Benjamin Tan's Blog

May 5, 2026

Trupanion: Recovery Is Real, and the Story Is Narrower Now

Trupanion’s () latest quarter (Q1 2026) did not change the story so much as clarify it. This is no longer the old hypergrowth pet insurance darling that could do no wrong. It is a more mature, more disciplined business rebuilding credibility through better pricing, stronger margins, and steadier execution. That is a less glamorous story, but a more investable one.

Q1 2026 Numbers: SummaryThe headline numbers were solid. Q1 2026 revenue rose 12% to $384m, while subscription revenue grew 16% to $269.5m. Net income came in at $4.9m versus a loss a year ago, and adjusted EBITDA improved to $17.4m from $12.2m. Cash and short-term investments ended the quarter at $383.7m against total debt of about $109m, so balance sheet risk remains low.

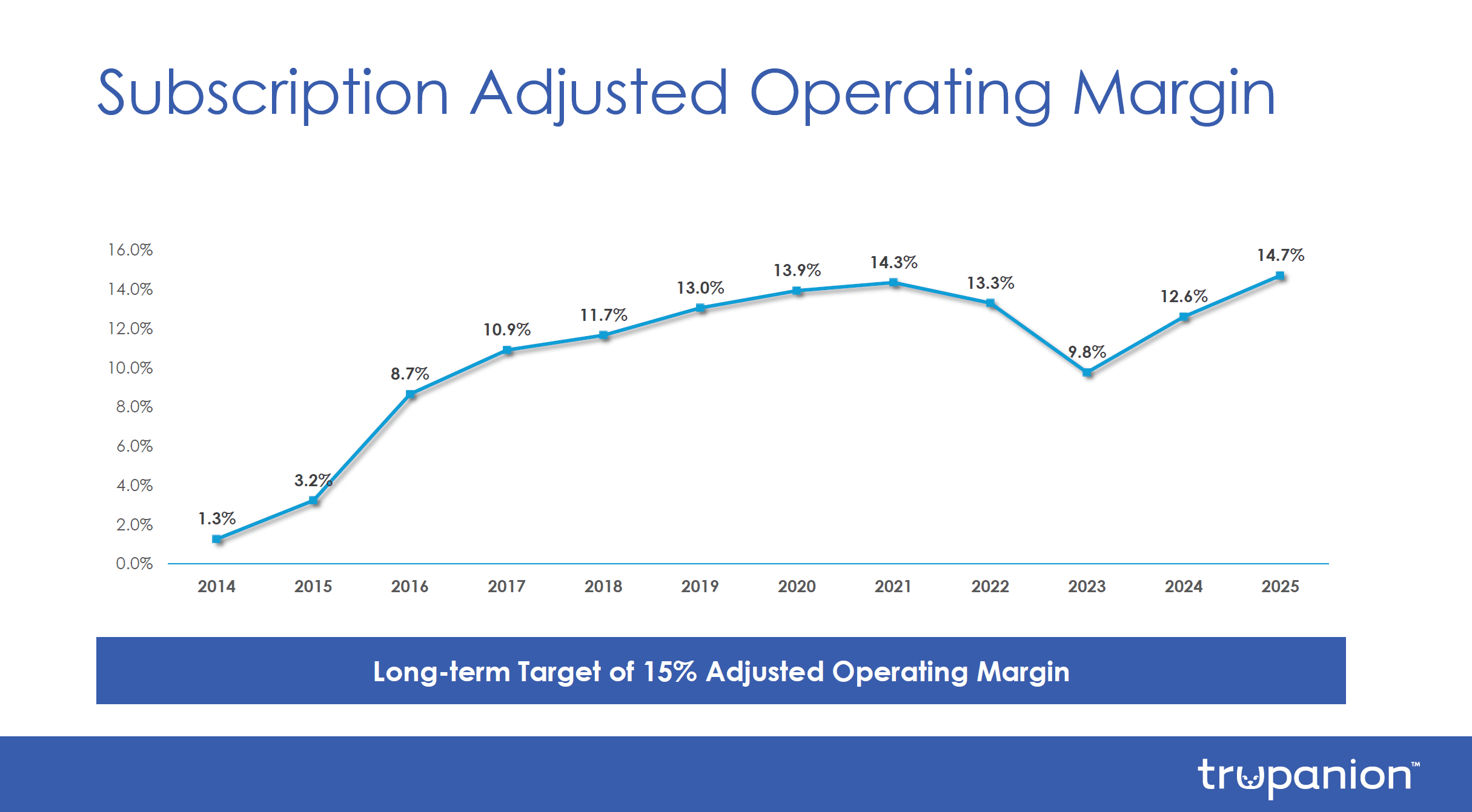

The real signal, though, is inside the subscription business. Subscription adjusted operating income rose 28% to $38.4m, and subscription adjusted operating margin reached 14.2%, up from 12.9% a year ago and the highest Q1 margin in company history. The subscription cost of paying veterinary invoices improved to 70.8% of subscription revenue from 71.8%, while fixed expenses fell to 5.8% of revenue from 6.2%. In plain English, pricing is catching up, and the operating model is scaling again.

Healthy Growth and Reacceleration of Core BusinessGrowth is not pristine, but it is healthy where it matters. Subscription pets increased 5% year over year to 1.106m, average monthly revenue per pet rose 11% to $85.79, and retention improved slightly to 98.35%. Pet acquisition cost rose to $315 from $267, so growth is not free, but management is still investing from a position of strength, not desperation.

The weak spot remains the non-core business. Total enrolled pets actually declined 2% year over year, and management expects growth in the other business segment to continue decelerating as it stops enrolling new pets in most U.S. states for its largest partner. That reinforces the right lens for analyzing : focus on the subscription business and treat the rest as runoff.

Takeaway: Staying Invested and InterestedMy takeaway is straightforward. The core business looks intact. Margins are improving. Growth is slower than it was in the glory days, but not broken. At this point, the thesis is no longer about dreaming on optionality. It is about underwriting a niche insurer that can still grow subscription revenue around the mid-teens while keeping pricing disciplined and returns attractive. That is enough for me to stay interested via a small stake that was further increased in Q1 2026 in my Traditional IRA.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. It examines how personality biases unconsciously influence investing behaviors. Learn more at my author page or order the book on Amazon. Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.

April 1, 2026

Most Investing Mistakes Are Not Analytical

Over time, I have come to realize that many of the biggest mistakes investors make—myself included—are not analytical. They are behavioral. They come from misalignment between who we are and how we invest.

Some people freeze, waiting for the “perfect” entry point.

Some overtrade, chasing momentum and narratives.

Some hold on too long, anchored to past decisions.

These are not failures of intelligence. They are patterns. And those patterns are often rooted in personality.

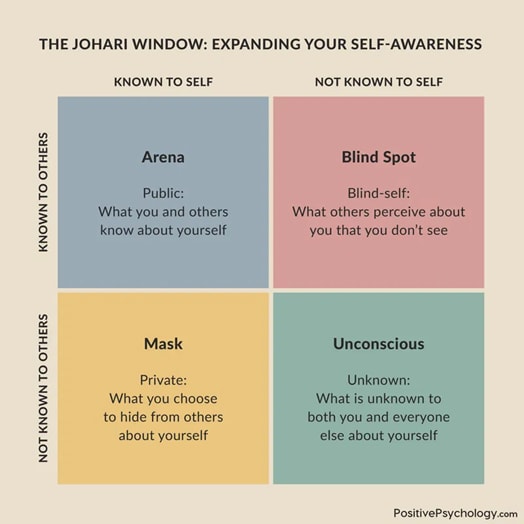

The Role of Self-AwarenessOne useful way to think about this is through the lens of the Johari Window.

The framework divides self-awareness into four quadrants: what is known to self and others (“Arena”), what is hidden (“Mask”), what is blind (“Blind Spot”), and what is unknown (“Unconscious”). In investing, many costly mistakes sit in the Blind Spot quadrant—patterns that others may observe, but that we do not fully recognize in ourselves.

This is where self-awareness becomes practical, not abstract. The goal is not to eliminate bias entirely, but to surface it early enough to manage it.

Source: Positive Psychology.comHow My Own Approach Evolved

Source: Positive Psychology.comHow My Own Approach EvolvedThis idea of correlating self-awareness with personal investing did not come to me all at once.

My own investing journey started from a more traditional place. I was trained in finance, spent years in banking, and initially approached investing through the lens of valuation and discipline. Over time, that framework evolved. Not because it was wrong, but because it was incomplete.

What changed was not just what I invested in, but how I understood myself as an investor.

The shift from value to growth was not purely intellectual. It reflected a broader evolution in how I think about risk, conviction, and time horizon. And in hindsight, personality played a larger role in that evolution than I initially recognized.

A Different Way to Think About Portfolio StrategyMy personal journey became the foundation of my book, Suit Yourself: A Portfolio Strategy for Every Personality Type:

Published by Koehler Books

Published by Koehler BooksThe premise is simple: There is no one-size-fits-all investing strategy.

A portfolio that works for one person may fail for another, not because the idea is flawed, but because it does not fit how that person actually thinks and behaves.

In the book, I explore this through the Enneagram framework, using storytelling and pop culture to make the concepts more accessible. The goal is not to prescribe what to buy, but to help readers understand how their own tendencies shape their decisions.

At its core, the book focuses on three things:

Why investors sabotage themselves

How personality shapes investment decisions

How to align portfolios with identity

Lowering the Barrier to EntryOne piece of feedback I received recently stood out. A reader told me that the ideas only fully clicked once they started reading the book.

That was useful to hear. It is suggested that the biggest barrier is not disagreement, but entry.

Read the Preview ChaptersSo I decided to remove that barrier.

I have shared two chapters of the book on my website. These include the introduction and a chapter on my own investing journey, where I discuss how my philosophy evolved and how personality influenced that process.

If you are curious about how psychology intersects with investing, you can read the preview here.

The Real Risk in InvestingWhether or not you decide to read further, the core idea is worth considering: Investing is not just about finding the right opportunities. It is about understanding the person making the decisions.

And that person is you.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. It examines how personality biases unconsciously influence investing behaviors. Learn more at my author page or order the book on Amazon. Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.March 2, 2026

Trupanion: Mispriced Coverage

The pet insurance category is underpenetrated; Trupanion’s margins are normalizing. Yet, the current valuation reflects neither.

The pet insurance category is underpenetrated; Trupanion’s margins are normalizing. Yet, the current valuation reflects neither.If you have read my book Suit Yourself, you will know that Enneagram Type Fives gravitate toward the complex and the niche. We like businesses that require spreadsheets, transcripts, and patience. We prefer the intellectual challenge of finding obscure stocks, and that is exactly our pitfall—overthinking rather than keeping it simple, like buying the S&P 500 or investing in a large-cap stock. And we are often attracted to underdogs that the market has quietly dismissed because we have an intellectual urge to prove the market wrong.

Trupanion fits that mold exactly, so this may be my psychological trap. I am aware that my personal biases may be at play here, unconsciously nudging me to look for evidence to support my preconceived thesis about this puppy. I am therefore writing up this analysis to lean more into objectivity and further away from the unconscious pull that may be driving my conviction. I am also capping my exposure by staying within the capital limits of my Traditional IRA and not extending it to my larger trading account.

Taking my own medicine here.

Trupanion: Capital Discipline Interrupted by Temporary Margin CollapsePet insurance is a niche sector, and insurance math is complicated. Trupanion management talks about targeting an internal rate of return of 30-40% on pet acquisitions, rather than adjusted EBITDA theatrics. That combination made Trupanion the kind of small, esoteric stock that rewarded deep work for a number of years at the height of its growth during COVID.

Strip away the noise in the last few years, and one can see that Trupanion’s business structure remains intact. Trupanion operates a cost-plus model: approximately 70% of subscription revenue is paid to veterinarians. The company targets a long-term, subscription-adjusted operating margin of about 15%. Excess capital is invested in pet acquisitions only if the projected internal rates of return are between 30% and 40%. This is not a traditional insurance approach; it aligns more with disciplined capital allocation within a subscription model. The margin drop in 2022–2023 was not a failure in strategy; it was due to pricing lag. Veterinary costs rose faster than premiums could be adjusted. Lifetime value temporarily declined. As a result, the market’s confidence faltered. However, pricing is now catching up. Margins are improving, and the financial guardrails remain in place.

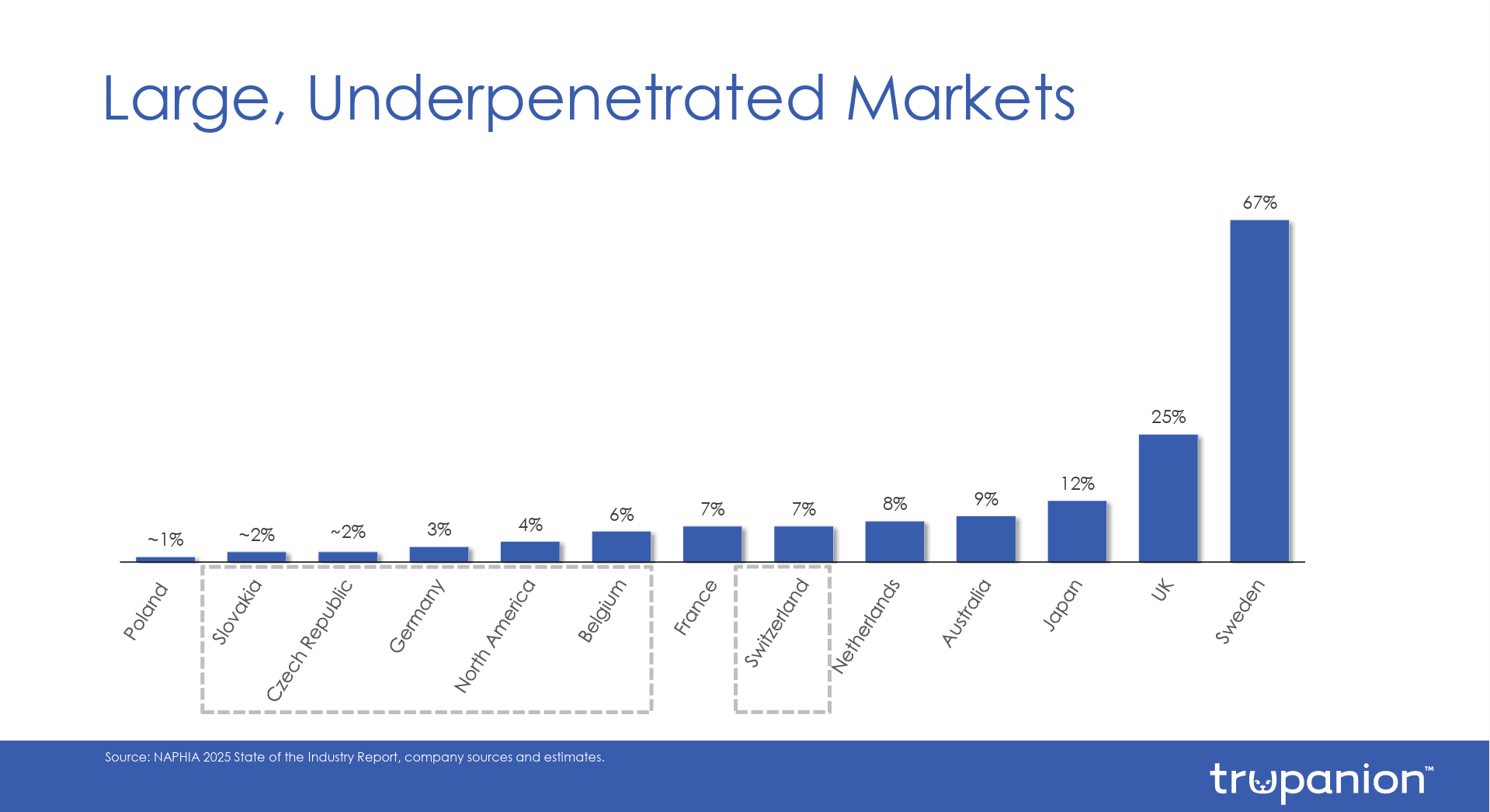

Source: Trupanion’s Q4 2025 investor presentation

Source: Trupanion’s Q4 2025 investor presentationThe key question is not whether Trupanion can return to hypergrowth. It is whether normalized subscription margins of 15% are durable while the subscription business compounds in the mid-teens.

I believe they are.

Growth Has Slowed, But That is Not the Same as BrokenBetween 2020 and 2022, when COVID prompted many to own pets, Trupanion was compounding revenue at 30-40%. Subscription pet adds were accelerating. Internal rates of return were consistently above target. The narrative was pristine.

Today, growth is mid-teens. That slowdown reflects three realities:

The pandemic pet boom pulled demand forward

Competition increased in digital distribution

Management intentionally moderated pet acquisitions while restoring margins

The veterinary channel remains the company’s structural advantage. Trupanion Express still differentiates at the point of care. Retention remains among the highest in the industry.

This is no longer a hypergrowth story but a disciplined specialty insurer operating in an underpenetrated category. Pet insurance penetration in North America remains low, and veterinary costs continue to rise. Those forces still support category expansion over time.

Source: Trupanion Q4 2025 presentation

Source: Trupanion Q4 2025 presentationThe key question is straightforward: can subscription revenue increase by 13% to 15% annually while preserving margin discipline and IRR targets? Keep in mind that Trupanion management is forecasting exactly that for FY 2026. If the answer to this question is yes, then the current valuation seems disconnected from its intrinsic value.

The Valuation DisconnectAt roughly $27 per share, Trupanion market capitalization is about $1.2b. Adjusting for cash and debt, its enterprise value is under $1b. That places the stock at less than 1x subscription revenue. For a business that has historically targeted 25% intrinsic value growth and deployed capital at 30% to 40% IRRs, that multiple implies structural impairment.

If subscription growth settles in the 8% to 10% range, the stock may simply be fairly valued. If growth stabilizes closer to 15% with normalized subscription margins of around 15%, the upside over a multi-year horizon becomes compelling.

This is not a bet on multiple expansion. It is a bet on durable underwriting discipline and mid-teens growth in a still underpenetrated category.

What Has Changed Since I First Bought ItI first bought Trupanion at $17 per share pre-COVID in my trading account. Back then, the appeal was explosive growth paired with strict capital guardrails. Today, the business is more mature. Growth is slower. Management replaced its CFO after a pricing misstep. Margin restoration took longer than expected. Yet the company is arguably more seasoned now. The balance sheet is solid. The playbook is clearer. Expectations are lower.

My Plan for TrupanionMy Traditional IRA position in Trupanion is currently small, under 2% of the account. I am fully allocated for Q1 under the deployment rules I set publicly. Barring a material deterioration in subscription growth or margin commentary in the upcoming earnings report, I intend to add in Q2 2026.

The bet is straightforward. I am underwriting normalized subscription margin durability and mid-teens growth. If that thesis holds, less than 1x EV/Sales for a disciplined, niche compounder looks attractive over a multi-year horizon.

This is not a comfort trade. It is a discipline trade. If margins hold and growth remains intact, intrinsic value should compound regardless of short-term sentiment. That is the bet I am willing to make.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. It examines how personality biases unconsciously influence investing behaviors. Learn more at my author page or order the book on Amazon. Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.February 2, 2026

Project 350K: A Review of My 2025 Traditional IRA Performance

Project 350K: A mid-year review was posted in June 2025

Project 350K: A mid-year review was posted in June 2025At the beginning of 2025, I set a goal for my Traditional IRA: to grow it to $350,000 over a 10-year period, as outlined in parts 1, 2, and 3. Since I already have most of my net worth invested in lower-volatility assets such as real estate and large-cap stocks, this account allows me to adopt a more aggressive investment posture. Meanwhile, statutory contribution limits naturally restrict the amount of capital deployed—a useful constraint given my Type 5 tendency to gravitate toward niche, smaller-cap companies and to risk overconcentration.

Reaching $350,000 over ten years implies a roughly 14% annualized return. That target was intentionally aggressive, designed to test both my investing process and my discipline. With the benefit of hindsight, 2025 provides the first meaningful data point on how that process performs under real-world conditions.

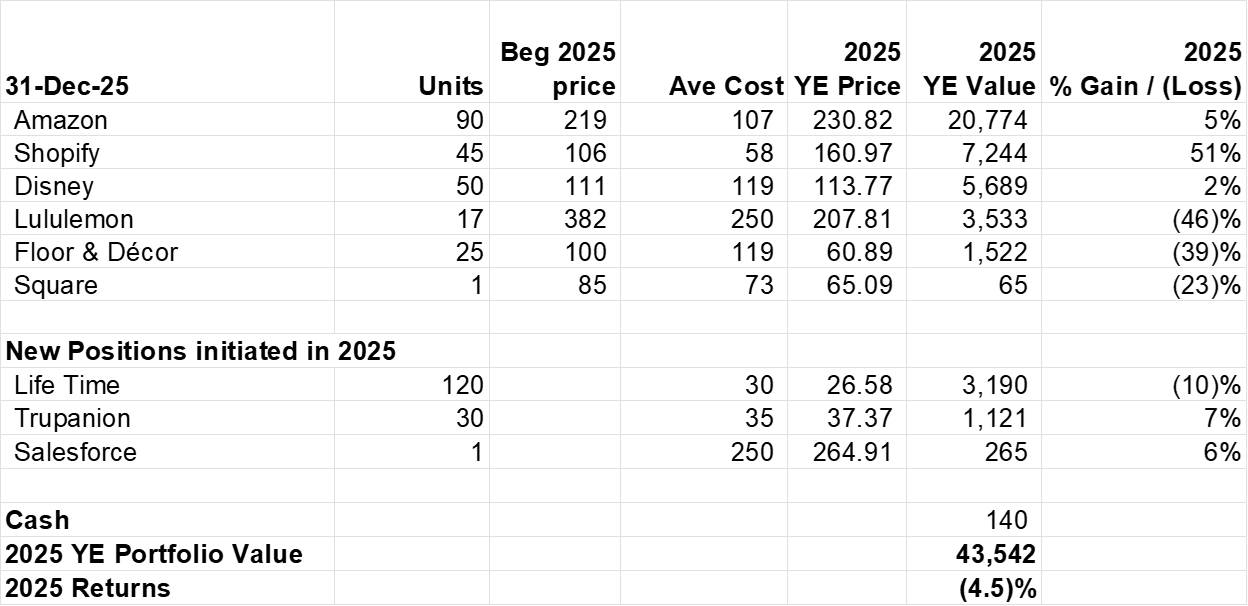

Hard Facts: Performance and Key DragsAs of December 31, 2025, the account stood at approximately $43,500 after receiving the maximum annual contribution of $7,000. The portfolio declined 4.5% for the year. By comparison, the S&P 500 returned 18%, and the Nasdaq rose 21%.

Here is a breakdown of the portfolio at year-end 2025:

The primary contributors to underperformance were a lack of meaningful appreciation in Amazon , which rose just 5%, and a significant drawdown in Lululemon over the course of 2025. Neither position was actively traded during the year; performance reflected market movements.

The drag was partially offset by a roughly 50% gain in Shopify . However, that was more than offset by a poorly timed position in Globant , which resulted in a material loss during 2025.

Globant warrants specific attention. I initiated the position early in the year, added shortly thereafter, and ultimately exited the entire stake by August at a loss. While the capital at risk was contained, the sequence highlighted a recurring issue: adding to a position before sufficient evidence had accumulated to support the thesis, and holding on longer than warranted as fundamentals deteriorated.

The Central Lesson: Pacing Matters More Than IdeasThe most consequential takeaway from 2025 was not stock selection but capital deployment, as my mid-year review made clear. I allocated the majority of my annual contribution in the first quarter. When volatility increased and opportunities improved later in the year, flexibility was limited.

Front-loading capital reduced optionality and increased sensitivity to early-year misjudgments. In contrast, positions initiated later in the year—such as incremental additions to Life Time and Salesforce —benefited from better entry points and clearer operating signals.

Portfolio Structure ObservationsThe portfolio remains concentrated, with only a handful of positions carrying most of the weight. This remains a work in progress. Over time, I expect the account to hold roughly 12–15 positions, each with an allocation of approximately $5,000–$7,000, focused on businesses with operating leverage and durable brand or platform moats.

One structural adjustment I am introducing in 2026 is the selective use of opportunistic trades to enhance returns. With Amazon representing roughly half of the portfolio, achieving alpha is difficult unless it materially outperforms the market. To compensate, I will selectively deploy capital into shorter-duration opportunities in companies I know well from my trading account.

This thinking led to a position in Elastic in January 2026, funded by selling a legacy position in Floor & Decor . I have followed Elastic for years and previously held a position there profitably before exiting in 2024. Currently, Elastic trades near 4x EV/Sales, making it both a recovery candidate and a potential acquisition target. This position is sized accordingly and assessed on a different time horizon than my core holdings.

With additional purchases in Life Time and Salesforce completed in January, along with the Elastic position, capital deployment for Q1 2026 is complete.

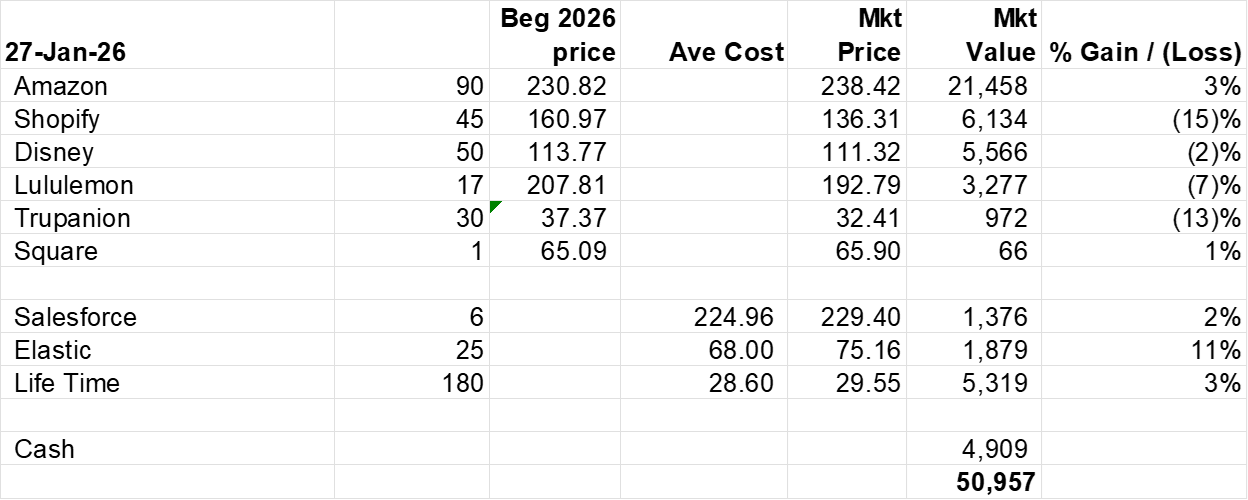

Current Traditional IRA Portfolio (Jan 26, 2026, closing price)Looking Ahead to 2026

Current Traditional IRA Portfolio (Jan 26, 2026, closing price)Looking Ahead to 2026Based on the 2025 experience, my focus for 2026 is as follows:

More deliberate pacing: Capital will be deployed more evenly across quarters.

Anchor stock: Amazon remains the portfolio anchor. While it may dampen upside in strong markets, it provides stability and scale.

Long-term conviction holdings: Life Time , Salesforce , Shopify , Lululemon , and Disney remain core positions, subject to further top-ups but capped at $5,000–$7,000 each.

Positions under evaluation:

Square $XYZ remains a meaningful holding in my trading account, but it is a small position here, resulting from deploying excess cash before Project $350K took shape. Although it has underperformed, recent management guidance indicates accelerating gross profit growth. While I identified this company as a potential multi-bagger as early as 2022, the stock and its underlying financial performance struggled in recent years. I will revisit this position in the coming quarters, mainly to adjust risk appropriately for my trading account.

Trupanion is another re-entry after a profitable prior investment. The pet insurance market continues to grow, though topline growth has slowed to the low-teens. This position will be reassessed following Q4 results and 2026 guidance.

The original $350,000 target remains intact, but it is best viewed as an outcome rather than a mandate. Achieving it will require favorable market conditions, disciplined execution, and time. More importantly, success depends on building a repeatable process that limits large errors and preserves upside when conditions improve.

2025 did not deliver outsized returns. It did, however, deliver clarity. In a multi-year project, that may be the more valuable currency.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. Learn more at my author page or order the book on Amazon. Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.November 3, 2025

The Trade Desk’s Existential Crossroads

The Trade Desk ( ) has long been the open internet’s counterweight to the walled gardens — an advertising platform built on transparency, neutrality, and scale. For years, that narrative justified a premium valuation. But in the wake of June’s earnings, which sent the stock tumbling from the $90 range to the low $50s, investors must now confront an uncomfortable question: Is TTD’s dominance still structural, or has it become merely executional?

I have held for years and pared down half my holdings last summer. I have been feeling stuck with those residual shares—not out of fading admiration for the company, but because the competitive dynamics have shifted, and the market’s re-rating may be more structural than sentimental.

The Catalyst Behind the SlideThe June 2025 quarter was meant to showcase the payoff from Kokai, $TTD’s new AI-driven platform. Instead, it underscored the gap between promise and proof. Revenue grew 19% year over year, and Q3 is expected to post a 14% increase, far below expectations. The result was a valuation compression that wiped out years of multiple expansion.

This is not a broken business—far from it. still generates strong free cash flow and remains the default DSP for most major agencies. But the premium multiple it once enjoyed was built on a narrative of sustained 25-30% growth. That story has now flattened to mid-to-high teens, and the market is adjusting accordingly.

Kokai: A Step Forward, Not a Moat

Kokai, the company’s much-touted AI overhaul, is an impressive technological evolution. It brings AI-enhanced bidding, supply-path optimization via OpenPath and OpenSincera, and a new “Deal Desk” feature for pacing and forecasting. Roughly three-quarters of spend now runs through it, with internal data showing double-digit KPI improvements.

Yet despite these advancements, Kokai doesn’t create a new moat — it merely enhances ’s execution layer. The open internet remains fragmented, and while Kokai helps clean up the supply chain, it does not change the economics of ad demand. and (DV360) are embedding their own AI stacks into ad delivery, with privileged access to identity and inventory that cannot match. is pushing deeper into shoppable CTV, and even legacy players like Adobe () are modernizing their DSPs for enterprise clients.

The open internet narrative still matters — but advertisers increasingly value identity and efficiency over philosophical purity. In that environment, ’s “neutrality” advantage shrinks.

The Valuation RealityAt roughly 10x EV/Sales and over 40x EV/EBITDA—even after the sell-off—it needs to deliver at least 20% growth consistently to sustain its multiple, and much more to rerate it back to its prior stock prices. Management deserves credit for prudence and capital discipline, but at today’s scale, even strong execution cannot offset macro softness, ad-budget caution, and rising competition from vertically integrated ecosystems.

I view this re-rating as not merely cyclical but evolutionary. The company’s next growth leg must come from deeper retail-data integration, global CTV penetration, and proven AI monetization. Those are multi-year endeavors.

My Takeremains a best-in-class DSP with brilliant leadership, robust cash generation, and a differentiated culture. It is still the platform of choice for brands that value transparency. But the stock’s investment case has shifted: from a hypergrowth disruptor to a high-quality operator priced like one.

I will be looking to liquidate my remaining shares. This is not a bearish call on ’s business — it is an acknowledgment that the risk-reward profile no longer fits the narrative that once propelled it. The company will likely continue to lead in its category, but the category itself is maturing.

Sometimes the hardest sell is not the broken story, but the still-great one that has already told its best chapter.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

There will not be a Substack post in December. January 2026 will be a year-end review of my Project 350k (see Part 1, Part 2, and Part 3) performance in 2025.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance. My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. Learn more at my author page or order the book on Amazon.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.October 1, 2025

REPOST: What is Quality?

In the whirlwind of life lately—parenting, graduate school, startup building, and book launch—I haven't had time to write a fresh October piece. But perhaps that is a good excuse to revisit two earlier posts I remain proud of.

These two pieces, written back to back in August 2023, were born from a period of deeper questioning: What does “quality” mean in investing? How do we stay grounded when we feel stuck with an underperforming stock? The catalyst was Robert Pirsig’s Zen and the Art of Motorcycle Maintenance, a book that taught me that “quality” is not a static trait — it is an event, an interaction, a moment of harmony between subject and object. That is a surprisingly resonant lens through which to view both investments and investor behavior.

In “What Is Quality?”—reposted below—I pushed back against the overuse of that term in the financial world. Everyone claims to seek it, but few can define it. In the follow-up, “Stuck With an Investment?”, I unpacked the emotional complexity of holding a position that no longer sparks conviction but still resists being sold.

Both posts speak to a central theme: investing is as much about identity and adaptability as it is about metrics. If you are wrestling with decisions around holding, trimming, or doubling down, these essays may offer a useful frame.

Next month, I plan to share reflections on The Trade Desk ()—one of my earliest tech holdings that feels stuck given recent performance—once I have more breathing room.

*********

(August 2023)

The book Zen and the Art of Motorcycle Maintenance: An Inquiry Into Values is a narration of a summer motorcycle trip undertaken by a father and his son. It is not just a novel but a penetrating examination of numerous philosophical questions.

“Zen and the Art of Motorcycle Maintenance sold millions of copies and made Pirsig a reluctant hero to generations of intellectual wanderers…Zen was an instant classic — a work of literature that captured the spirit of its time and retained its appeal long after the hippie movement had faded.” — Washington Post

“Zen and the Art of Motorcycle Maintenance sold millions of copies and made Pirsig a reluctant hero to generations of intellectual wanderers…Zen was an instant classic — a work of literature that captured the spirit of its time and retained its appeal long after the hippie movement had faded.” — Washington PostHalfway through this book, I am intrigued by the contentious concept of "Quality.” Specifically, two lines have stuck in my head:

“How are we supposed to know what quality is?”

“…even though Quality cannot be defined, you know what Quality is.”

While the “Quality” discussion in the book is not related to investing or business, I cannot help but wonder about its applications in stock picking.

Quality Investments: Only in Hindsight?To make this post more focused, I shall stick to consumer-related companies.

Within that space, we can agree that some of the most successful companies include Nike, Apple, Amazon, Costco, Tesla, and Netflix. They have all grown by orders of magnitude in terms of earnings, scale, cultural impact, fandom, and of course, share price.

Warren Buffett famously invested in Apple in 2016 - he had deemed it a Quality company. Apple is now Berkshire’s most prominent position. (Picture source: The Hustle)

Warren Buffett famously invested in Apple in 2016 - he had deemed it a Quality company. Apple is now Berkshire’s most prominent position. (Picture source: The Hustle)However, before arriving at their vaulted positions, they all went through growing pains. Apple struggled with topline concerns when Buffet took a stake in the company. Tesla was in “production hell” when it tried to ramp up Model 3 at Fremont and almost went bankrupt. Netflix had multiple near-death episodes throughout its corporate history, as chronicled in the book, That Will Never Work, authored by its co-founder, Marc Randolph.

In the eye of the storm, few would have been able to discern “Quality” amidst missed earnings, social media chatters, negative headlines, production delays, and intense cash burn.

Unpacking QualitySeasoned investors, whether retail or institutional, have probably reviewed enough companies to know (at least on some subconscious level) what a quality stock should be. Borrowing from the list of exemplary companies above, one may infer the following to be some of the critical characteristics of “Quality”:

Products and services enjoying customer loyalty and renewal thereof with each generation of consumers

Strong cost controls and capital discipline

Growing total addressable market through continual additions to product and service line-up, plus international expansion

Some investors like to use quantifiable traits like minimum revenue growth or profitability to qualify for “Quality.” While the approach is sound, that logic may break when a company undergoes financial turbulence, as did giants Amazon and Meta in recent quarters for different reasons.

Conversely, we probably know what low-quality means, primarily by studying cautionary tales. Peloton crashed and burned after mismanagement of hypergrowth discombobulated its operations to the point where the new CEO Barry McCarthy had to completely reverse its vertically integrated strategy and raise rescue financing.

Another example of a low-quality but hyped stock is Allbirds BIRD 0.00%↑. The company has been in the news for its lackluster financial results, burning through cash and struggling with waning demand. For a brand so early on its expansion track, Allbird has (so far) failed to live up to its promise.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Allbirds' ad featuring Lindsay Lohan (2022)Quality is Earned Over Time?

Allbirds' ad featuring Lindsay Lohan (2022)Quality is Earned Over Time?

“You never know who's swimming naked until the tide goes out.”

Warren Buffett

To be a “Quality” company, it must first endure. It is useless to have all the trappings of a successful corporate in the making if it cannot survive recessionary pressures or a hostile capital market.

For example, in the face of growing competition and a weakening economy, Tesla slashed prices to boost demand and keep its Giga factories running at full speed. But thanks to its established branding, customer goodwill, and balance sheet strength, it still generated near-record cashflows and sustained considerable investments into additional Giga factories and the production ramp of Cybertruck and Semi.

A Tesla Semi prototype on display outside Petersen Automotive Museum in Los Angeles

A Tesla Semi prototype on display outside Petersen Automotive Museum in Los AngelesIn contrast, the chances of Lucid enduring as a standalone enterprise look bleak, with its suboptimal production scale, rapid cash burn, and weak balance sheet. Along with EV peers at early (and costly) stages of expansion, these newbies cannot be considered “Quality” companies until they survive multiple storms.

Conclusion: Quality and Proven Resilience may be InseparableI may therefore deduce that the longer a company has been thriving (and exhibiting hallmarks of a well-run enterprise) over multiple economic cycles, the higher its “Quality.”

Quarterly numbers may display choppiness, but proven resilience over many years (or decades) is perhaps the closest indicator of “Quality” when reviewing investment opportunities.

I think we all know it.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance. My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. Learn more at my author page or order the book on Amazon.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.September 9, 2025

Suit Yourself Is Now Out!

After years of reflection and writing, my debut book, Suit Yourself: A Portfolio Strategy for Every Personality Type, is finally out, published through Koehler Books. This side passion project brings together my professional and personal journey across psychology, personal finance, and the many ways our identities shape how we invest.

For those who have already started reading, thank you—and if you found the book useful or thought-provoking, I would be grateful if you left a review on Amazon. Every review helps the book reach more readers who might benefit from its message.

It is now available through:

Check out my recent interview with ThinkAdvisor: Perfectionist? Achiever? Investigator? How Clients' Personality Type Informs Their Investment Style by Jane Wollman Rusoff.

More interviews and features are in the pipeline—stay tuned.

People who have read the book have been giving me encouraging feedback, which still surprises me. I have had my moments of self-doubt about writing this book—even now. But maybe that is just part of being human and doing something for the first time. Writing and publishing a book is not a linear path, and I am learning to sit with that.

Thank you to everyone who has supported the journey.

To find out more about your typology, try the free quiz on my website.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.August 11, 2025

Life Time: A Small-Cap Bet on Stickiness, Scale, and Pricing Power

An abridged version of this write-up first appeared on Yahoo Finance as a featured community analysis.

Local Life Time club in Atlanta, Georgia

Local Life Time club in Atlanta, GeorgiaPeter Lynch’s core advice is simple: invest in what you truly understand. I have been a Life Time member since November 2024—using not just the gym, but also the spa, daycare, and café—and that proximity prompted deeper due diligence into the company as an investment opportunity. At the same time, I recognize the risks and potential for biases: remains a small-cap company, with a market value under $10 billion, and my favorable experience as a member may color my investor perspective. Nevertheless, I believe can more than double its current share price of approximately $27 within the next 2-3 years, and I have taken a small position to create alpha in my Traditional IRA.

Hard Moat and Meaningful White Spaceoperates 184 centers across ~30 US states and one Canadian province. The company has explicitly guided for 10 to 12 new openings per year—a measured pace that aligns with its premium positioning and capital discipline. Management has not set a long-term unit count target; however, investor materials suggest that meaningful whitespace remains in both urban and affluent suburban markets, particularly through mall integrations and residential developments. With an average club size of approximately 100,000 square feet, is building a national wellness infrastructure that cannot be easily replicated.

Inclusive Demographics, Pricing PowerWhile many gyms target specific groups or provide generic experiences, differentiates itself. It is more than simply a fitness facility; it serves as a lifestyle community that welcomes families with young children, working professionals, retirees, and individuals of all ages, genders, and sexual orientations. The diversity of its members becomes clear during my visits to the local club.

This inclusive appeal supports two of Life Time’s most durable advantages: member stickiness and pricing power. On the Q2 2025 earnings call, management noted that visits and retention were at all-time highs, prompting a deliberate focus on raising prices and ancillary revenues rather than expanding membership. That level of strategic restraint is rare in fitness retail and underscores the strength of Life Time’s value proposition.

Optimization and Greater Return on InvestmentFinancially, is entering a more disciplined phase. Revenue for Q2 2025 increased to $762 million, up 14% year over year. Net income rose by 37%, and free cash flow turned positive for the fifth straight quarter. These improvements are deliberate. The company is intentionally shifting its focus from rapid expansion to margin growth, cash generation, and debt reduction.

In contrast, , which relies heavily on a franchise model, reported $341 million in revenue for the second quarter of 2025, representing a 13% increase. Life Time's adjusted EBITDA was $211 million, surpassing Planet Fitness's $148 million. Membership numbers were 849,643 for Life Time and 21 million for Planet Fitness.

That gap reflects two very different business models: focuses on unit growth and franchise royalties, while emphasizes a more personalized, asset-intensive platform with greater monetization opportunities. In June 2025, Life Time signed a $150 million sale-leaseback deal, converting real estate into capital without losing control. Another $100 million in sale-leaseback transactions are expected in the second half of the year. This is a company trading scale for sustainability, doing so on its own terms.

What Could Go Wrong and Valuationis dependent on retaining affluent members across economic cycles, and its business model carries significant operating leverage. Any revenue slowdown or cost mismatch could disproportionately compress margins. Growth initiatives in digital and branded products are still relatively unproven. Momentum is real, but execution must remain tight.

Still, at the current valuation, the risks might be justified by the potential upside. Management expects 2025 revenue to grow by around 14%, reaching $3.0 billion. Adjusted EBITDA is forecasted to increase by 20%, and net income by over 86%—showing that margin expansion is now a key focus. has also reduced its net debt leverage from 3.0x to 1.8x over the past year, indicating disciplined cash flow management. Based on the company's 2025 adjusted EBITDA guidance, its enterprise valuation (with a $27 per share price) is about 12 times. In comparison, trades at roughly 20 times (at $105 per share).

If continues to grow revenues in double digits while further expanding margins, more than doubling its share price is plausible.

Final Thoughtis not trying to be everything to everyone. It is building a high-end, high-engagement wellness platform with a long runway for monetization and margin improvement. While the stock remains overlooked relative to its scale, pricing power, and member retention, the underlying business is gaining operating leverage with each passing quarter. For investors seeking exposure to health, fitness, and real estate in one disciplined vehicle, offers asymmetric upside.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance. My book, Suit Yourself: A Portfolio Strategy for Every Personality Type, blends Enneagram psychology, pop culture, and behavioral finance to offer a personalized roadmap to investing. Learn more at my author page or preorder the book on Amazon.

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.July 1, 2025

Early Praise for Suit Yourself and a Moment of Gratitude

Front and back covers of my upcoming book, to be published on August 18, 2025. See below for pre-order details.

Front and back covers of my upcoming book, to be published on August 18, 2025. See below for pre-order details.I started writing Suit Yourself: A Portfolio Strategy for Every Personality Type to bridge two worlds that rarely meet: the inner world of personality and the outer world of personal finance. I wanted to explore why investing feels so different for each of us—and why that difference deserves to be honored, not erased through a one-size-fits-all approach.

What began as a personal curiosity has evolved into a book that others are now starting to see themselves in. That has been the most rewarding surprise.

As we get closer to launch on August 18, I wanted to share a few words from early readers that have meant the world to me:

“One of the biggest challenges investors face is between the ears. Learning how to manage our emotions and understanding why we do what we do goes a long way towards market success. Benjamin has written a book helping outline those challenges and how to overcome them by understanding our personality types.”

— Dave Ahern, Co-host of the popular investing podcast, Investing for Beginners

“The highest ROI activity you can do isn't analysis of a company or a sector, it's understanding yourself… Suit Yourself helps you understand how you can leverage your own disposition to maximize your strengths, and avoid your pitfalls.”

— Nathan Worden, Community Manager, Yahoo Finance

“Suit Yourself is more than an investment guide—it goes beyond sound investment strategies and provides clarity into the emotional rollercoaster of life itself… Concise, yet powerful… Definitely a book to have on any bookshelf, to read, and to reflect upon repeatedly over time.”

— Felicia Teng, CPA and Founder of Get Counting

“Benjamin Tan's Suit Yourself provides an insightful exploration of investment strategies through the lens of the Enneagram personality framework. Through his entertaining use of pop culture references and personal stories, Tan turns complicated financial ideas into understandable concepts while providing customized investment strategies for people to match their portfolio choices with their personal characteristics.”

— Dr. Patrick Behar-Courtois, Author of Maximizing Organizational Performance

Writing this book stretched me in all the right ways. Publishing it has stretched me even more. I am grateful to everyone who believed in the core message: that the best investment plan is the one that suits you.

If you would like to be one of the first to read it, Suit Yourself is now available for pre-order:

Thank you for walking this journey with me. More soon.

To find out more about your typology, try the free quiz on my website.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.June 5, 2025

Mid-Year Lessons from Project 350k

When I began Project 350k (see Part 1, Part 2, and Part 3) earlier this year, the idea was simple: grow a modest Traditional IRA portfolio into something far more substantial, eventually hitting a $350,000 target. The implied target return is around 15%—ambitious but not unachievable. Statutory limits on the amount of capital contributions would also cap the amount of risk I take relative to my net worth, which comprises a mix of home equity, REITs, fixed income, large caps, and mid-sized companies poised for S&P inclusions.

Now that we’re halfway through the year, I thought I’d pause and reflect on a few things I’ve already learned.

Time for a mid-year stock take and make some pivots to investing style1. Timing of Deployments Matters:

Time for a mid-year stock take and make some pivots to investing style1. Timing of Deployments Matters:With a contribution cap of $7,000 per year, I should have been more strategic with the timing and sizing of my buys. Not used to making deployments of this size, I was still operating the Traditional IRA account without being fully cognizant of limitations.

Between January and February alone, I made all four of my current investments:

Disney ( ) : Purchased $2,782 @ $107/share (Jan 16)

Globant ( ) : Purchased $2,000 @ $200/share (Jan 27)

Life Time Group ( ) : Purchased $1,153 @ $32.95/share (Feb 18)

Trupanion ( ) : Purchased $1,050 @ $35/share (Feb 20)

Looking back, I essentially used up the annual limit within the first six weeks of the year! That decision left me with no capital to act on better opportunities. When markets wobbled in April and May, I had to sell my stake in Warner Music Group ( ) to free up capital. While that position was always earmarked for disposal due to its tepid growth profile, I still should have been more conservative with the deployments of this small portfolio.

There’s a discipline to pacing.

2. Sizing Should be ConsistentMy allocations were uneven. Disney ( ) and Globant ( ) got significantly larger portions than Life Time ( ) or Trupanion ( ). If I had stuck to $1k per name, I could have left room for later conviction adds—or scaled out more gracefully as earnings reports came in during Q1.

3. Risk is About MeReentering Globant ( ), a name I had previously owned and profited from, felt safe. But it is a small cap. And historically, I have had a blind spot for these.

This particular investment turned into my Achilles' heel. Q1 results disappointed, and revenue guidance for 2025 is well below my minimal 10% threshold for Project $350K. I am now looking for an exit from this name. Meanwhile, larger-cap names I already hold in my trading account—like The Trade Desk ( ) and Zscalar ( )—have fared much better.

Ironically, I ignored them to “diversify.” Geez.

4. My personality Showed UpLooking back, I can see how much my personality shaped the early moves in this portfolio—perhaps more than I realized at the time. In my upcoming book, Suit Yourself, I explore how each of the nine Enneagram types tends to approach investing, with their own psychological biases and behavioral tics. As a Type 5 who can lean into a Type 7—optimistic and, at times, impulsive—I now recognize how those traits showed up in my decision-making.

A preview of the front and back covers of my upcoming book,

Suit Yourself

A preview of the front and back covers of my upcoming book,

Suit Yourself

The rush to deploy capital was not just about market timing. It was about chasing momentum, fearing I would miss out on ideal entry points. It felt like decisiveness, but in hindsight, it was impulsivity disguised as confidence. I told myself I was making bold, reasoned moves. But really, I was skipping the part where I pause, zoom out, and ask: “Is this the best use of limited capital right now?”

There’s a core lesson here: investors are not spreadsheets. We are human. And when left unchecked, our patterns—risk-averse or risk-seeking—can lead us astray, even when we know better. I have spent years studying valuation, business fundamentals, and capital cycles. Yet in this small account, the psychological impulse to act quickly overrode what should have been a more methodical deployment plan.

Self-awareness does not guarantee success but gives you a fighting chance to interrupt your worst habits. That’s what Suit Yourself—and this project—is really about.

Follow me on X.com (formerly Twitter) @ConsumeOwnTech and Yahoo Finance

Thanks for reading Consume Your Own Tech Investing! Subscribe for free to receive new posts and support my work.

Subscribe to Consume Your Own Tech Investing FOR FREE to receive a welcome email with the following:

My Top 10 high-conviction portfolio positions, combining value and growth stocks

Book recommendations in investing, consumer, and tech sectors

Monthly articles delivered straight to your inbox

NOTE DISCLAIMER: This blog does not represent investment advice and is solely the author’s opinion. Contents herein are for educational purposes only. Any discussion here is not an offer to sell or the solicitation of an offer to buy any securities of any company. The author is not a stockbroker or financial adviser. Consume Your Own Tech Investing makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. Consume Your Own Tech Investing recommends that you do your own due diligence. Please see the full Disclaimer on the About page for more detail.