it’s not retirement itself that shapes their future. It’s the decade or so before it. That’s the window where you still have time to make strategic decisions – about money, work, lifestyle, and how you want the next 30 years to feel.

The problem is that the word retirement still sounds like the end. It feels old. And for many people in their 50s, thinking too far ahead feels uncomfortable. They put off planning, or assume their super will take care of itself, or just hope things will work out.

But by the time they’re ready to engage, they’re often left asking, “why didn’t I know this sooner?”

The truth is, the best retirements don’t start at 65 or 67. They start in your 50s, with practical decisions that give you more flexibility and less pressure – now and later.

That might mean getting serious about salary sacrificing or topping up your super while you’re still earning well and getting it into the position where, if it compounds at a long-term return rate of 7 to 10 per cent over 15 years ahead, before you retire, that it will be “enough”. And you can even forecast that in your late 40s or 50s.

It could mean getting the mortgage under control as early as you can once the kids are (finally) off your hands. Or thinking differently about your home versus investment mix, and perhaps choosing to downsize and shift money into superannuation once the downsizing window, which so many people are unaware of, opens at the age of 55. That’s when the government allows you to put in up to $300,000 per person from the sale of your principal residence if you’ve owned it for 10 years or more.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

Why I wrote

Prime Time

—and what I hope it sparks

Why I wrote

Prime Time

—and what I hope it sparksWell, it’s here. Prime Time isn’t just a podcast anymore - it’s now a book, and on day 1, it’s a bestseller!

Yep, Prime Time: 27 Lessons for the New Midlife is officially out in the wild, and I couldn’t be more excited to bring you this behind-the-scenes episode. I’m joined by the incredible Sophie Hamley, my publisher from Hachette Australia and the woman who said yes (twice!) - first to How to Have an Epic Retirement and now to this book, which I’m calling ‘the prequel’ to an Epic Retirement. This new book is packed with all the things you’d have wished you knew earlier and put into action.

We’re digging into what this book is really about, how it came together, and why that bump so many people go through in midlife isn’t a crisis - it’s quite possibly the beginning of your prime time. If you’re anywhere between 47 and 70, still working, still juggling, still trying to figure out what the hell comes next… this is your episode.

It’s a casual, personal conversation. We actually recorded it as a ‘Prime Time live’ on launch day on Youtube —Wednesday 30 July — with all the anticipation and buzz that comes from two people who’ve poured so much into something and are finally watching it land. It’s real, it’s reflective, and it’s a bit of a celebration too. So have a listen, order a copy, and make YOUR Prime Time count.

We actually recorded this podcast LIVE on Youtube. It was a hoot! Watch here.

We actually recorded this podcast LIVE on Youtube. It was a hoot! Watch here.LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

July 31, 2025

Almost there… can we hit #1 on Amazon today?

Hey friends! Bec here.

Something wild has happened. Prime Time: 27 Lessons for the New Midlife has climbed all the way to #2 on Amazon - and not just in a category, but #2 overall on the Amazon Bestseller List.

That’s right. We’re sitting just behind the top spot in all of Amazon. And with your help, we might just tip it over the edge today.

But I seriously need your help.

If you’ve been thinking about grabbing a copy, now’s the perfect moment. Or you might want to gift one to someone navigating midlife with big dreams, challenges, financial goals, questions, or new beginnings.

Every single order today counts - especially in the next few hours. You can even grab the Kindle edition to send straight to your device (or someone else’s).

👉 Click here to buy the book on Amazon - today matters

If you already have it and love it — thank you. You can still help by:

Sending this email to a friend who’d love the book

Gifting a Kindle copy (it’s easy!)

Sharing the link on your socials with a “let’s help Bec hit #1!” vibe

And if we make it? You’ll be the first to hear about it. And I’ll absolutely cry.

Thank you for being part of this. Let’s make some Prime Times count!

With so much gratitude,

Here’s that Amazon link again! This time as a button!

PS - Thanks!

Prime Time: 27 Lessons for the New Midlife

Prime Time: 27 Lessons for the New MidlifeFeel like you’re turning the corner into a new stage of life? It might just be your Prime Time.

From bestselling author and podcast host Bec Wilson comes Prime Time: 27 Lessons for the New Midlife—a practical, inspiring guide for making the most of the powerful years from your late 40s through your 70s.

This isn’t about winding down. It’s about stepping up. In 27 punchy, practical lessons, Bec tackles everything from money and superannuation to work, purpose, health, happiness, family and travel. You’ll learn how to invest with confidence, build flexible income streams, and make the most of tax concessions. But this book goes far beyond the financials—because your Prime Time is about curiosity, meaning and momentum.

Whether you’re reshaping your career, preparing for semi-retirement, chasing long-postponed dreams or just ready to prioritise you, this book is your playbook. It’s for anyone who doesn’t want to wait for retirement to start living the life they know they’re ready to really enjoy.

Midlife is no longer the beginning of the end. With the right moves, it’s the start of something truly epic.

This is your Prime Time. Make it count.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

July 26, 2025

Can ChatGPT help you plan your retirement for free?

Feature: Can ChatGPT help you plan your retirement for free?

Newspapers: “To stop retirees going mad super funds must agree of on these three things”

Podcast: Take the plunge into solo travel with Fiona Dalton

From Bec’s Desk: Come on the journey

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

My new book arrives in stores this week.I can’t quite believe it — Prime Time: 27 Lessons for the New Midlife hits the shelves in just three days.

If you’ve ever thought, “Surely life can get better from here, and I don’t have to wait for retirement’ this book is for you. It’s packed with the good stuff: easy-to-understand financial lessons; real talk about work, purpose and happiness; practical steps you can take, and a whole lot of encouragement.

If you haven’t ordered your copy yet, now’s the perfect time. Pre-orders really help get the book into more hands by starting the sales off with a bang (and hopefully seeing it hit the bestseller lists). I’d be so grateful if you grabbed yours.

Can ChatGPT help you plan your retirement for free?

Can ChatGPT help you plan your retirement for free? I, like most people, have been using ChatGPT more and more lately - to help with, well… just about everything.

When my dog got really sick and I realised the vet was Googling treatments in front of me (while charging by the 15-minute block), I turned to ChatGPT. It helped me track his recovery and manage his rehab, step by step. And it was terrific where my vet left me hanging.

On my trip, I used ChatGPT to set our daily travel plans, and guide us on the things to do and she learnt quickly I hate crowded Eurosummer beaches packed with expensive sunloungers and redirected us to nice free and peaceful places instead.

Then, when I got back from holidays recently and wanted to up my game at the gym, I asked it to write me a program to build muscle and burn off the pasta and gelato. It nailed it.

It’s not always spot-on the first time - but ask the right questions and it gets sharper quite quickly.

So I thought - why not help you try it with retirement planning?

Not to replace good advice, but to build understanding, boost confidence, and help you learn faster. Because if you’ve ever felt in the dark about super, retirement income, or what life after work, or in your Prime Time might look like - this might just be your shortcut to getting yourself some more clarity.

So today I want to share with you three great prompts you might want to try, and how it answered the first one for Jess (a person I made up) who’s 54 right now, earns $90,000 per year and has $300,000 in super.

Prompt 1: Is Jess on track to retire at 67?“Jess is 54 with $300,000 in super and earn $90,000 a year and plans to keep working full-time until 67. She salary sacrifices $100 a week into super. Estimate how much she might have in super by retirement, and what income that could give her, assuming 7.5% returns and 0.8% fees. Show the income in today’s dollars and include if I’d likely qualify for the Age Pension.”

Here’s what ChatGPT came back with:

“Estimated super at 67: ~$1,005,800

Annual retirement income (assuming 5% drawdown): ~$50,290

Likely Age Pension eligibility: Nil – her assets would be too high to qualify at first

Total annual income (in today’s dollars): ~$50,290

What this tells us: Jess is tracking well—especially considering many Australians enter retirement with far less. That $1 million balance gives her a decent base to draw from, and she may become eligible for a part pension later on as her balance reduces over time.

But beware: This is a straight-line projection. Life rarely goes in a straight line. So if Jess wants to explore part-time work in her early 60s, or a bigger travel budget for her first decade of retirement, she’ll want to model that too (and Prompts 2 and 3 can help).”

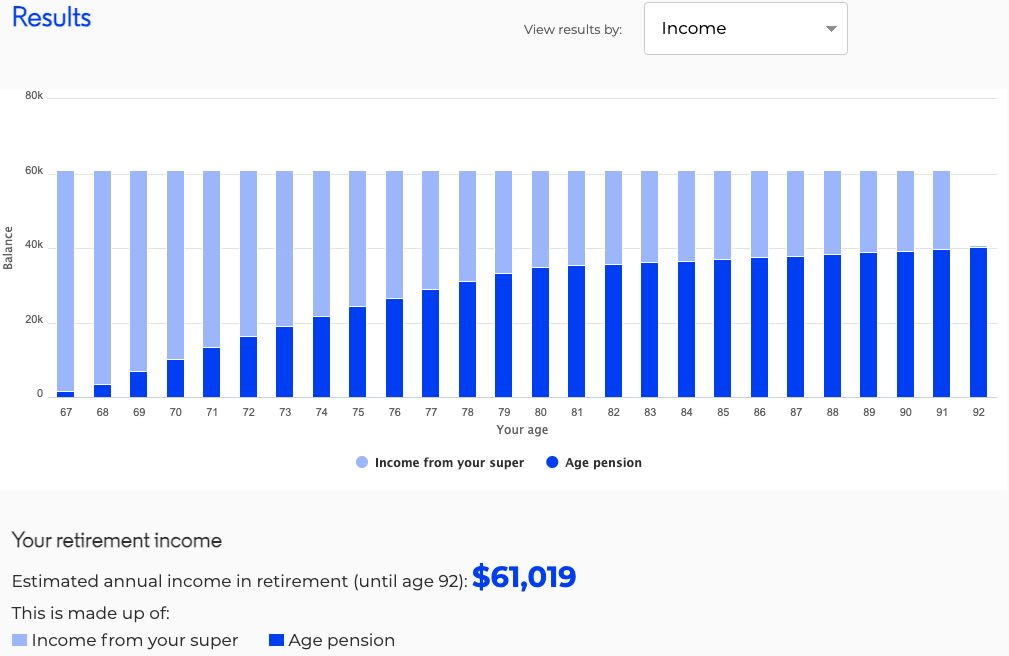

Checking the resultTo check how the AI result compared, I ran the same metrics through the MoneySmart Retirement Planner. And this was the result:

Estimated annual income in retirement (until age 92): $61,019

Estimated super balance at retirement: $638,876

In contrast, the Moneysmart calculator, which also uses a 7.5% investment return before retirement, shows that Jess would qualify for a part pension on retirement. So - who do you believe?

Bec’s note:

Bec’s note: I wanted to test how helpful ChatGPT really is when it comes to retirement planning. This was a simple, sensible prompt for Jess and it gave me a very clean, very confident answer. But then I ran the same scenario through the government’s MoneySmart Retirement Planner — and the results were… different.

The AI projected a $50,290 income in today’s dollars, based on drawing down 5% of her super annually, and said she wouldn’t qualify for the Age Pension at first. The Moneysmart tool showed an annual income of $61,019 and suggested she’d be eligible for a small part pension straight away.

Who’s right?

Well, both are using similar assumptions — like a 7.5% return before retirement — but they’re calculating differently. The AI used a flat drawdown model. Moneysmart models pension eligibility more accurately and adjusts for inflation over time.

The takeaway? ChatGPT is great at simplifying complex ideas, giving you a quick feel for how things might pan out. But it's not a full financial modelling tool. The magic really happens when you start asking smarter follow-up questions like:

“What happens if Jess goes part-time at 60?”

“When exactly would she become eligible for the pension?”

“How long would that income last if she lives to 95?”

I love it as a tool for learning and building financial confidence — but not for final decisions. That’s why I think playing with it is so valuable. You get clearer, faster, and more curious about your future.

Ready to try your own? Here are two more prompts worth playing with — and the results are fascinating. (No room in this newsletter for all the juicy detail… but you’ll see why it’s worth a go.)

Prompt 2: Can I go part-time at 60?“If I want to go part-time at 60 and work 3 days a week earning $55,000, what super balance would I need by then to top up my income and still retire at 67 comfortably? Assume I’d like to maintain a total income of around $65,000 per year. Suggest a plan from now to 60 to make that happen.”

Then, I thought I’d get clever and bring in some of my very new Prime Time thinking.

Prompt 3: Give me a staged life plan for my Prime Time yearsMy verdict?“Create a staged life plan for me from 54 to 70. Include goals and priorities for money, work, health and lifestyle. I don’t just want a retirement plan; I want a clear picture of how to make the most of these next 15 years, including when to travel more, when to shift work hours to part time, and how to stay financially confident.”

AI is shaping up to be an incredible tool for experimenting, sense-checking your plans, and building confidence in the dark. And let’s be honest — it’s a lot easier than wrestling with Excel, and it’s far better at explaining things clearly. It’s not always right, and it doesn’t always give you the detail until you dig for it — but if you know that, you’ll be cautious.

Will it replace what I do? I really hope not — unless it develops a personality, a decent sense of humour, and the ability to make super and retirement feel easy to understand. (In which case, I may need to start podcasting from a cave. 😉) What it might do is help streamline the advice industry’s workloads - and that’s not a bad thing.

In the meantime — I’ll keep writing books if you keep reading them and making courses if you keep attending. Deal?

It’s back! The Epic Retirement Flagship Course kicks off this August — and Earlybird is going to end this week🔥If you’ve been thinking about getting serious about your epic retirement, time’s almost up to get 25% off. My 6-week How to Have an Epic Retirement Flagship Course has already helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

🎟️ Earlybird spots are still 25% off. But we’ll be closing off the deal this week.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

I’m home — back from the Prime Time holiday of my dreams. And I’ve hit the ground running - fast.

First stop: Sydney, where I sat on the couch on the Today Show and talked about the book (nervewracking but I think I did a good job). And then I headed to my publisher’s office and signed hundreds of books for Booktopia’s presales orders.

After that, it was up to Noosa to launch Prime Time with a beautiful luncheon over the water at the Noosa Alive Festival. And finally, back to Brisbane just in time to appear on 7Sunrise on Saturday morning. In between there was a chat with Jess on ABC Radio’s NSW Drive show too 😁.

Somewhere in there I also refit my home office into a new filming studio for courses and videos — and tomorrow, Nina (A wonderful woman I’ve worked with for years in another role) joins the Epic Retirement Institute team as our first official permanent team member.

It’s all happening. We’ve got hundreds registered for the upcoming Epic Retirement Flagship Course kicking off on the 28th August and we’re about to shut the Earlybird 25% off and start packing the welcome packs for mailing.

—

And then there’s the big one…. Prime Time: 27 Lessons for the New Midlife lands in stores in just three days. I’m a wee bit excited. (Presales are SO GOOD! I’m honestly humbled).

It’s a book for anyone in their 40s, 50s or 60s who’s ready to stop coasting and start shaping this next chapter — with more clarity, more confidence, and more choice.

If you haven’t already grabbed your copy, now’s the time to pre-order. It means the world to me — and it really helps the book hit the ground running when it launches.

This book is the heart of everything I’ve learned and shared over the past few years. I can’t wait to get it into your hands.

—

Lastly, I’m excited to hold my own first ever free online event. It’s a book launch for Prime Time:27 Lessons for the New Midlife. My wonderful publisher from Hachette, Sophie Hamley will be joining me live online to chat about the book with you - because we both know it intimately and none of you will have seen it. All the details and the free registration link is below! And we’re hosting it on the day the book hits stores — a free lunch and learn! I’ll send out the link to everyone registered this week.

Now go, enjoy your Sunday. And thank you — for everything you consume that I do.

Bec x

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Register here for the Prime Time: 27 Lessons for the New Midlife live online book launch on Wednesday.

To stop retirees going mad, super funds must agree on these three things

To stop retirees going mad, super funds must agree on these three things

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 27th July 2025.

Here’s a fun game to play in your last month of work. Log into your super fund and try to find the form to start your retirement income. Now guess what it’s called.

Is it a pension account? A retirement income stream? A “choice income” option? Flexi pension? Super income stream? Or something else that sounds suspiciously like a branding brainstorm that got out of hand?

If you’re confused, congratulations. You’re really normal.

Super funds have spent the past two decades reminding us to save for retirement, making it easy and almost doing the job for us. But when we get to the business end of retirement, where we’re finally ready to spend our super, there’s suddenly a lot to figure out.

It’s at this point that they serve up a jargon soup which makes little sense to anyone outside the finance department, made more confusing because a lot of the terms cross over with language that is used to describe government payments.

Some funds call your retirement account a pension, but you associate the word pension with social security. Some call it an income stream, which makes more sense – if you’ve spoken to an adviser. If not, it’s just a new concept altogether.

What we need is a superannuation dictionary for retirement.

Others go with “income”, just to be vague. A few try to be cute and use all three, switching between “pension” and “income” and even adding in the wider term “account-based pension” just as you’ve finally worked out what the first one meant.

The only thing they seem to agree on is that none of them should use the same words as each other, or, helpfully, as the government.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

Solo travel has exploded in popularity - especially among women over 50. But if the words “solo travel” still conjure images of dining alone with a sad sandwich or battling awkward silence in a hotel room for one… this episode will change that.

I’m joined by veteran travel industry leader, sabbatical queen, and travel podcast host Fiona Dalton, who’s here to bust myths, drop brilliant tips, and make the case for why solo travel might just be the greatest gift you can give yourself in your Prime Time. Fiona is an experienced solo traveller herself - and tells some great home truths you can learn from.

We cover everything from travel formats and solo supplements to those weirdly intimidating solo dinners - and Fiona shares her own inspiring stories from biking NZ to driving Scotland to road-tripping the fjords of Norway.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

July 12, 2025

Timing and choices

Feature: Timing and choices

Newspapers: “These three phases define modern retirement. Which one are you in?”

Podcast: Starting your Prime Time with very little: An honest conversation

From Bec’s Desk: Tuscany… without the kids

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

A little chat about timing and choicesThis week, my article in The Age and The Sydney Morning Herald lays out how to stage your midlife using the phases I explain in my new book, Prime Time. It’s one I really want you to read. Please. It’s short, it’s sharp, and it’s not behind a paywall—just a simple sign-in gate. You can read it here.

Then I want you to read the comments. (they are full of messages from people who didn’t get to choose but instead had retirement forced on them).

There’s only a few, but they’re real. And they’re honest. Even for those of you who currently feel invincible or irreplaceable.

I wish I could reply to them directly, but I’m in Italy, and the newspaper’s commenting system won’t let me post. So, let me say it here instead - because I have a few passionate things to add. And these are things I cover in the book.

The truth is: the three stages of Prime Time aren’t available to everyone. But they can be. It all depends on when you go through your setup phase. If you haven’t done that work, you probably haven’t stopped to think about what needs to be in place to live well in your middle and later years. You might not have considered your super; nor contemplated whether your career will age well - or if it’ll support you if you want to slow down, shift gears, or work part-time. And by the time you do think about both… it might be too late to make meaningful change.

I know it sounds idyllic to choose your own path into midlife and retirement. But the hard truth is, most people don’t get that choice. Only 31% of Australians retire on their own terms. The rest are pushed—by redundancy, illness, or the needs of someone they love.

And that is exactly why I’m doing this work with Prime Time—to help you grab the steering wheel before something else does. To help you see that you can shape your next chapter, but you need to start early. Because if you don’t take charge during the setup phase, there’s every chance the lifestyle phase and the part-time years will be taken out of your hands. And then, having an epic retirement can feel harder.

In the book, I go deep on this. In the article, I only had 800 words—and one of the commenters rightly pointed out what didn’t fit in.

So go read it. Read the article, read the comments, and ask yourself:

Do I want to be part of the 31% who get to choose? OR Could we make that 31% into 50 or 60% with better planning.

Prime Time: 27 Lessons for the New Midlife lands in Australia on 30 July. It’s for everyone who wants to shape their second half—before someone else does it for them.

I’m off now to make my Prime Time count. If you can relate to the three stages share it with everyone today. We ARE reading the comments.

It’s back! The Epic Retirement Flagship Course kicks off this August — and Earlybird is still running🔥If you’ve been thinking about getting serious (but not boring-serious) about your next chapter, now’s the time. My 6-week How to Have an Epic Retirement Flagship Course has already helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

🎟️ Earlybird spots are now open - and they’re 25% off.

They won’t last long, and once they’re gone, they’re gone. So if this is your season, jump in now and lock it in at the best price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

Even shorter than last week. It’s Saturday, I’m in Tuscany with my hubby. It’s B-E-A-U-T-I-F-U-L. We sent the kids home yesterday for school and uni and doggy daycare. This week is for us, adventuring through wineries, villages, climbing duomos and having time to mull over cheese and proscuitto platters slowly.

I’ll be back in a week. Then we’ll close the earlybird on the course, and we’ll launch this new book in stores all over the country and we’ll get out there and have some fun talking about Prime Time.

In the meantime — have a listen to the wonderful podcast below; read my Sydney Morning Herald column and smile at your progress to becoming a Prime Timer or Epic Retiree.

I have one big callout this week to add.. big news.

Our Epic Retirement Club just flew past 500,000 members worldwide. OMG. Half a million people! What a brilliant community of learners and contributors we’ve built together there — just brilliant.

And get this - it now reaches somewhere around 50 million people a month across the internet. Fifty million! 😎 Pretty cool, huh? (No, you can’t advertise in it. It’s strictly for learning and growing people’s retirement confidence. No sneaky promos, either - we ban anyone who tries.)

A massive shoutout to our amazing 18 volunteer moderators who keep the space thoughtful, safe, and purposeful. They’re the reason it works so well.

We don’t allow financial advice or self-promotion in the group. It’s a confidence-building, peer-to-peer learning space, and one of the most positive corners of the internet for anyone navigating midlife, retirement, or beyond.

And, one last thing. I’m excited to hold my own first ever free online event. It’s a book launch for Prime Time:27 Lessons for the New Midlife. My wonderful publisher from Hachette, Sophie Hamley will be joining me live online to chat about the book with you - because we both know it intimately and none of you will have seen it. All the details and the free registration link is below! And we’re hosting it on the day the book hits stores — a free lunch and learn! I’ll send out the link to everyone registered when I get back and set the tech up!

Now go, enjoy your Sunday.

Bec x

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Prime Time: Live Book Launch Event

Prime Time: Live Book Launch EventOK, we’re doing it. I’m holding a free live online event for the book launch on launch day… and my publisher from Hachette, Sophie Hamley, will be my cohost. If you’d like to attend, please register your interest below. It’s a free event, and I’ll do my best to pack it with valuable information.

Register here for the Prime Time: 27 Lessons for the New Midlife live online book launch.

These three phases define modern retirement. Which one are you in?

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 13th July 2025.

We used to think about life in two financial stages: work and retirement. You worked full-time, saved what you could, and then one day you stopped and lived frugally on whatever you’d accumulated.

That model is out of date. And thank goodness.

What’s replacing it is a more layered, flexible and human approach. For many of us, the 50s, 60s and even 70s are no longer a single long descent into retirement. They’re a new season of earning, spending, planning and evolving. And money plays a different role in each phase.

From my work with hundreds of thousands of Australians, I see three emerging phases that most people experience in midlife and the lead-up to retirement: the Setup Phase, the Lifestyling Phase, and the Part-timing Phase. And I want us to understand all three.

Each one has different financial dynamics. Each one comes with both opportunity and risk. And you don’t always get to experience all of them – especially if money is tight – but with some planning, and the growth of superannuation that we’re getting today, more and more people can.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

If you’re in your 40s or 50s and starting to quietly panic about retirement, you’re not alone—and you’re not too late. In this raw and refreshingly honest episode, I chat with Mary, a single mum and media professional who’s spent her working life juggling freelancing, kids, and surviving. Now, at 47, she’s finally stopped ignoring “the big dark thing in the corner” (her money) and is facing her financial future head-on.

Mary doesn’t hold back. We talk about the fear of being old and broke, the realities of patchy super, and the moment she decided it was time to rip the Band-Aid off and take control.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:July 5, 2025

What is a Prime Timer?

Feature: What is a Prime Timer?

Newspapers: “The major retirement planning question we’re all getting wrong”

Podcast: Living a 'soft retirement' and test driving jobs

From Bec’s Desk: We’re having a book launch online event!

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

What is a Prime Timer?This week in the Epic Retirement Facebook Group many of you asked me to answer a big question 'What is a Prime Timer?'

In short — I’m a Prime Timer. And I think many of you are actually Prime Timers and that's possibly something you can associate with and start doing and being BEFORE you retire.

I’m nearly 50 now, but at 47 and a half, I hit a turning point. I burned out. I’d been in a high-visibility career, meeting goals that I thought were important, in a system I’d once found exciting but that no longer made sense for me. I didn’t have time to make a grand plan. As it happened, I just was put in a position where I had to stop. Cold. Yes it was somewhat my choice -- but not really. You know how that is, when the other options are even less appealing right. And from that point, I had to rebuild everything from scratch: income, purpose, identity. It wasn’t graceful. It certainly wasn’t pretty. But it was one of the most important turning points in my life.

Back then, my work was my purpose. I was constantly switched on, overperforming at work but underinvesting in everything else - my health, my interests, my fun. I was tired, stressed, and chasing someone else’s idea of success. And I hadn’t even paused to ask if it was what I wanted because before this stage of life frankly, you're often just juggling life and responsibilities (particularly with 3 kids).

Stopping was terrifying. But because I had a little bit of courage, I went exploring. I tried new things. I figured out what I liked again - and started to think about the kind of life I actually wanted to live next. And yes - one of the first projects I decided on was to write How to Have an Epic Retirement. And I decided in that process I wanted to do more around the second half of life.

So then I began researching the second half of life for that first book, and in doing so I came across something fascinating: the science shows many of us go through a dip in happiness between about 47.5 and 55. For some, it leads to growth. For others, the change comes whether you’re ready or not — and it can be really confronting. And either way it drives us to make choices, choices we have the ability to make for ourselves earlier rather than at retirement.

So here’s the shift I see now. So many of us in our late 40s, 50s and 60s are (or could be) approaching life differently. We’re not ready to retire - or even talk about retirement, really - but we are ready for some of the benefits that used to be reserved for it: flexibility, breathing space, joy.

We want financial confidence so we can do life on our terms. We want meaning, experiences, and a chance to reconnect with ourselves — beyond the years of raising kids, juggling mortgages, and keeping everything afloat.

So I’m opening the door to a conversation about a new life stage – one that comes after ‘adulting’ and before ‘retirement’. I selfishly call it my Prime Time. And I feel like it can be.

I think that for many of us, our Prime Time begins when the kids get their drivers licence, the mortgage starts to look conquerable, and we get a bit more time and money in our wallets as the kids start to become more and more independent. That’s when we start to ask: What do I actually want next? What lights me up now?

And the truth is, we’re in a unique position. We’ve been contributing to super for decades. We’ve got compounding on our side (if we learn how it works). We’ve got life experience, perspective, and - thanks to much longer life expectancies -we’ve got time. And all of that gives us something no previous generation has had at this stage of life: choices.

That’s why I started talking about Prime Time. Because I think it’s a new stage of life and I think many people here looking at retirement as the solution are actually in your Prime Time and you could embrace it.

There’s three phases of life within your Prime Time in my opinion (and I talk about them in my next book).

Your Setup Phase: The period where you get in control of your money, interests and passions. You work out how much is enough, and you get yourself on the path to real fiinancial confidence.

Your Lifestyling Phase: The period while you are working full time where you flex thing a bit more in your direction – finding joy, taking longer holidays, getting healthy and enjoying life AND work. You might need to change what you do to find that balance or maybe you just need to self-invest more.

And your Part Timing Phase: I don’t think we need to retire to get the benefits of a part time lifestyle. And I think future generations, starting with ours are priving that work, if you do something you enjoy can be good to continue with as you enjoy your lifestyle. So I’m calling this! I think our Part Timing phase is the absolute bomb!

And so, that’s a simple snapshot of a Prime Timer. Ultimately, I’m a Prime Timer. I think many many of you are here too. And I have written a book to help you and me on our journey. I think there’s 27 lessons that can help us – but they’re for another day.

Prime Time: 27 Lessons for the New Midlife is indeed the name of my new book, which will come out in Australia on the 30th July.

I’m off now to make my Prime Time count. If you think you might be a Prime Timer - tell me about it. What are you doing to make this stage of your life count. Do you feel like you have to wait for retirement to do that - or are you finding little ways now?

We're all in this together. Making it count. Making it epic. Whatever your path -- make sure you get to choose it.

It’s back! The Epic Retirement Flagship Course kicks off this August — and Earlybird is officially ON 🔥If you’ve been thinking about getting serious (but not boring-serious) about your next chapter, now’s the time. My 6-week How to Have an Epic Retirement Flagship Course has already helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

🎟️ Earlybird spots are now open - and they’re 25% off.

They won’t last long, and once they’re gone, they’re gone. So if this is your season, jump in now and lock it in at the best price.